Markets Edge Higher as Traders Weigh Earnings, Trade Deals, and Central Bank Decisions | Weekly Market Analysis

Key events this week:

Tuesday, July 29, 2025

- USA - CB Consumer Confidence (Jul)

- USA - JOLTS Job Openings (Jun)

Wednesday, July 30, 2025

- USA - ADP Nonfarm Employment Change (Jul)

- USA - GDP (QoQ) (Q2)

- Canada - BoC Interest Rate Decision

- USA - Crude Oil Inventories

- USA - FOMC Statement

- USA - Fed Interest Rate Decision

- USA - FOMC Press Conference

Thursday, July 31, 2025

- China - Manufacturing PMI (Jul)

- Japan - BoJ Interest Rate Decision

- USA - Core PCE Price Index (YoY) (Jun)

- USA - Core PCE Price Index (MoM) (Jun)

- USA - Initial Jobless Claims

- USA - Chicago PMI (Jul)

Friday, August 1, 2025

- Eurozone - CPI (YoY) (Jul)

- USA - Average Hourly Earnings (MoM) (Jul)

- USA - Nonfarm Payrolls (Jul)

- USA - Unemployment Rate (Jul)

- USA - S&P Global Manufacturing PMI (Jul)

- USA - ISM Manufacturing PMI (Jul)

- USA - ISM Manufacturing Prices (Jul)

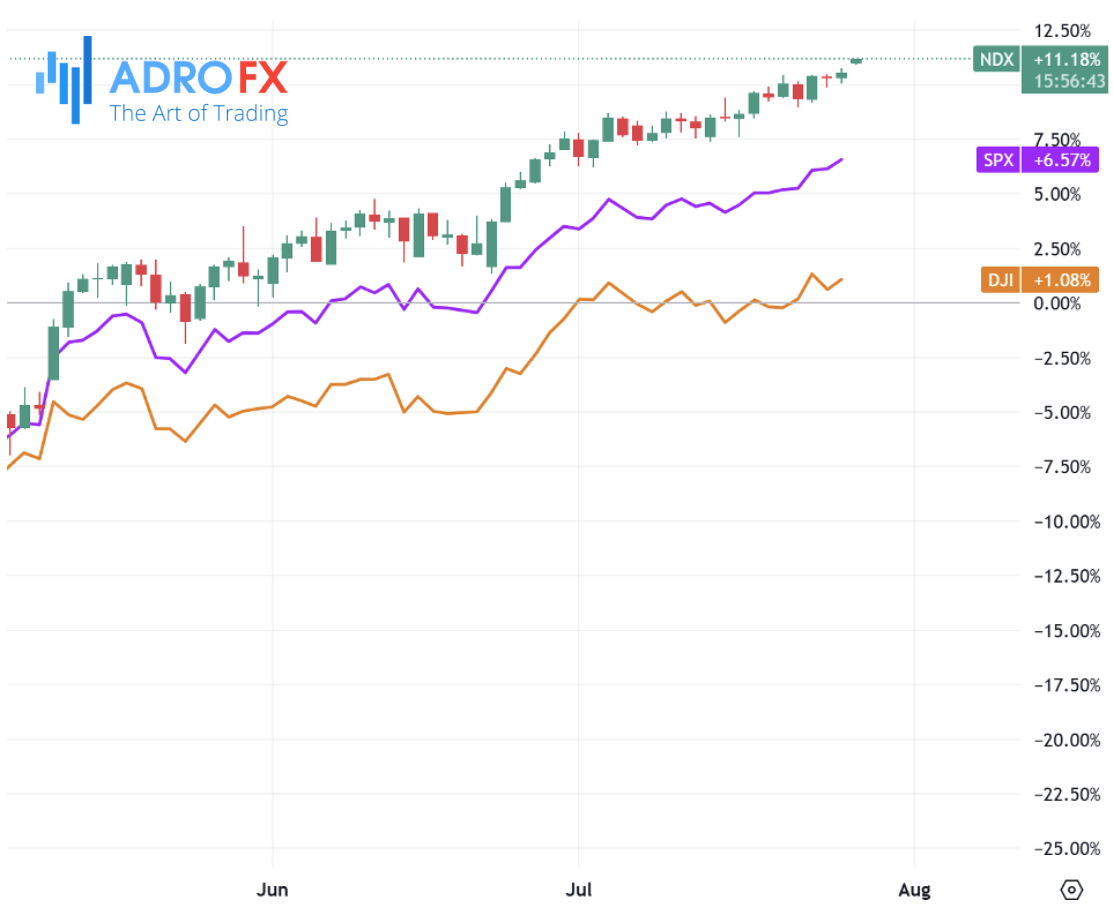

US equities climbed to new records at the close of last week, with the S&P 500 extending its winning streak to five consecutive sessions. The rally was supported by optimism around corporate earnings and signs of progress in trade negotiations between the US and its global partners.

On Friday, the Dow Jones Industrial Average posted a 208-point gain, or 0.5%, while the S&P 500 rose by 0.4%. The Nasdaq Composite edged up 0.2%, contributing to the positive momentum that has been building in recent weeks. Notably, nearly 83% of S&P 500 companies that have reported earnings so far have exceeded Wall Street’s expectations, reinforcing investor confidence.

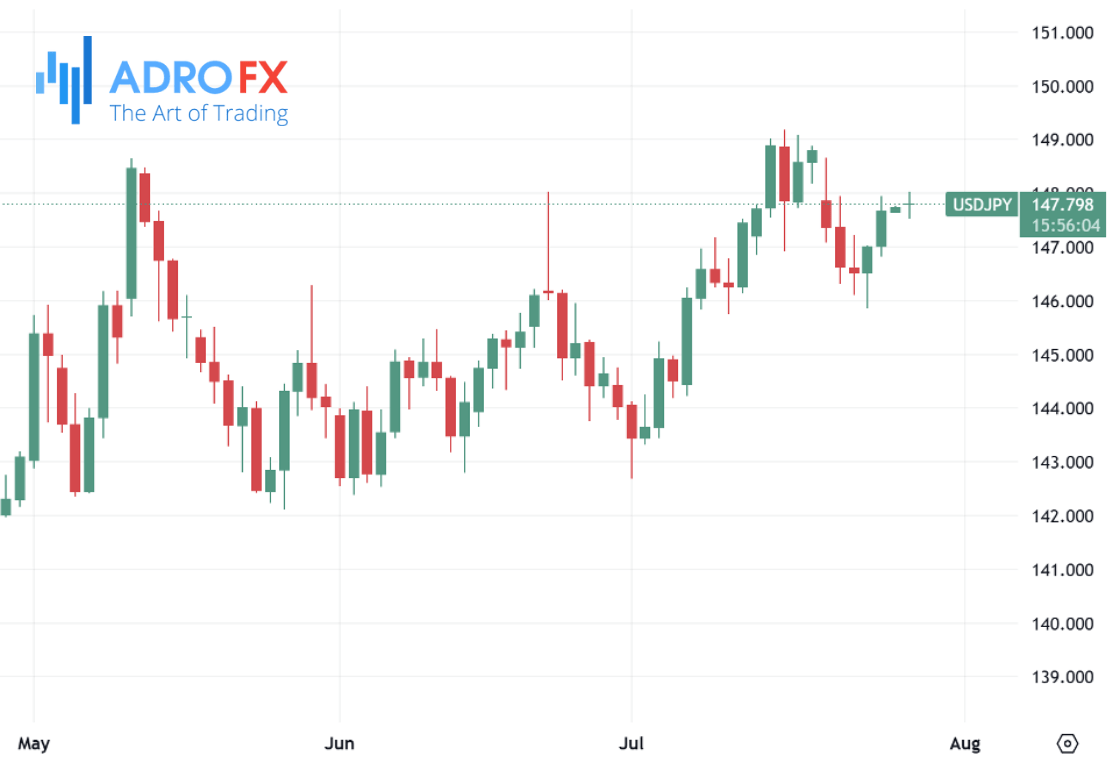

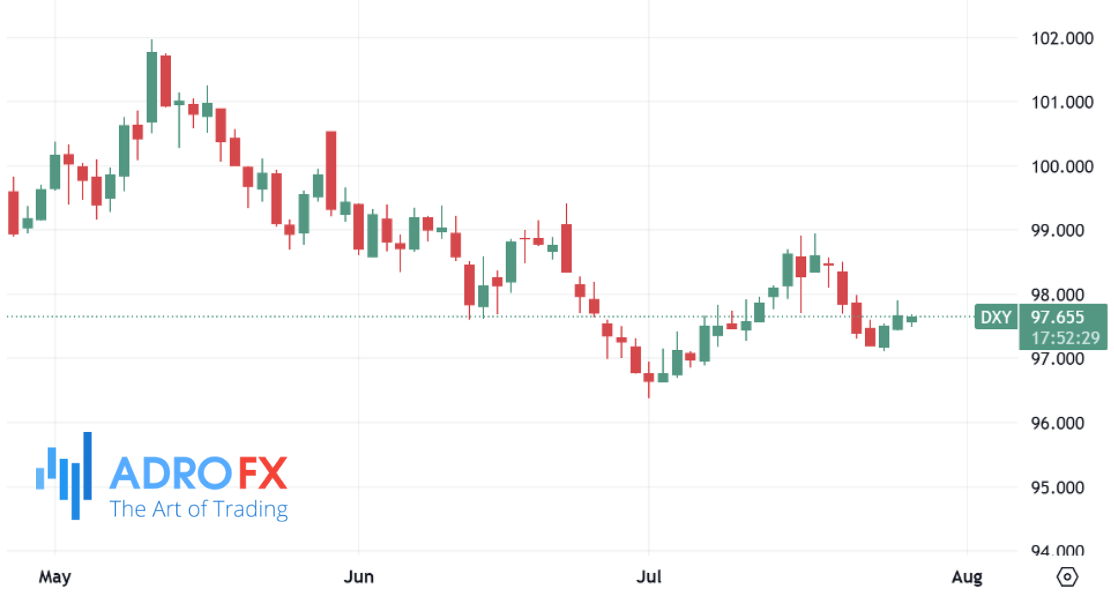

The outlook for global trade added another layer of interest as markets opened a new week. Developments in Asia, Europe, and North America all contributed to investor sentiment. The Japanese Yen bounced slightly after dipping to a one-week low against the US Dollar. A tentative trade deal between Japan and the United States opened up speculation that the Bank of Japan may consider a rate hike later this year, offering support for the yen. Meanwhile, the US Dollar began the week on a more cautious note as traders eyed central bank meetings and macroeconomic data releases.

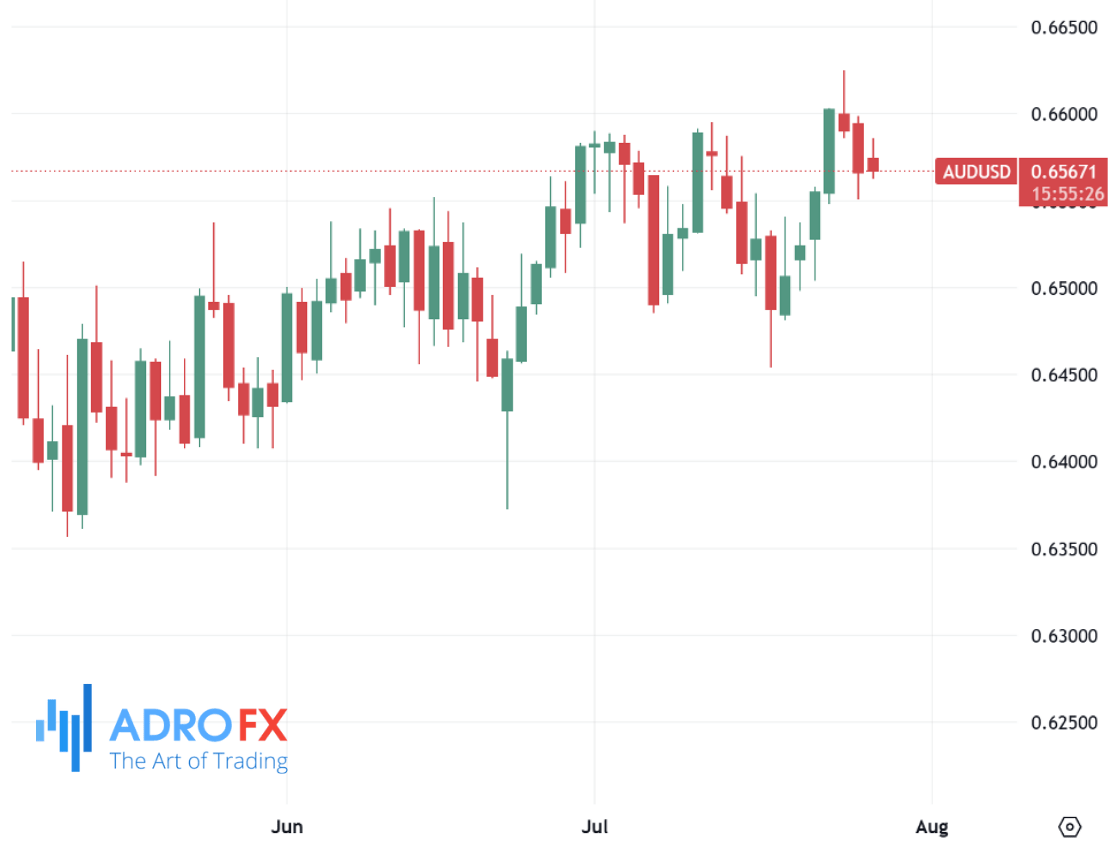

The Australian Dollar held its ground following two sessions of declines. Traders are closely watching for any updates from the anticipated meeting between US Treasury Secretary Scott Bessent and Chinese Vice Premier He Lifeng, which is scheduled to take place in Stockholm. Speculation suggests that the two countries could agree to extend their current tariff truce for another three months. Given the strong trade links between Australia and China, the outcome of these discussions could have significant implications for the AUD. Additionally, traders are bracing for the release of Australia’s second-quarter Consumer Price Index data, a key input into the Reserve Bank of Australia's next interest rate decision. RBA Governor Michele Bullock reiterated last week that inflation must remain low and stable, while also acknowledging growing global uncertainty.

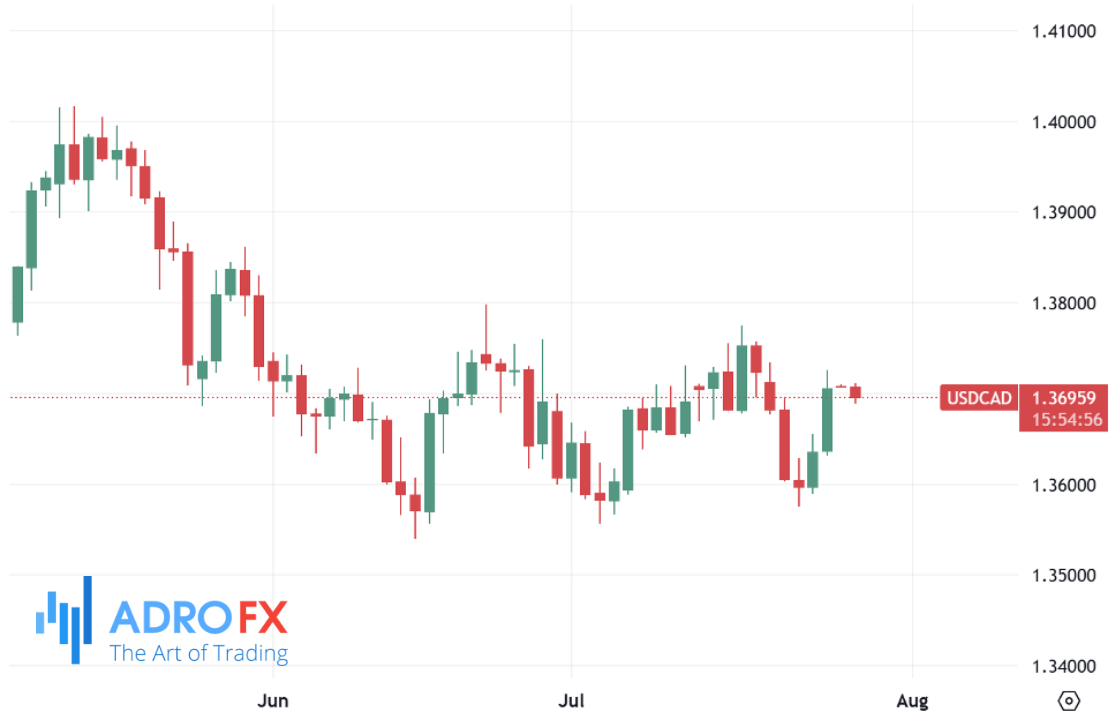

In North America, the Canadian Dollar made gains as the USD/CAD pair dipped after two days of upward movement. Investors are awaiting the US Federal Reserve’s monetary policy decision, which is due on Wednesday. The market widely expects the Fed to maintain its benchmark interest rate in the 4.25% to 4.50% range. However, the post-meeting press conference will be closely examined for any hints that rate cuts could begin as early as September. CME’s FedWatch tool indicates that investors are currently pricing in a 62% chance of such a cut.

Trade headlines also took center stage following comments from US President Donald Trump, who expressed doubt over reaching a trade agreement with Canada before the August 1 deadline. Trump suggested that a tariff may be imposed in place of an agreement, citing a lack of progress in negotiations. Canadian Prime Minister Mark Carney responded that Canada will not be pressured into accepting a disadvantageous deal, emphasizing that the government would prefer no agreement to a bad one.

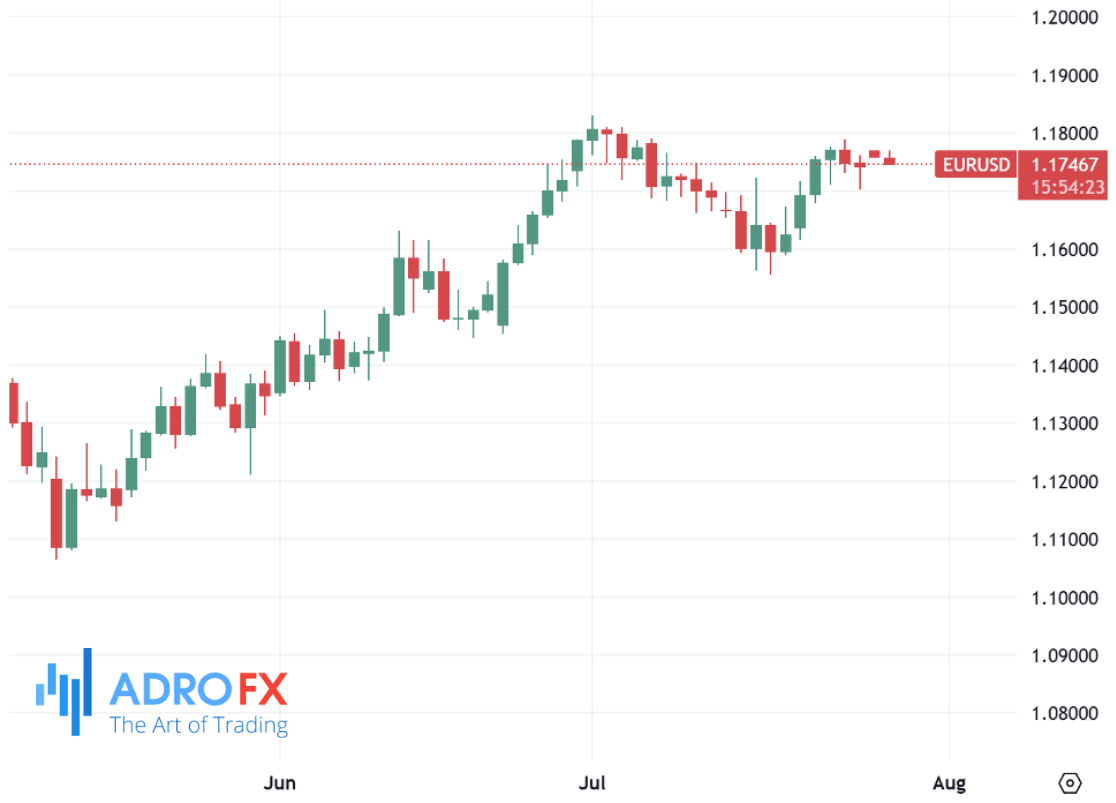

The Euro gained ground in early Monday trading following two sessions of losses. The EUR/USD pair traded around 1.1770 after news emerged that the US and the European Union had reached a framework trade agreement. The accord, which includes a 15% tariff on a range of European goods effective August 1, helped reduce fears of a broader transatlantic trade war. European Commission President Ursula von der Leyen said the EU had pledged $600 billion in US investment and would not impose retaliatory tariffs, signaling improved relations.

The European Central Bank left interest rates unchanged at its recent meeting, citing that disinflation is proceeding as anticipated. The ECB emphasized its data-driven approach and indicated that further clarity on the economic outlook is needed before any policy changes are announced.

In the UK, the British Pound showed signs of life after a recent dip, with GBP/USD climbing toward the 1.3450 range. Despite the modest rebound, traders remained hesitant due to the rising likelihood that the Bank of England may cut rates in August. Recent labor data has painted a soft picture, with the unemployment rate rising to 4.7%, a four-year high, and wage growth slowing to its weakest pace since 2022. These signals have overshadowed lingering inflation concerns and kept expectations for policy easing alive.

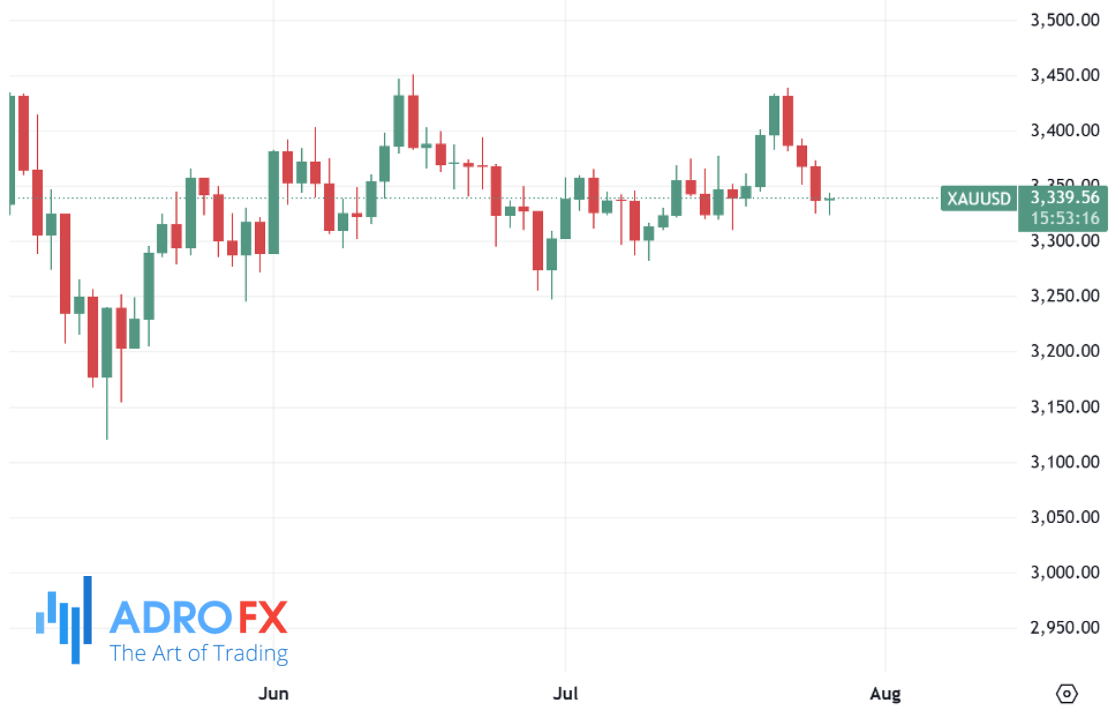

Gold prices also caught a bid in early Monday trading, moving higher near the $3,312 range as the US Dollar weakened. A combination of caution ahead of the Fed’s two-day policy meeting and subdued USD price action provided a lift to the precious metal. Investors are positioning carefully as they await not just the Fed's decision, but also a raft of important US economic reports, including the Q2 GDP estimate, PCE inflation data, and the July nonfarm payrolls. Each of these could influence expectations around future monetary policy and impact gold's direction.

Despite its gains, gold remains in a precarious position. Optimism surrounding the US-EU trade agreement has buoyed broader risk sentiment, which tends to weigh on demand for safe-haven assets like gold. Additionally, while President Trump has continued his public pressure campaign for lower interest rates, the Fed is widely expected to hold steady this week. Several key Fed officials, including Governor Chris Waller and Vice Chair Michelle Bowman, have recently signaled support for a rate cut, though the ultimate decision remains uncertain.

Traders are now laser-focused on the outcome of Wednesday’s Federal Open Market Committee meeting. While the consensus points to a hold in rates, any dovish signals from Fed Chair Jerome Powell could accelerate expectations for a rate cut in the months ahead. Political pressure from the White House has added complexity to the situation, raising concerns about the Fed's independence. Trump’s personal criticism of Powell has become more frequent, especially as inflation remains a thorny issue heading into the second half of the year.

The US Dollar, therefore, finds itself in limbo - caught between a resilient labor market that argues against immediate easing and external political and inflationary pressures that suggest a more accommodative stance may be needed soon. Traders are waiting for Powell’s tone and any forward guidance to gain a better read on the Fed’s trajectory. Until then, the USD may remain on the defensive, and markets could stay volatile as they navigate a dense calendar of economic events.

In the broader macroeconomic picture, investors are balancing robust corporate earnings with ongoing geopolitical uncertainties and central bank maneuvering. As key data and policy announcements approach, the next several days are expected to bring sharper movements across currencies, equities, and commodities, shaping the market narrative for the rest of the summer.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates