Dow's Modest Weekly Gain Amid Inflation Concerns, Precious Metals Retreat on Stronger Dollar, and Key Economic Events Ahead | Daily Market Analysis

Key events:

- USA - Consumer Inflation Expectations

On Friday, the Dow concluded with an increase, achieving a modest weekly advancement. However, the potential for further gains was limited due to resurfacing concerns about inflation, which led to an increase in Treasury yields. These inflation worries also dampened investor expectations that the Federal Reserve would refrain from implementing interest rate hikes later in the year.

The Dow Jones Industrial Average demonstrated a 0.3% uptick, corresponding to a 105-point rise. In contrast, the Nasdaq experienced a decline of 0.6%, while the S&P 500 saw a marginal decrease of 0.1%.

On Monday, both gold and copper prices experienced declines, dropping to their lowest points in a month. This downward movement was attributed to the influence of a stronger dollar, prompted by growing apprehensions regarding elevated US inflation, which in turn amplified concerns about the potential for higher interest rates.

The rise in the dollar was notably evident, as it reached a level not seen in over a month against a basket of currencies. The heightened strength of the dollar had a dampening effect on the majority of commodities priced in this currency.

The focus of the previous week revolved around US inflation data. As reported by the Bureau of Labor Statistics (BLS) on Thursday, the headline consumer price inflation (CPI) exhibited a milder-than-anticipated rise of 3.2% over the twelve months ending in July. This figure came in slightly below the expected 3.3%, although it increased from the previous 3.0%. This followed a year-long trend of diminishing prices after reaching a peak of 9.1%. Concurrently, the core US inflation for the same period eased to 4.7%, lower than the predicted 4.8%, marking a return to levels last observed in late 2021. Additionally, on a month-over-month (MoM) basis, both the headline and core CPI readings for July mirrored those of June, each advancing by 0.2%, as anticipated. Alongside the consumer price inflation metrics, the US witnessed a slight rise in weekly unemployment filings on Thursday, surpassing 20,000 to reach 248,000.

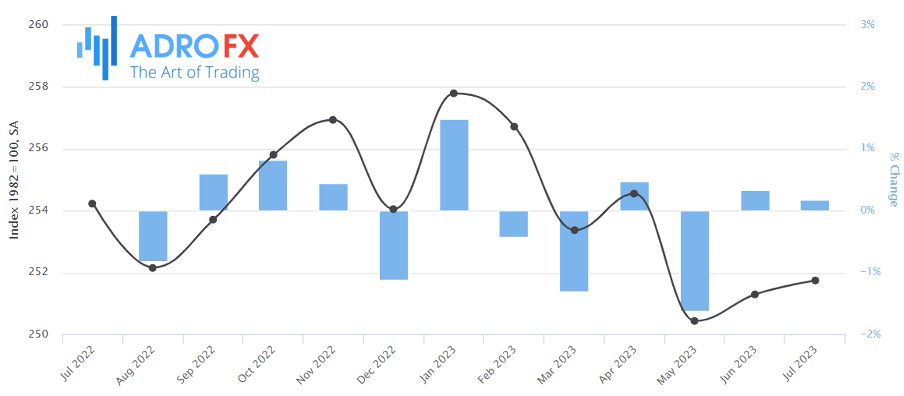

Subsequently, Friday ushered in the latest Producer Price Index (PPI) inflation figures, revealing higher-than-expected year-over-year (YoY) and month-over-month (MoM) increments for July. This signified a reversal of the year-long trend of declining wholesale prices. YoY PPI headline inflation surged by 0.8%, a notable increase from June's upwardly revised 0.2%, slightly surpassing the median projection of 0.7%. Moving from June to July, headline PPI prices ascended by 0.3%, a significant rise from the previous 0.0% and just surpassing the anticipated 0.2%. This marked the most substantial month-on-month escalation since the start of the year. The BLS attributed this widespread surge primarily to a rise in service costs, which increased by 0.5%, indicating the swiftest recovery in almost a year. Interestingly, the ascent in PPI inflation (and headline CPI) exhibited a partial divergence from the University of Michigan's (UoM) release of consumer inflation expectations on Friday. This report indicated a decline in August to 3.3%, down from July's 3.4%.

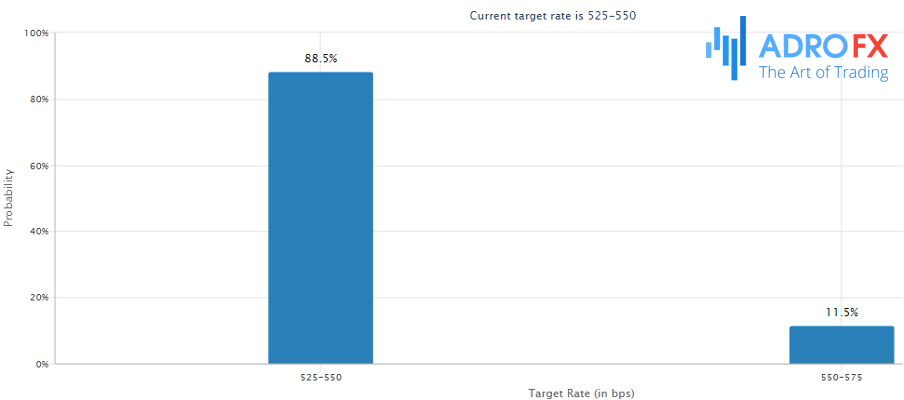

Looking ahead, significant events in the United States during the upcoming week include the release of retail sales data for July and the Empire State manufacturing index for August. The possibility of weaker-than-anticipated figures here could reinforce the narrative of a gradual economic slowdown. The subsequent focus will be on the minutes from the Federal Open Market Committee (FOMC) meeting, scheduled for Wednesday. If these minutes indicate that Fed officials are leaning towards a pause in rate hikes for September or November, it could exert downward pressure on the dollar and offer support to equities and bonds. Currently, the implied rate trajectory for the next rate decision on September 20th suggests a 90% likelihood that the Fed will maintain the current target range of 5.25%-5.50%.

Across the Atlantic, attention will be on the UK inflation data for July, set to be released on Wednesday. Market consensus suggests that year-on-year consumer price inflation may ease to 7.4% from June's 7.9%, while core inflation for the same period is projected to remain more resilient at 6.8%. On a month-on-month basis, economists expect both headline and core inflation to stay unchanged from June to July, rising by 0.1% and 0.2% respectively. Presently, markets are pricing in a 70% probability that the Bank of England (BoE) will raise the Official Bank Rate by another 25 basis points at the upcoming meeting on September 21st, with a projected terminal rate of 5.75% by March 2024. In the event of softer inflation data this week, rate forecasts could decline, potentially pressuring the British pound. Conversely, any positive surprises in the data could have the opposite effect. Additionally, it's important to note other significant UK data releases during the week, including employment and wage numbers for June on Tuesday, and retail sales data for July on Friday.

The week also brings the release of the latest Reserve Bank of Australia (RBA) meeting minutes on Tuesday, along with the quarterly Aussie wage price index. Additionally, all eyes will be on the Reserve Bank of New Zealand (RBNZ) on Wednesday. The consensus among economists suggests that the central bank has concluded its tightening cycle.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates