Global Markets Lifted by Growing Rate-Cut Optimism as Currency Moves and Commodity Swings Shape a Volatile Start to the Week | Weekly Market Analysis

Key events this week:

Tuesday, November 25, 2025

- USA - Core Retail Sales (MoM) (Sep)

- USA - PPI (MoM) (Sep)

- USA - Retail Sales (MoM) (Sep)

- USA - CB Consumer Confidence (Nov)

Wednesday, November 26, 2025

- New Zealand - RBNZ Interest Rate Decision

- UK - Autumn Forecast Statement

- USA - Durable Goods Orders (MoM) (Sep)

- USA - GDP (QoQ) (Q3)

- USA - Initial Jobless Claims

- USA - Core PCE Price Index (MoM) (Sep)

- USA - Core PCE Price Index (YoY) (Sep)

- USA - New Home Sales (Sep)

- USA - Crude Oil Inventories

Friday, November 28, 2025

- USA - Chicago PMI (Nov)

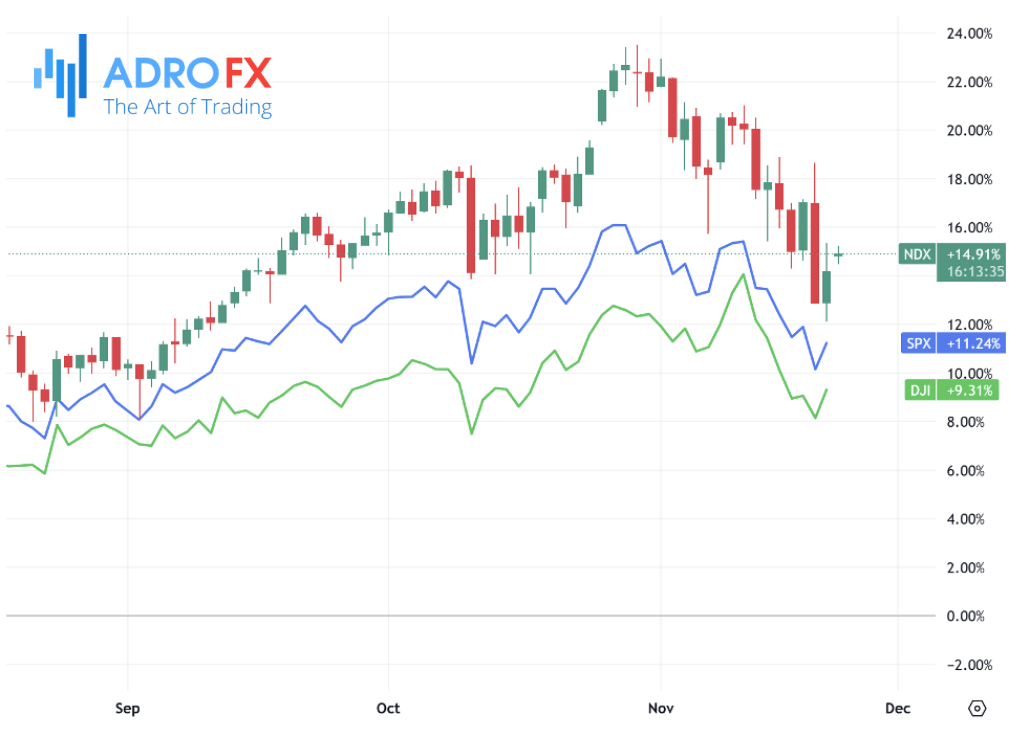

A wave of optimism swept through U.S. equities on Friday as traders sharpened their expectations for a Federal Reserve rate cut in December, sending major indices higher and briefly igniting enthusiasm across the tech sector.

The S&P 500 surged, the Dow Jones Industrial Average climbed nearly 500 points, and the Nasdaq Composite pushed higher in tandem, each advancing around 1.6%.

Nvidia stole much of the attention as its trading session turned into a rollercoaster. The chipmaker swung sharply between gains and losses after a report suggested U.S. officials were considering softening restrictions on exports of its H200 AI chips to China. The potential shift, still in early internal discussions according to Bloomberg’s reporting, injected fresh energy into AI-related names — at least momentarily. Enthusiasm fizzled later in the day, reflecting how fragile sentiment has become in a sector many fear is beginning to stretch too far. Even Michael Burry, known for his prescient warning ahead of the 2008 financial crisis, recently cautioned that true underlying demand for AI technology remains far below sky-high valuations.

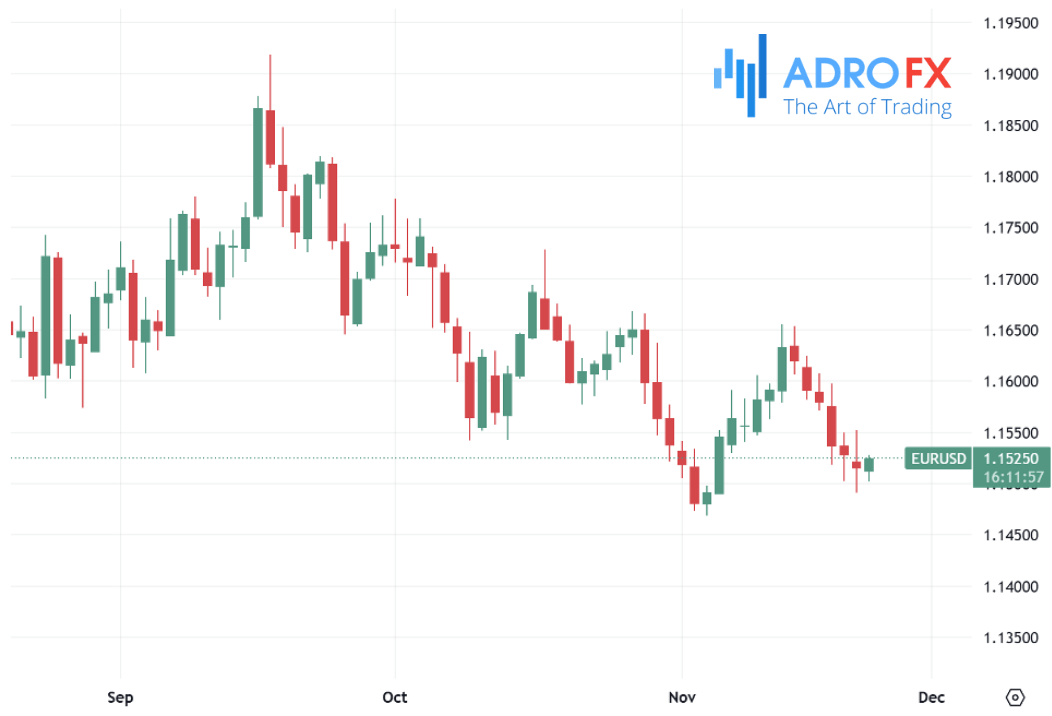

While U.S. equities found solid footing, currency markets entered the new week in a more cautious but reactive mood. The euro strengthened against the dollar, pushing EUR/USD toward 1.1525 as the greenback softened under the weight of rising expectations that the Fed is preparing to cut rates. That shift in tone began with comments from New York Fed President John Williams, who signaled that slowing labor market dynamics may pose a more serious risk than residual inflation pressures. His suggestion that the next move could be downward for interest rates encouraged traders to reprice the December meeting more dovishly.

Other Fed officials remained careful in their messaging. Boston’s Susan Collins noted she would require a “high bar” to support further easing, while Dallas Fed President Lorie Logan argued that keeping rates steady for longer would allow policymakers to better gauge the economy’s real response to restrictive monetary policy. The mixed guidance created a delicate backdrop ahead of U.S. data releases this week, particularly the September PPI and Retail Sales figures, both expected to influence the dollar’s next directional move.

Across the Atlantic, the European Central Bank appears firmly committed to keeping rates unchanged well into 2025 or even 2026, according to a November poll of economists. With inflation largely contained and the regional economic outlook stabilizing, the ECB is signaling that its current stance remains appropriate for now. President Christine Lagarde reiterated on Friday that the central bank will continue monitoring inflation risks closely and stands ready to adjust policy if needed. Her steady, unhurried approach may offer some support to the euro against lower-yielding counterparts such as the yen.

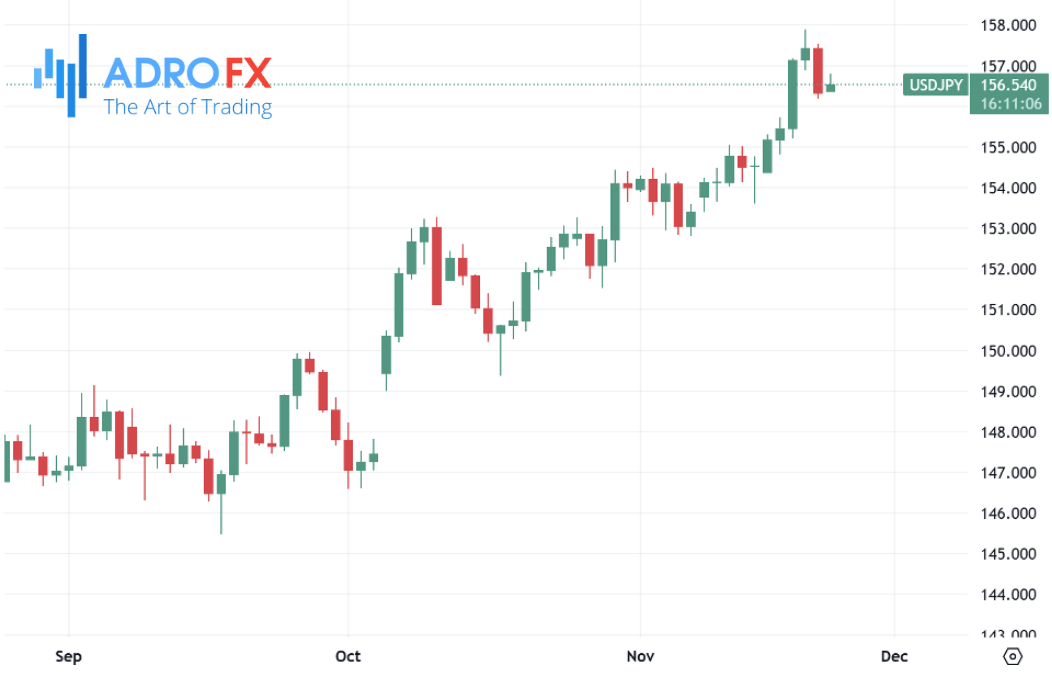

Japan, on the other hand, continues to grapple with deepening pressure on its currency. The yen remained weak through Monday’s Asian session as concerns grow about Japan’s deteriorating fiscal position under Prime Minister Sanae Takaichi’s pro-stimulus agenda. Adding to the pressure is the perception that the Bank of Japan is in no hurry to tighten policy amid political pushback against rate hikes. A generally positive risk tone in markets further undermined demand for the safe-haven JPY.

Still, Japanese officials are not sitting quietly. Finance Minister Satsuki Katayama revived speculation about possible intervention to stem excessive yen weakness, while government panel members echoed similar concerns over the weekend. Those signals helped slow the yen’s decline, though not enough to reverse the broader momentum favoring USD/JPY buyers at the start of the week.

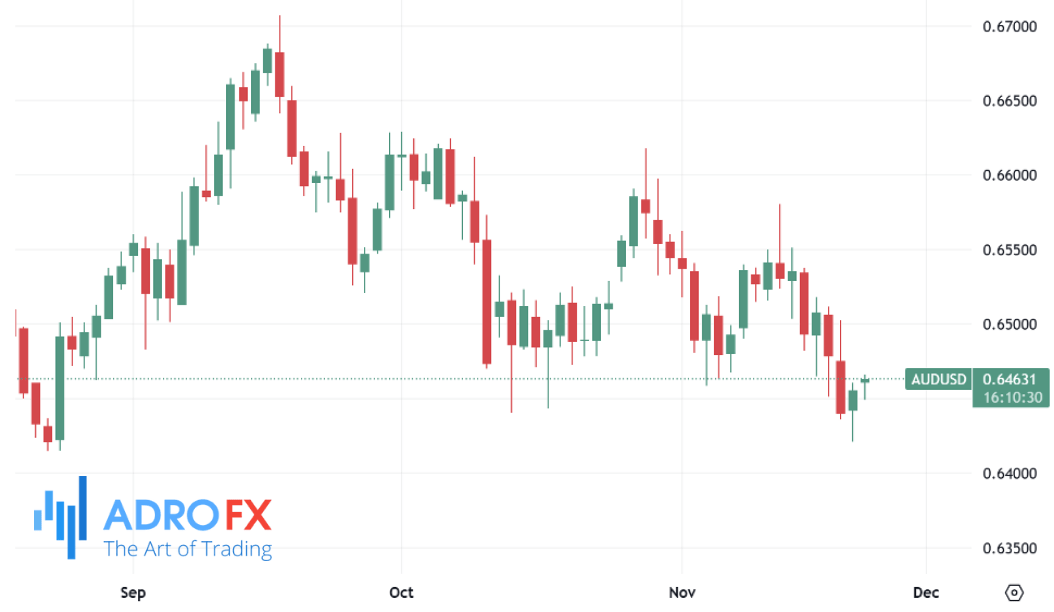

The Australian Dollar attempted to hold firm as markets turned their attention to a key inflation release expected midweek. Australia’s first “complete” monthly CPI reading for October is anticipated to guide expectations for the Reserve Bank of Australia’s policy outlook. Traders have been leaning toward a steady-rate narrative after the RBA’s November minutes emphasized patience. With monetary policy effects still working their way through the system, officials signaled they are reluctant to overreact to short-term data fluctuations. Assistant Governor Sarah Hunter reiterated that single-month readings can be noisy and highlighted the importance of evaluating labor-market performance and broader supply-capacity trends.

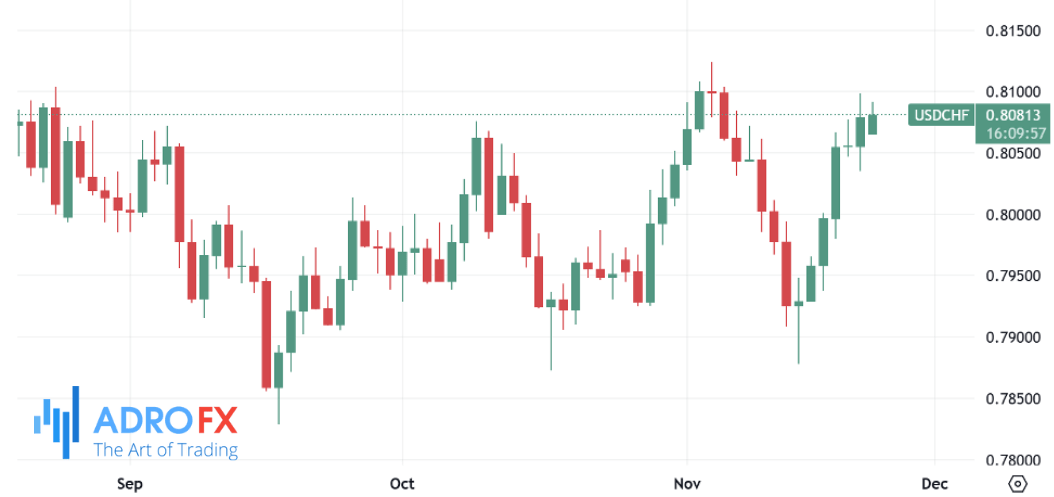

USD/CHF continued its winning streak for a seventh consecutive session, stabilizing around 0.8080 in Asia. However, the upside may face limitations as the Swiss franc remains supported by expectations that the Swiss National Bank will refrain from cutting rates in December. Rising inflation forecasts further justify a cautious stance. Additionally, CHF received an unexpected tailwind from a fresh tariff agreement struck between Switzerland and the Trump administration, which lowers the U.S. tariff rate from 39% to 15% — an adjustment seen as potentially boosting Switzerland’s economic recovery following a contraction last quarter.

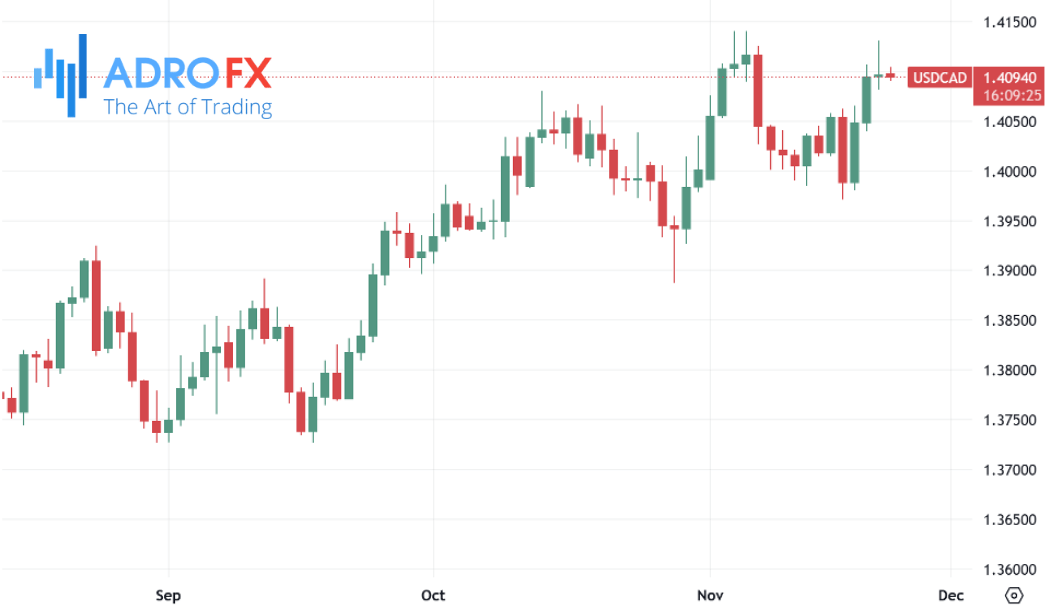

Over in North America, USD/CAD softened for a second straight session as the U.S. dollar weakened on rate-cut speculation. The Canadian dollar, however, struggled to fully capitalize due to falling oil prices. WTI crude extended its losing streak to a fourth session, sliding toward the $58 mark after reports hinted the U.S. is pushing for progress on a Russia-Ukraine peace framework — an outcome that could increase supply into an already crowded crude market. Canada’s economic picture didn’t help either: Statistics Canada confirmed that September retail sales dropped 0.7%, erasing the prior month’s gain, largely driven by declining auto sales.

The British pound started the week under pressure once again. GBP/USD hovered just below 1.3100 as the U.S. dollar attempted to stabilize. The pound’s broader weakness reflects lingering uncertainty ahead of Wednesday’s UK Autumn Budget and rising market conviction that the Bank of England may cut rates as early as next month. With traders unwilling to take big positions before seeing the government’s fiscal roadmap, the pair remained directionless but defensive.

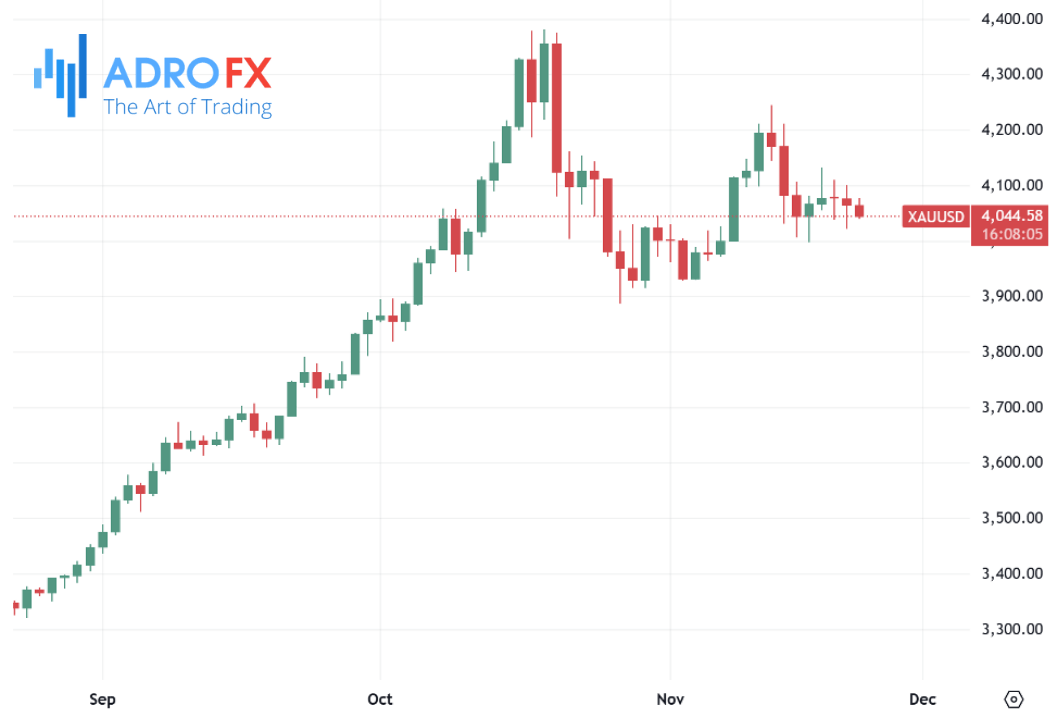

Gold prices slipped early Monday, falling below $4,050 without building any strong bearish momentum. The metal remains locked in a tight range, caught between geopolitical stress — including intensifying conflict dynamics in both the Russia-Ukraine and Middle East regions — and anticipation of key U.S. macro releases. With Q3 GDP estimates and the Fed’s preferred PCE inflation index both set for release later this week, traders appear content to wait for clearer signals before committing to a new trend.

Across equities, currencies, and commodities, the week begins with markets balanced delicately between optimism over impending policy easing and caution over geopolitical friction and uneven economic data. Investors around the world now turn toward upcoming inflation reports, GDP readings, and policy remarks to shape the next major move in global risk appetite.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates