Stocks Surge to New Peaks as S&P 500 Hits Record High; GBP/USD Dips in Anticipation of UK CPI Figures | Daily Market Analysis

Key events:

- UK - CPI (YoY) (Feb)

- USA - Crude Oil Inventories

- USA - FOMC Economic Projections

- USA - FOMC Statement

- USA - Fed Interest Rate Decision

- USA - FOMC Press Conference

- New Zealand - GDP (QoQ) (Q4)

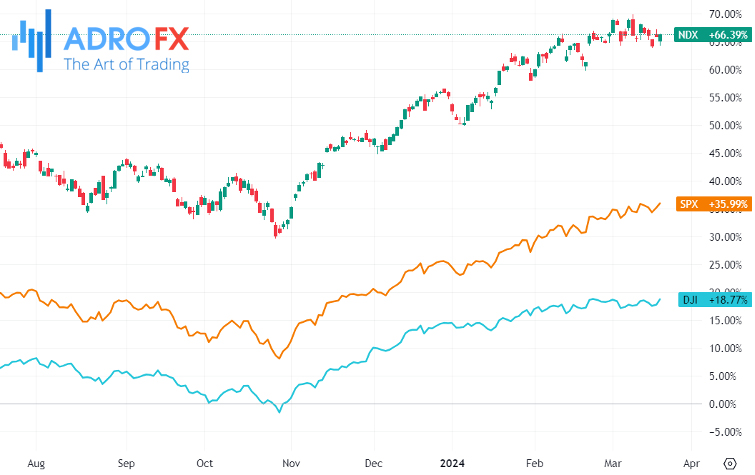

Tuesday saw the S&P 500 reaching unprecedented heights, buoyed by the energy sector's performance and a dip in Treasury yields, all while investors anticipated Wednesday's Federal Reserve decision. The S&P 500 surged by 0.6%, setting a new record at 5,178.48, with the NASDAQ Composite also climbing by 0.4%, and the Dow Jones Industrial Average gaining 320 points, marking an increase of 0.8%.

The Federal Reserve's two-day meeting commenced on Tuesday, with expectations of unchanged rates, but investors remained cautious, considering the possibility of a reduced number of rate cuts for the year ahead due to recent inflation data surpassing expectations. Data released in recent weeks indicates that US inflation has consistently exceeded the central bank's medium-term target of 2%.

Despite concerns about a potentially less dovish stance from the Fed, Treasury yields experienced a decline, with the 2-year Treasury yield dropping by 4 basis points to 4.69%. Additionally, positive economic indicators showed signs of recovery, particularly in the housing sector, with housing starts and building permits surpassing expectations.

The Australian Dollar showed resilience, rebounding from earlier losses and striving to enter positive territory on Wednesday. The strengthening ASX 200 contributed to the AUD's performance, supporting the AUD/USD pair, although the robust US Dollar could be exerting downward pressure on the pair.

Meanwhile, the Reserve Bank of Australia maintained interest rates at a 12-year high of 4.35% during its latest meeting. RBA Governor Michele Bullock emphasized the ongoing battle against inflation but refrained from providing specifics regarding the timing or likelihood of rate adjustments, indicating the bank's openness to various possibilities.

The US Dollar Index continued its upward trajectory, attributed to improved US Treasury yields. Investors eagerly awaited the Federal Reserve's interest rate decision scheduled for Wednesday, with the Federal Open Market Committee widely expected to maintain the key federal funds interest rate within the range of 5.25% to 5.5%.

During the Asian session on Wednesday, the Japanese Yen entered a bearish consolidation phase, hovering near a four-month low against the US Dollar. This downtrend was triggered after the Bank of Japan raised short-term interest rates for the first time since 2007 and abandoned its complex Yield Curve Control policy at the conclusion of the March meeting on Tuesday. Despite maintaining an accommodative stance on financial conditions, the central bank refrained from providing clear guidance on future policy steps or the pace of policy normalization. This ambiguity, coupled with the prevailing risk-on sentiment, has persisted for the seventh consecutive day, exerting downward pressure on the safe-haven JPY.

Meanwhile, the price of Gold continued its sideways consolidative movement during the Asian session on Wednesday as traders adopted a wait-and-see approach ahead of the highly anticipated FOMC monetary policy meeting.

Despite this, the downside for Gold prices remains supported due to geopolitical risks emanating from the prolonged Russia-Ukraine conflict and tensions in the Middle East. Investors appear cautious and await further clarity on the Federal Reserve's stance on interest rate cuts before making significant directional bets. As such, attention will be focused on updated economic projections and remarks from Fed Chair Jerome Powell during the post-meeting press conference, which are expected to influence the next significant move for the non-yielding yellow metal.

During the early Asian session on Wednesday, the GBP/USD pair sustained losses for the fifth consecutive day. Market participants are eagerly anticipating the release of the UK February CPI inflation data, which could provide insights into the Bank of England's stance on interest rates.

The UK CPI inflation report, scheduled for later in the day, holds significance as it may shed light on whether the BoE will signal the timing of its first interest rate cut or maintain its current higher rate stance for an extended period. Forecasts suggest that the headline UK CPI is expected to show a 3.6% month-on-month increase in February, down from a 4.0% rise in January.

Meanwhile, the Core CPI figure is projected to decline to a 4.6% year-on-year rate in February, compared to a 5.1% rise in January. A stronger-than-expected inflation report could persuade the BoE to prolong its higher rate narrative, potentially bolstering the Pound Sterling against the US Dollar.

Traders will closely monitor the UK CPI inflation data ahead of the Federal Reserve's interest rate decision. Following the Fed meeting, attention will shift to Chairman Jerome Powell's press conference and the release of economic projections. Additionally, market participants will closely observe Thursday's BoE interest rate decision for further insights into monetary policy.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates