Wall Street's Major Indices Rally as Nasdaq Records Historic Gain and Apple Hits $3 Trillion Market Valuation | Daily Market Analysis

Key events:

- USA - Independence Day - Early close at 13:00

- UK - Manufacturing PMI (Jun)

- USA - ISM Manufacturing PMI (Jun)

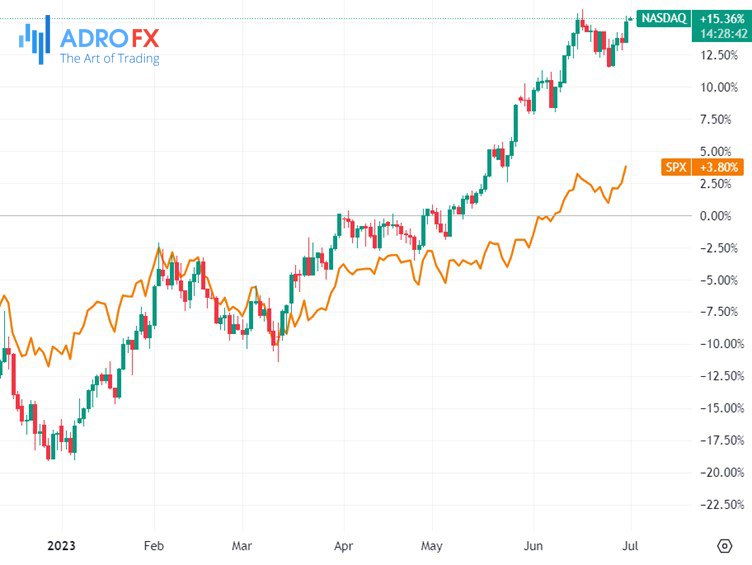

Friday saw a solid advance in Wall Street's three major indices, with the Nasdaq, known for its focus on technology stocks, recording its largest first-half gain in 40 years. This positive momentum coincided with Apple achieving a market valuation of $3 trillion for the first time since January 2022. Apple's stock closed at $193.97, up 2.3%, after reaching a record high of $194.48. The company's performance was buoyed by growing investor enthusiasm for growth stocks and confidence in Apple's ability to succeed in new markets.

Investors showed increased interest on the final day of the second quarter, driven by signs of cooling US inflation as indicated by closely monitored measures tracked by the Federal Reserve. A report from the Commerce Department revealed that the Personal Consumption Expenditures (PCE) index rose by 3.8%, lower than April's 4.3% figure. Excluding volatile food and energy prices, the core PCE index increased by 0.3%, down from the previous month's 0.4%.

The data sparked hope that the Federal Reserve's rate-hiking cycle could be nearing its end. The decline in Treasury yields in response to the easing inflationary pressure contributed to the positive market sentiment. Burns McKinney, a portfolio manager at NFJ Investment Group in Dallas, Texas, highlighted the impact of falling yields on market conditions.

The Nasdaq achieved its strongest first-half performance in 40 years, delivering a gain of over 31%. Specifically, the Nasdaq 100 index, which includes top technology stocks, experienced its largest first-half gain on record, surging by approximately 39%.

On Friday, the S&P 500's growth index rose by 1.4%. Apart from Apple, other popular stocks among investors, such as Microsoft, Nvidia, Amazon, and Meta Platforms, made significant contributions to the S&P 500's positive performance. These stocks recorded gains ranging from 1.6% to 3.6%, building on their impressive rallies driven by strong earnings and the growing interest in artificial intelligence.

As we enter the first full week of July, an eventful economic calendar awaits.

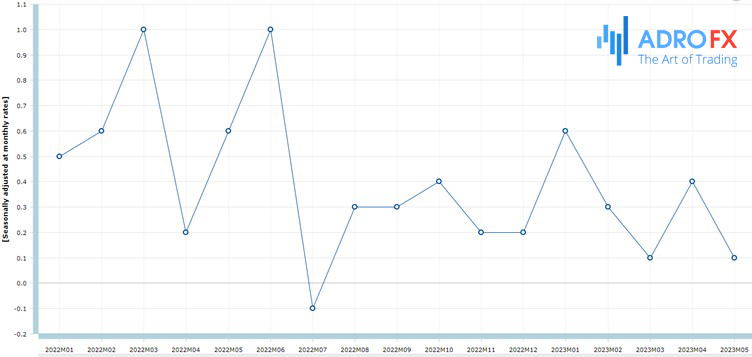

On Tuesday at 5:30 am GMT+1, the Reserve Bank of Australia (RBA) rate decision will take place, and it's a closely watched event to see if the central bank will raise its Official Cash Rate (OCR) by 25 basis points (bp) to 4.35% or maintain the status quo. In the previous two RBA meetings, the market was surprised by consecutive 25bp rate hikes. The recent monthly Consumer Price Index (CPI) data showed a rise of 5.6% in the twelve months to May, lower than April's 6.8% and market expectations of 6.1%. Strong employment data and uncertainties around China's economic recovery have led to a 63% probability of the RBA holding rates this week.

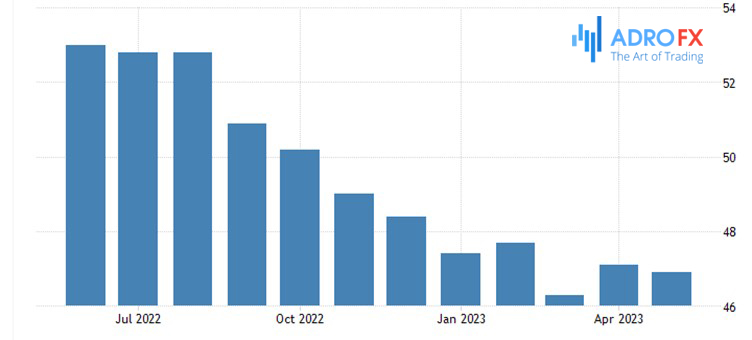

In the US, attention will be on the ISM Manufacturing and Services Purchasing Managers' Index (PMI) releases. The Services PMI has remained in contractionary territory for several months, and Monday's release at 3:00 pm GMT+1 is expected to continue that trend, with a forecast range between 48.3 and 46.7. The ISM Services PMI, scheduled for Thursday at 3 pm GMT+1, has remained in expansionary territory but experienced a decline from April's 51.9 to May's 50.3. The median expectation for June's release is 51.0. Notably, the past three months have seen a range between 52.0 and 50.0.

The most anticipated data in the US this week will be the labor market indicators. ADP non-farm employment change and JOLTS job openings data will be released a day before Friday's non-farm payroll report for June at 1:30 pm GMT+1. The median consensus is for 225,000 new payrolls added in June, down from May's strong figure of 339,000. The unemployment rate is expected to remain unchanged at 3.7%, with average hourly earnings projected to match the previous month's value at 0.3%. A strong jobs report for June would increase the likelihood of a rate hike this month.

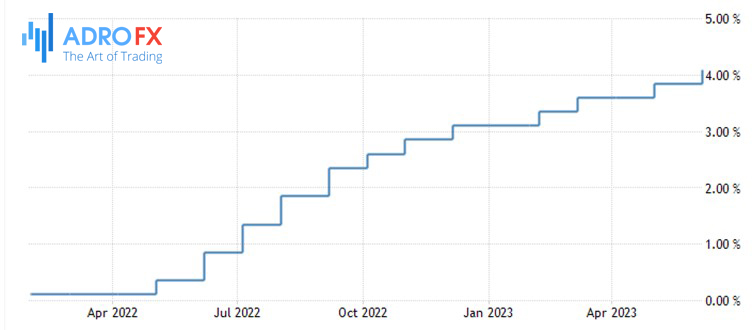

The Federal Open Market Committee (FOMC) left the Federal Funds target rate unchanged in June but signaled a hawkish stance. According to the FOMC's dot plot for May, two more rate increases are projected by the end of 2023. Currently, markets are pricing an 80% probability of a 25bp hike at the next meeting on July 26, followed by a potential pause and subsequent cuts in 2024.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates