S&P 500 Ends Lower as Trade Tensions Flare with Canada and Global Tariff Risks Rise | Weekly Market Analysis

Key events this week:

Tuesday, July 15, 2025

- China - GDP (YoY) (Q2)

- USA - Core CPI (MoM) (Jun)

- USA - CPI (YoY) (Jun)

Wednesday, July 16, 2025

- UK - CPI (YoY) (Jun)

- USA - PPI (MoM) (Jun)

- USA - Crude Oil Inventories

Thursday, July 17, 2025

- Eurozone - CPI (YoY) (Jun)

- USA - Core Retail Sales (MoM) (Jun)

- USA - Initial Jobless Claims

- USA - Philadelphia Fed Manufacturing Index (Jul)

- USA - Retail Sales (MoM) (Jun)

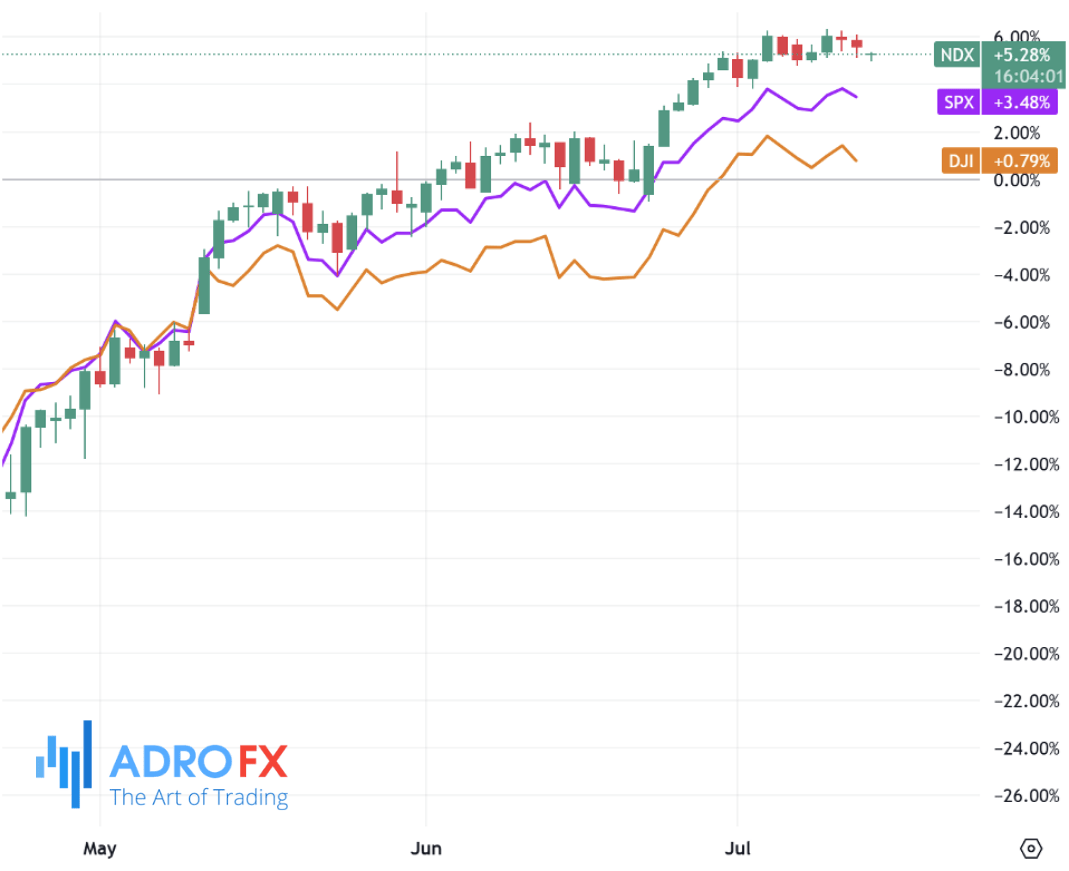

The S&P 500 ended Friday’s session in the red, marking a weekly decline as fresh trade tensions reignited fears of a broader global trade conflict. President Donald Trump’s announcement of a 35% tariff on Canadian imports set to take effect August 1 sent shockwaves through the markets, dragging major US indices lower.

The Dow Jones Industrial Average dropped 279 points, or 0.6%, while the S&P 500 declined 0.4%. The NASDAQ Composite lost 0.2%, pulling back slightly from its record highs earlier in the week.

The sudden escalation came after Trump issued a letter detailing the new duties against Canada, which he framed as a necessary move to rebalance trade and protect US industry. These tariffs are on top of existing sector-specific duties already rolled out earlier this year. With the global economy still adjusting to prior measures, investors reacted swiftly to the latest development, weighing the potential impact on supply chains, cross-border trade, and corporate earnings.

Adding to the uncertainty, Trump also stated plans to impose 30% tariffs on goods imported from both the European Union and Mexico, beginning the same day as the Canadian tariffs.

Markets fear that such aggressive moves could trigger retaliatory action and further strain diplomatic and economic relations between key trade partners. Safe-haven assets benefited as a result, with gold rallying to a three-week high around $3,374 during Monday’s Asian session. Demand for bullion surged as investors sought protection from growing market volatility.

However, gold’s momentum was somewhat tempered by a firm US dollar, which continues to hover near late-June highs amid waning expectations of a near-term rate cut by the Federal Reserve. With the Fed seen as likely to keep policy tight until inflation shows further signs of slowing, appetite for the non-yielding metal remained cautious. Traders are now turning their attention to upcoming US inflation data, which could influence the Fed’s stance and the near-term direction for both the dollar and gold.

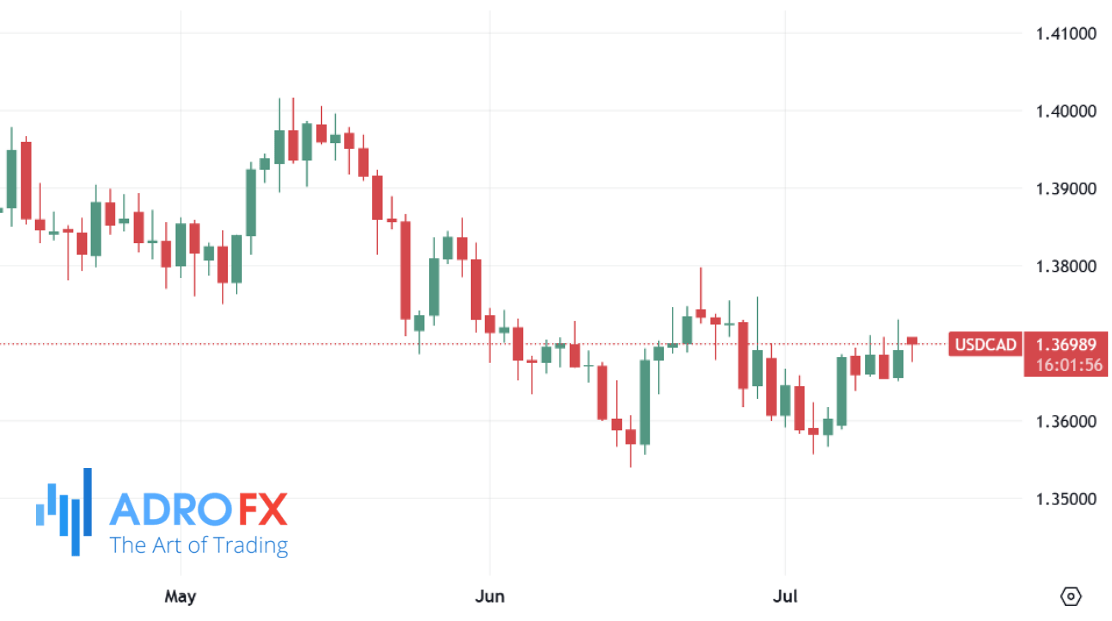

In the commodities-linked currency space, the Canadian dollar remained under pressure, despite a surprise in domestic labor market data. USD/CAD hovered around 1.3690 in Monday’s Asian trading, even as Statistics Canada reported a robust 83,100 new jobs added in June, far exceeding the 8,800 previously, and a drop in the unemployment rate to 6.9%, better than the expected 7.1%. The strong data cast doubt on whether the Bank of Canada will pursue any rate cuts at its upcoming meeting, with market pricing now showing just a 13% probability of easing this month.

Meanwhile, the Japanese yen struggled near three-week lows against the greenback. The USD/JPY pair found support as expectations for a Bank of Japan rate hike in the near term continued to fade. The yen was further pressured by political uncertainty in Japan and stronger-than-expected US economic data, which backed the Fed’s case for maintaining higher interest rates. While the BoJ is rumored to be considering an upward revision to its inflation forecasts later this month, those speculations failed to reverse the bearish sentiment toward the yen in the short term.

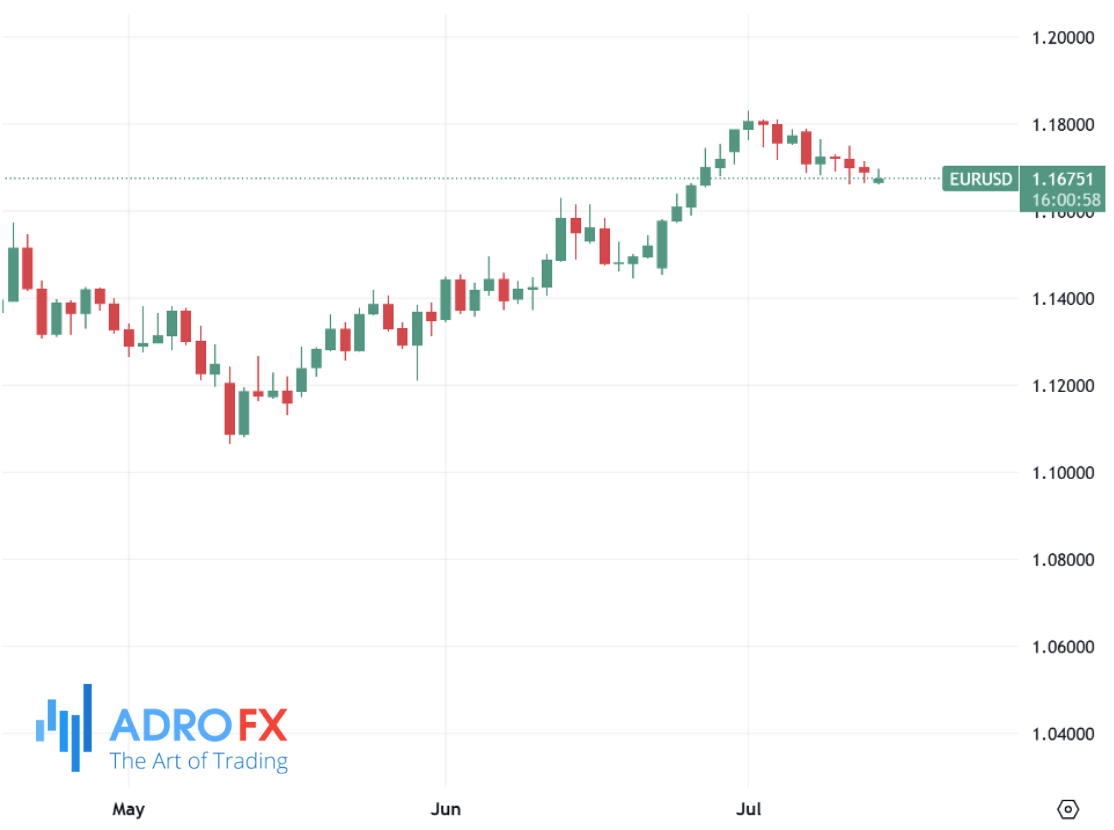

The euro staged a modest rebound, with EUR/USD trading near the 1.1700 level during Asian hours. The move came as the dollar softened slightly amid widespread concerns about Trump's expanding tariff agenda.

European Commission President Ursula von der Leyen reiterated a dual strategy of keeping diplomatic channels open while quietly preparing countermeasures if talks fail. German Chancellor Friedrich Merz voiced concerns over the impact of a 30% US tariff, particularly on Germany’s export-heavy manufacturing sector, and called for renewed efforts to reach a deal before the August 1 deadline.

Elsewhere in the Asia-Pacific region, the Australian dollar retreated against the US dollar following the release of mixed trade data from China, Australia’s largest trading partner. AUD/USD extended its losses as China’s trade surplus narrowed to CNY585.96 billion in June, down from CNY743.56 billion in May. Despite improvements in export growth, the overall slowdown in trade momentum raised concerns about external demand. In USD terms, China’s trade surplus came in stronger than expected at $114.77 billion, but the data failed to lift broader risk sentiment amid global uncertainty.

Attention also turned to the Reserve Bank of Australia, which may opt to keep interest rates steady in August. Governor Michele Bullock flagged inflationary risks driven by high labor costs and low productivity, while Deputy Governor Andrew Hauser highlighted the unpredictable fallout from a prolonged global trade war. Rate markets are now mixed on the RBA’s next move, with inflation forecasts and international developments heavily influencing outlooks.

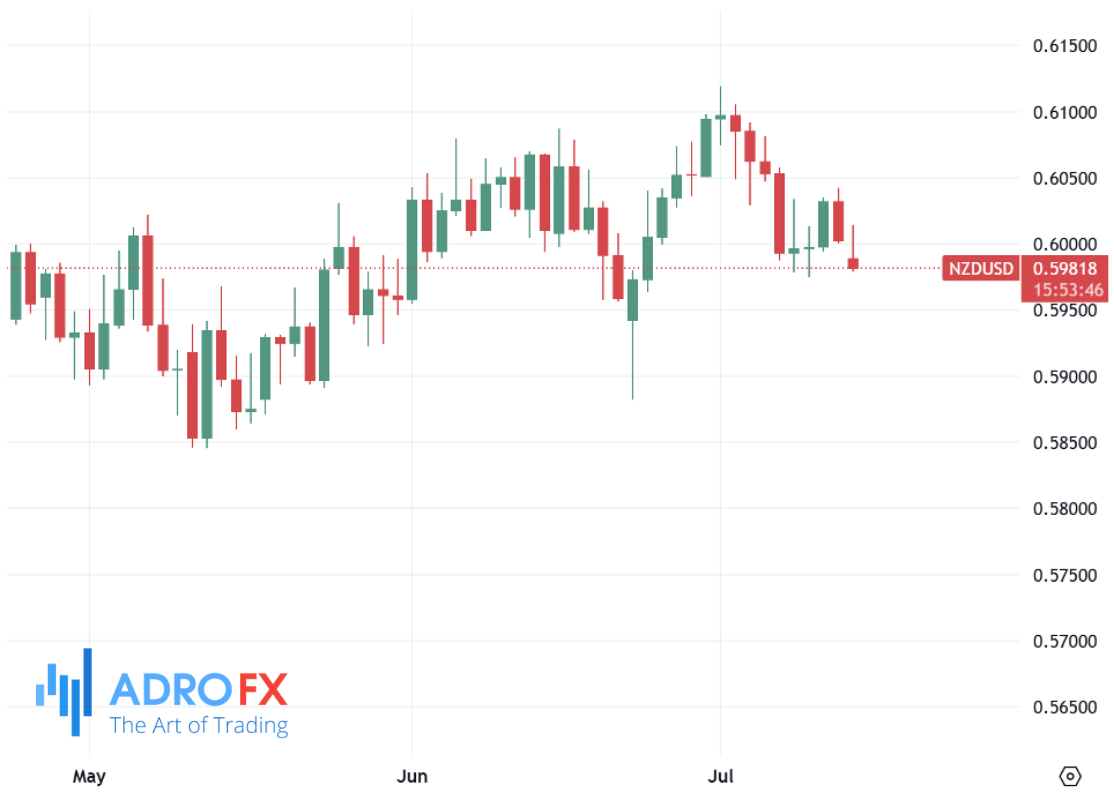

The New Zealand dollar also faced pressure as NZD/USD slipped toward 0.6035. Market participants remain cautious ahead of the Reserve Bank of New Zealand’s rate decision and the release of the Federal Open Market Committee (FOMC) minutes later this week. While the RBNZ is widely expected to leave rates unchanged, lingering uncertainty around tariff-related slowdowns and global risk sentiment continues to weigh on the kiwi. Central bank officials in New Zealand have emphasized the potential consequences of continued trade frictions, especially given the nation’s close economic ties with China.

Traders across major markets now look ahead to critical economic data that could set the tone for monetary policy through the second half of the year. On Tuesday, the US will release June consumer inflation figures, followed by the Producer Price Index on Wednesday. These reports will be closely monitored by investors and policymakers alike, especially with over 50 basis points of rate cuts still priced in for the Fed by December. Additionally, speeches from key FOMC members may help clarify the central bank’s trajectory in the wake of solid jobs data and persistent inflation concerns.

The upcoming earnings season will also come into sharper focus, with several major banks - including JPMorgan Chase, Wells Fargo, Citigroup, and Bank of New York Mellon - scheduled to report results on Tuesday. Investors will closely analyze financials to gauge whether corporate America is weathering economic headwinds and to what extent profitability may be impacted by slowing growth or higher funding costs.

While markets remain vulnerable to policy shocks, geopolitical risk, and fluctuating rate expectations, the underlying resilience of the US labor market and corporate performance may offer some cushion. Still, with trade tensions again dominating headlines and central banks walking a fine line, investors are likely to stay cautious, positioning carefully ahead of another data-heavy and politically sensitive week.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates