Dow Jones Slips as Weak Consumer Sentiment and Data Delays Cloud Market Outlook | Weekly Market Analysis

Key events this week:

Monday, November 10, 2025

- Japan - BoJ Board Member Nakagawa Speaks

- UK - FOMC Member Daly Speaks

Wednesday, November 12, 2025

- USA - 10-Year Note Auction

Thursday, November 13, 2025

- UK - GDP (QoQ) (Q3)

- UK - GDP (YoY) (Q3)

- UK - GDP (MoM) (Sep)

- USA - Core CPI (MoM) (Oct)

- USA - CPI (MoM) (Oct)

- USA - CPI (YoY) (Oct)

- USA - Initial Jobless Claims

- USA - Crude Oil Inventories

- USA - 30-Year Bond Auction

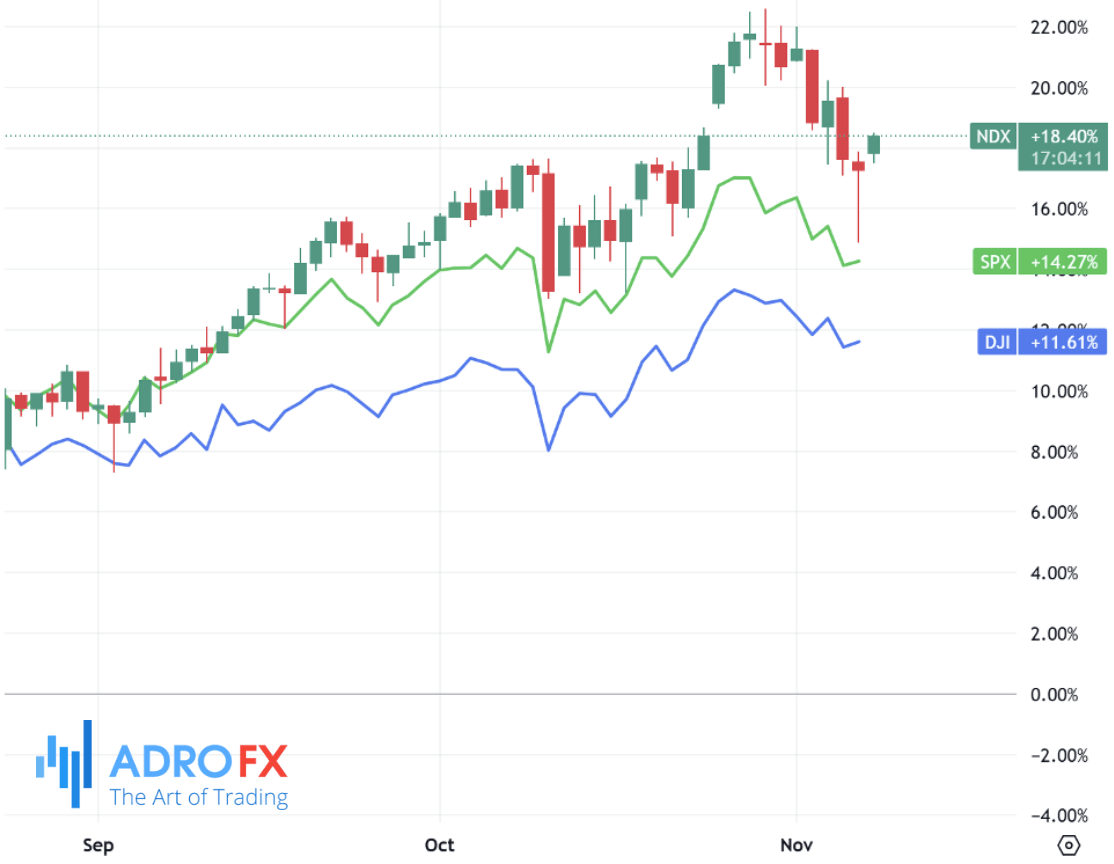

The Dow Jones Industrial Average slid again on Friday, briefly falling below the 46,800 mark for the first time in nearly three weeks before clawing its way back to end the session almost flat. Investors faced a tough mix of falling AI-related stocks and disappointing consumer sentiment data, both weighing on confidence in the broader economy. Although the market showed some resilience toward the close, sentiment remains fragile amid ongoing uncertainty over U.S. economic conditions and a record-long government shutdown that continues to block key data releases.

By the end of trading, the Dow had gained just 79 points, or about 0.2%, while the S&P 500 rose a modest 0.1%. The Nasdaq Composite, pressured by another round of profit-taking in major tech names, slipped 0.2%.

A major source of unease came from the University of Michigan’s latest Consumer Sentiment report, which showed Americans growing increasingly pessimistic about the economic outlook. The headline Consumer Sentiment Index dropped sharply to 50.3 from 53.6, while the Consumer Expectations Index fell to 49 from 50.3 — both among the lowest readings seen in recent years. These results indicate that U.S. households are becoming more concerned about jobs, income stability, and inflation heading into the year’s final quarter.

Despite strong spending among higher-income groups, the data reveal growing stress among lower- and middle-income consumers, who are struggling to keep up with rising prices and limited wage growth. This uneven dynamic has masked the depth of economic strain that lies beneath the surface, making it difficult for markets to gauge the true strength of U.S. demand.

Meanwhile, the federal government shutdown — now the longest in U.S. history — continues to disrupt the release of key economic indicators, including the much-anticipated nonfarm payrolls (NFP) report. With official labor and inflation data unavailable, investors are forced to rely on private-sector reports and retail data to estimate the economy’s trajectory. President Donald Trump, already presiding over the previous longest shutdown, now faces mounting political and economic pressure as the stalemate stretches on, raising further doubts about the near-term policy outlook.

Private data sources, however, paint a concerning picture. According to analytics firm DataWeave, major U.S. retailers such as Target (TGT) and Walmart (WMT) have seen their average prices rise by roughly 5.5% and 5.3%, respectively. These figures underscore how inflation’s impact remains uneven across different consumer categories — with essentials like groceries and household goods experiencing the steepest increases. While official CPI numbers often rely on averaged estimates, real-world data suggest that many households continue to face persistent cost pressures.

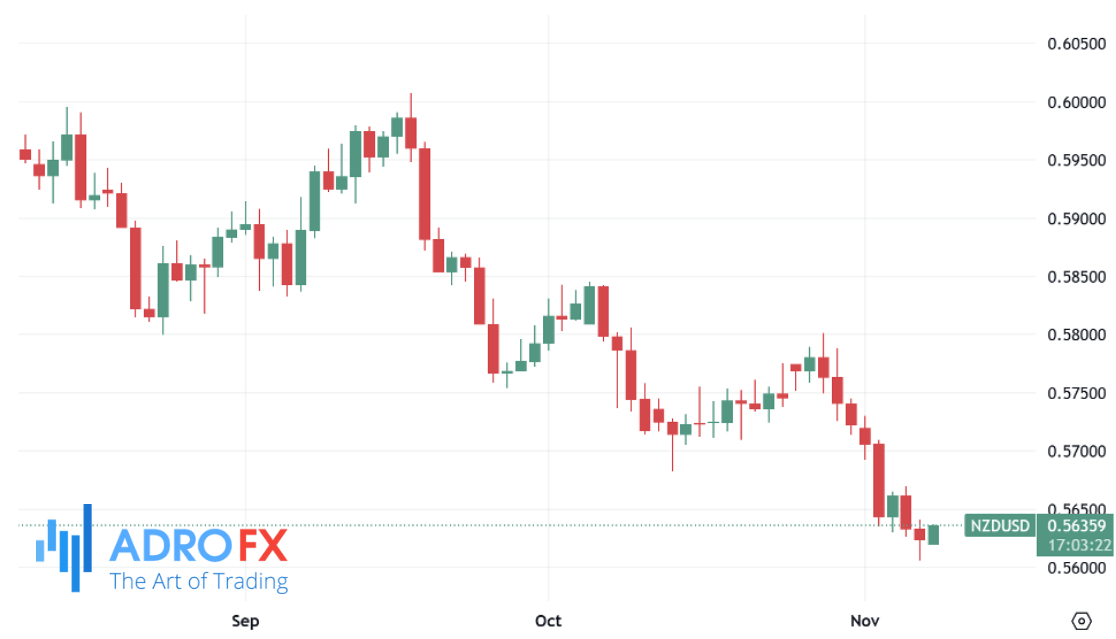

In the currency market, the New Zealand dollar managed to rebound modestly after falling to a seven-month low of 0.5605 in the previous session. During Monday’s Asian session, NZD/USD traded near 0.5630, supported by better-than-expected economic figures from China — New Zealand’s largest trading partner.

China’s Consumer Price Index rose 0.2% year-on-year in October, rebounding from a 0.3% decline in September and surpassing expectations for no growth. Monthly inflation also improved slightly, while producer prices continued to contract but at a slower pace. This mild recovery in Chinese inflation data helped lift market sentiment toward Asia-Pacific currencies. Additionally, easing U.S.-China trade tensions provided another boost after Beijing temporarily suspended its restrictions on exports of certain strategic materials, including gallium and germanium, through November 2026.

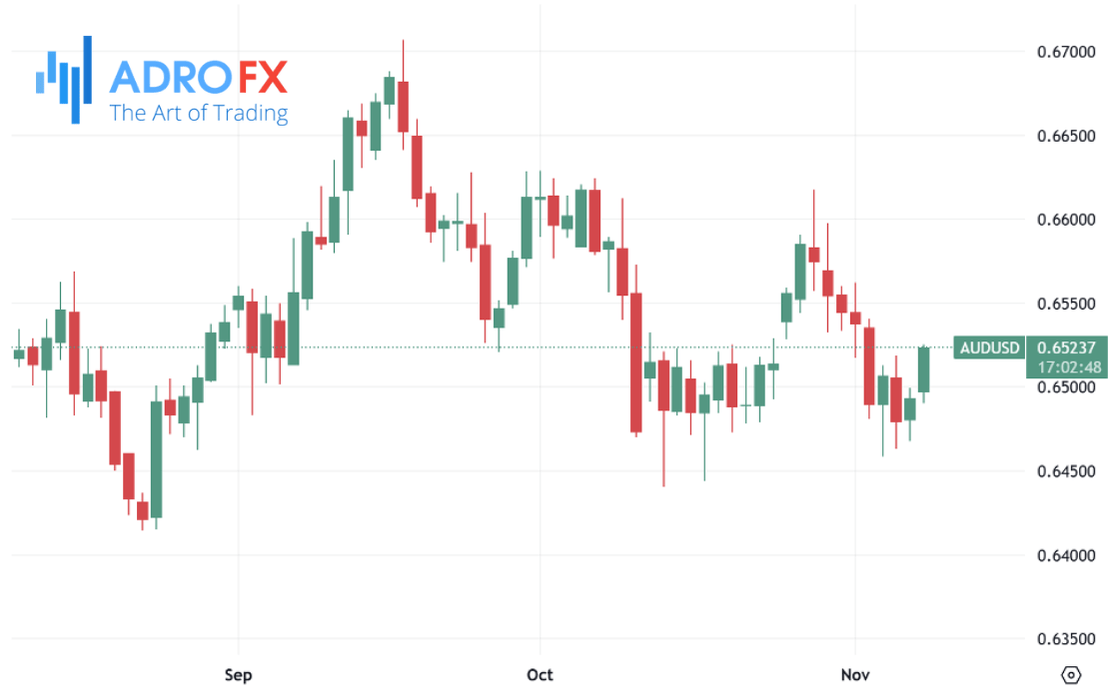

The Australian dollar also strengthened for a second straight session, with AUD/USD edging higher in early Monday trading. Support came from recent remarks by Reserve Bank of Australia Deputy Governor Andrew Hauser, who noted that the country’s monetary policy remains in a delicate phase. He emphasized that domestic demand continues to run slightly above potential, leaving little room for the central bank to loosen policy without risking renewed inflation pressures. Hauser’s comments reinforced expectations that the RBA will maintain its tightening stance for now, giving the Aussie dollar some extra lift.

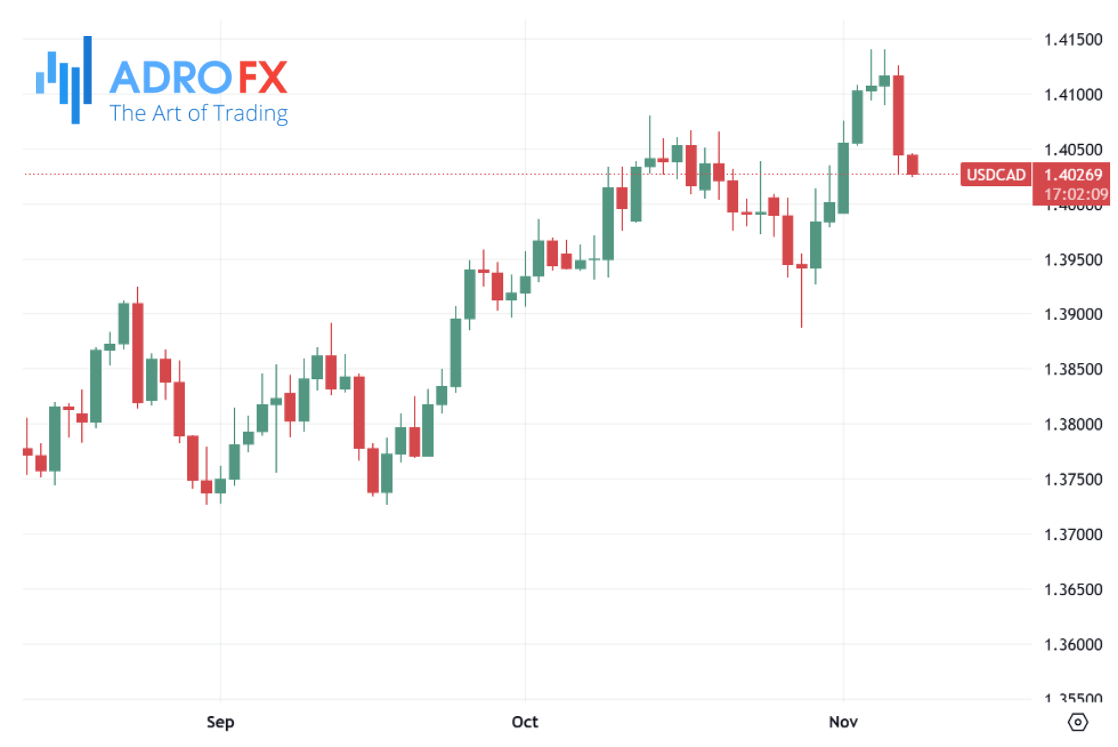

Across North America, the Canadian dollar gained ground following an upbeat employment report. USD/CAD slipped about 0.12% to trade near 1.4030 during Asian hours on Monday. Data from Statistics Canada showed the economy unexpectedly added 66,600 jobs in October, far surpassing expectations for a small decline of 2,500. The solid labor market performance suggests continued resilience in Canada’s economy despite global headwinds, helping the Loonie outperform most of its peers.

In contrast, the British pound lost momentum against the U.S. dollar, with GBP/USD easing to around 1.3150 after three sessions of gains. The dollar regained some strength amid signs that the record-breaking U.S. government shutdown could soon end, giving investors a modest reason for optimism. Traders are also awaiting a speech by Bank of England Chief Economist Clare Lombardelli for clues on the next policy moves.

Last week, the BoE opted to hold interest rates steady at 4.0%, citing the need for caution ahead of the upcoming Autumn Budget. Governor Andrew Bailey hinted that rate cuts are likely in the coming months, potentially before Christmas, but stressed that the timing will depend on inflation trends. The central bank continues to face the challenge of supporting growth without reigniting price pressures.

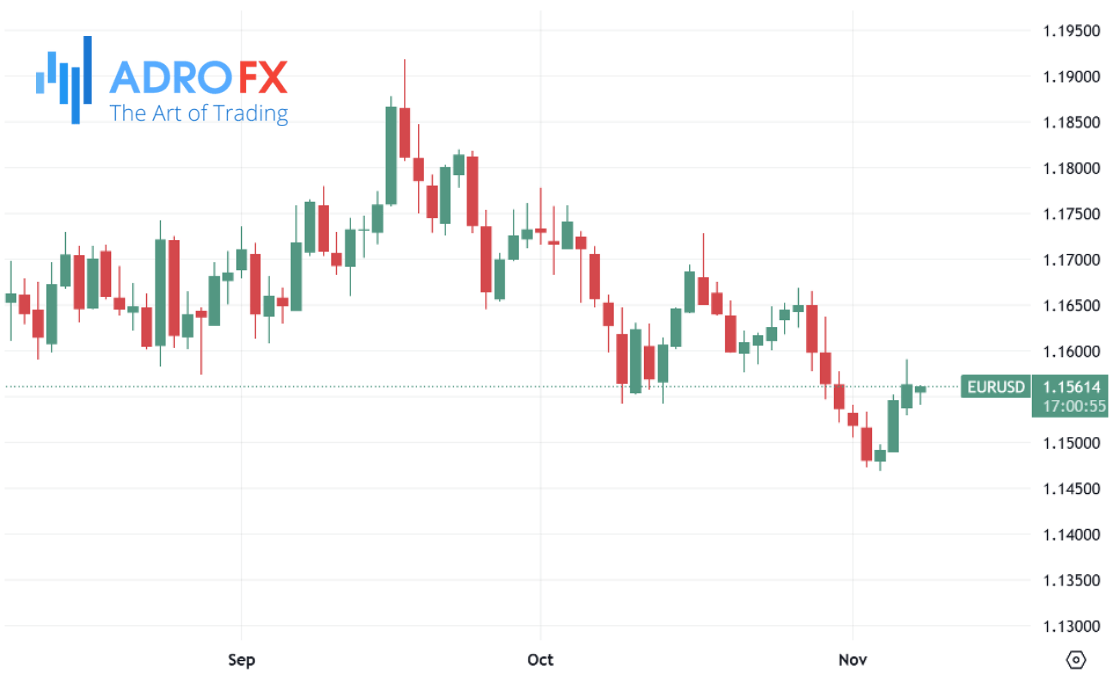

The euro also remained under pressure, with EUR/USD trading near 1.1550 after three consecutive days of losses. The pair may soon find support as markets adjust expectations for the European Central Bank’s next policy steps. While most analysts expect the ECB to keep rates unchanged for an extended period, the likelihood of a near-term rate cut has fallen sharply — from over 80% in October to roughly 45% by September 2026.

ECB policymakers have maintained a cautious tone, emphasizing flexibility and vigilance. Governing Council member Joachim Nagel warned against complacency on inflation, while Vice President Luis de Guindos noted that any dip in inflation below the 2% target is likely to be temporary. These remarks suggest that the ECB will stay on hold until it sees clearer signs of sustained price stability.

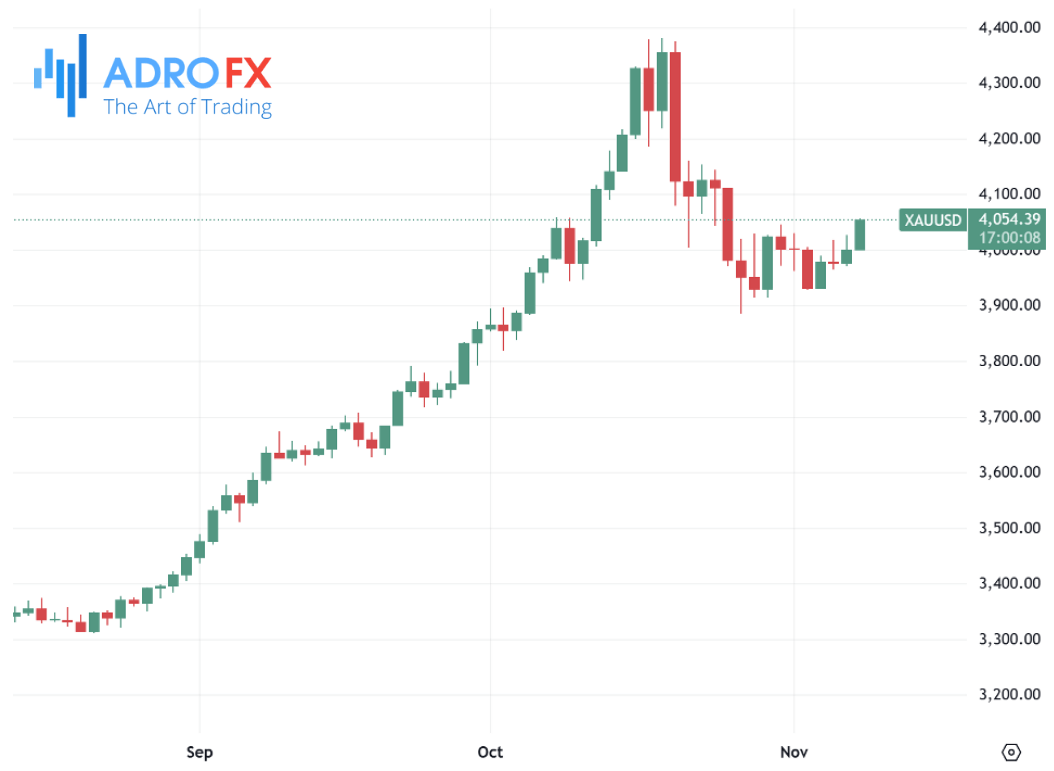

In commodities, gold prices climbed above $4,050 during early European trading on Monday, supported by renewed uncertainty surrounding the U.S. economy. Investors are positioning cautiously ahead of the upcoming U.S. Consumer Price Index release, which will offer fresh insight into inflation trends. Analysts expect headline CPI to rise by 0.2% month-over-month in October, while the core measure is forecast to increase by 0.3%.

Additionally, Friday’s U.S. retail sales report will be closely watched for further clues about consumer strength — a key driver of inflation expectations. For now, gold remains a preferred hedge against both economic and political instability, with traders favoring safety amid ongoing fiscal disruptions and fading consumer optimism.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates