Markets End the Week on a Positive Note Amid Tech Earnings and Global Currency Moves | Weekly Market Analysis

Key events this week:

Monday, November 3, 2025

- USA - S&P Global Manufacturing PMI (Oct)

- USA - ISM Manufacturing PMI (Oct)

- USA - ISM Manufacturing Prices (Oct)

Tuesday, November 4, 2025

- Australia - RBA Interest Rate Decision (Nov)

- USA - JOLTS Job Openings (Sep)

Wednesday, November 5, 2025

- USA - ADP Nonfarm Employment Change (Oct)

- USA - ISM Non-Manufacturing PMI (Oct)

- USA - ISM Non-Manufacturing Prices (Oct)

- USA - S&P Global Services PMI (Oct)

- USA - Crude Oil Inventories

Thursday, November 6, 2025

- UK - BoE Interest Rate Decision (Nov)

The US stock market wrapped up the week on a slightly upbeat note, with the S&P 500 closing higher on Friday. However, investors faced a volatile session as the major indexes swung between gains and losses, largely influenced by the quarterly results of technology giants Apple and Amazon. The Dow Jones Industrial Average added around 40 points, or 0.1%, while the S&P 500 rose 0.3%, and the NASDAQ Composite advanced 0.6%, helped by renewed optimism surrounding big tech.

Earlier last week, concerns about excessive spending in the technology sector initially weighed on sentiment. Yet, those worries eased somewhat as strong earnings reports from two of Wall Street’s most influential names reignited investor confidence. Apple and Amazon’s latest updates provided a temporary lift, offering reassurance that the tech sector remains resilient despite macroeconomic uncertainties.

Apple’s stock initially climbed but later gave back gains even after the company released a positive forecast for the upcoming holiday quarter. The iPhone maker expects revenue to rise between 10% and 12%, driven largely by its newest flagship model, the iPhone 17. CEO Tim Cook, speaking to CNBC, projected that this product cycle would help deliver the best December quarter in Apple’s history. Despite these upbeat expectations, the stock’s intraday performance reflected ongoing caution among traders, who continue to assess demand trends and broader market conditions.

Amazon, on the other hand, received a stronger investor reaction. Shares surged after the e-commerce giant reported quarterly earnings that comfortably exceeded Wall Street estimates. The company’s retail division benefited from improving margins, while its cloud business, Amazon Web Services (AWS), showed solid expansion. AWS revenue grew by 20%, marking its fastest pace since 2022. Though some analysts still see Amazon trailing competitors in the artificial intelligence race, the company’s performance suggests its AI-related investments are beginning to yield tangible results.

Meanwhile, geopolitical developments also played into market sentiment. The latest round of trade tensions between the United States and China appeared to ease slightly following informal discussions between President Donald Trump and Chinese President Xi Jinping. While no formal agreements have been signed, both sides reportedly agreed to pause new protectionist measures for one year. Although China has yet to deliver on its promises to increase agricultural imports or lift certain restrictions, the temporary truce helped calm nerves. It reduced the risk of further economic escalation.

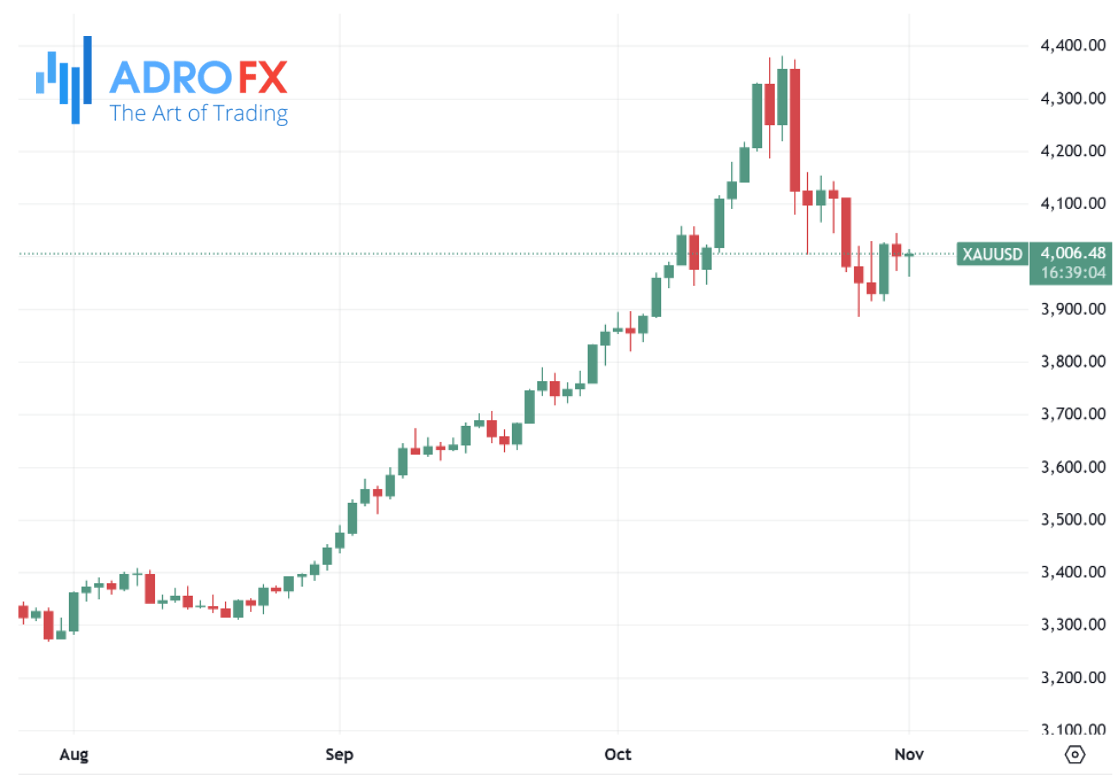

In the commodities space, gold prices (XAU/USD) rebounded after dipping to the $3,963 region earlier in the Asian session, reclaiming the $4,000 mark. The precious metal found support following remarks by President Trump suggesting potential restrictions on the export of advanced AI hardware to China. This renewed geopolitical uncertainty, combined with concerns about the possible fallout from a prolonged US government shutdown, helped attract safe-haven buying. However, gold’s upside was limited by a stronger US dollar, which continues to benefit from the Federal Reserve’s hawkish tone and expectations of higher interest rates for longer.

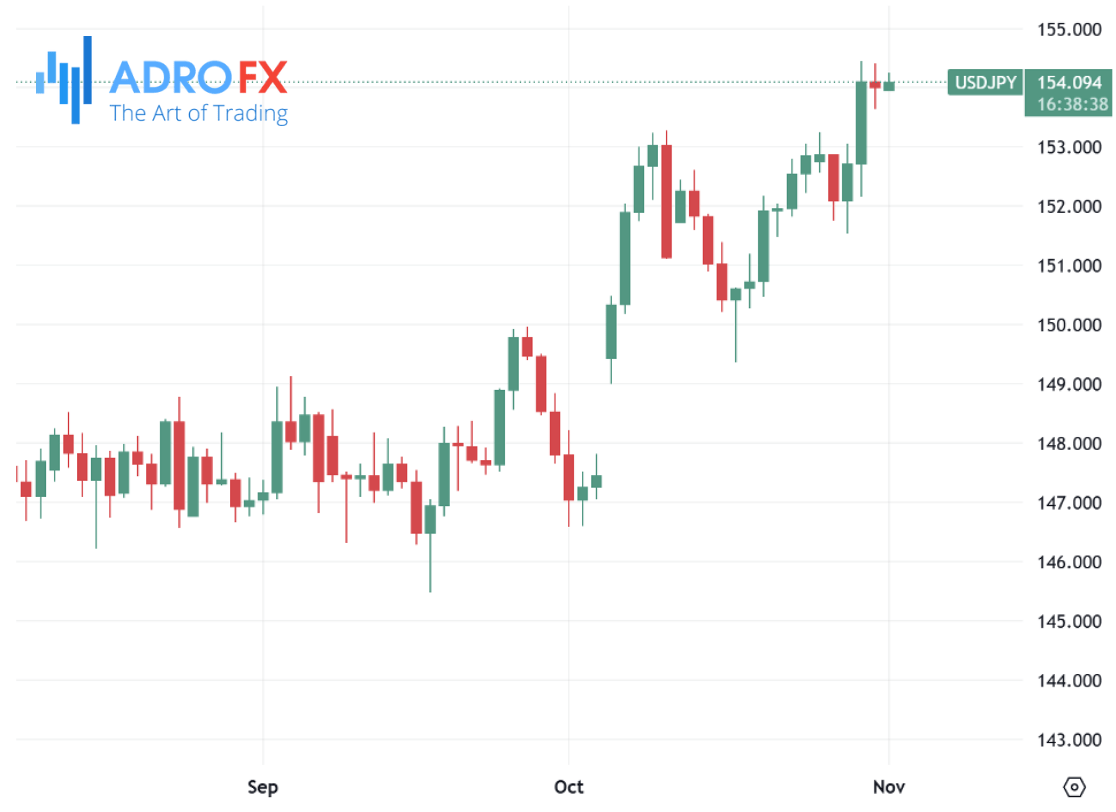

The Japanese yen remained weak, consolidating near its lowest level since mid-February as the dollar maintained strength. Market participants remain uncertain about when the Bank of Japan might raise rates again, especially amid speculation that newly appointed Prime Minister Sanae Takaichi will push for aggressive fiscal spending rather than monetary tightening. Even though Tokyo’s inflation figures came in stronger than expected, the yen’s traditional safe-haven appeal has been dampened by improving global risk appetite and rising US yields.

The Australian dollar halted a three-day decline, gaining modestly against the greenback. However, its upward momentum appeared fragile, with investors skeptical about a near-term policy shift by the Federal Reserve. Recent Australian data—including a 12% monthly increase in building permits and a small uptick in inflation—failed to generate much enthusiasm, particularly after China’s mixed economic releases. Job advertisements in Australia fell for the fourth straight month, highlighting a cooling labor market.

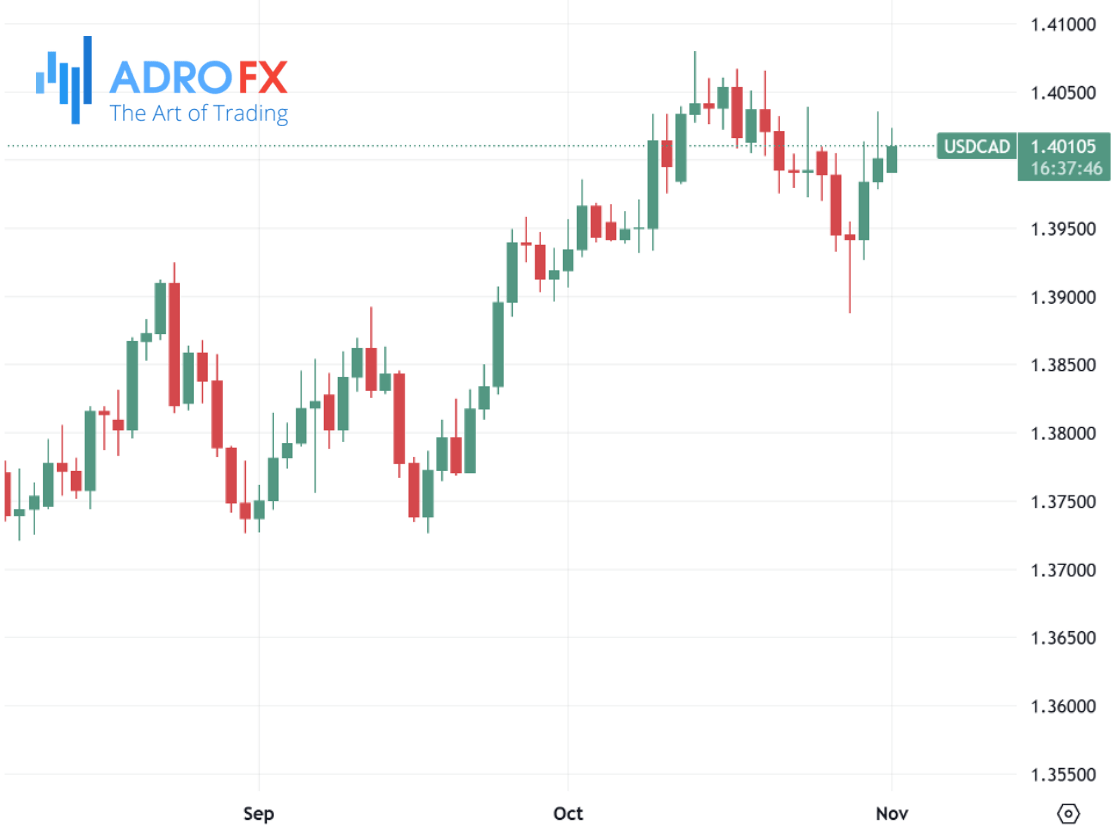

The Canadian dollar traded steadily after recent gains, with USD/CAD hovering around 1.4010. The loonie found support from higher oil prices, as West Texas Intermediate crude held firm near $61 per barrel. Crude’s strength followed news that OPEC and its allies plan to pause production increases in the first quarter of 2026 after a modest hike scheduled for next month. Given Canada’s role as the US's largest crude supplier, rising oil prices often bolster the CAD. Nonetheless, the pair could still see further dollar-driven strength if expectations for a December Fed rate cut continue to fade.

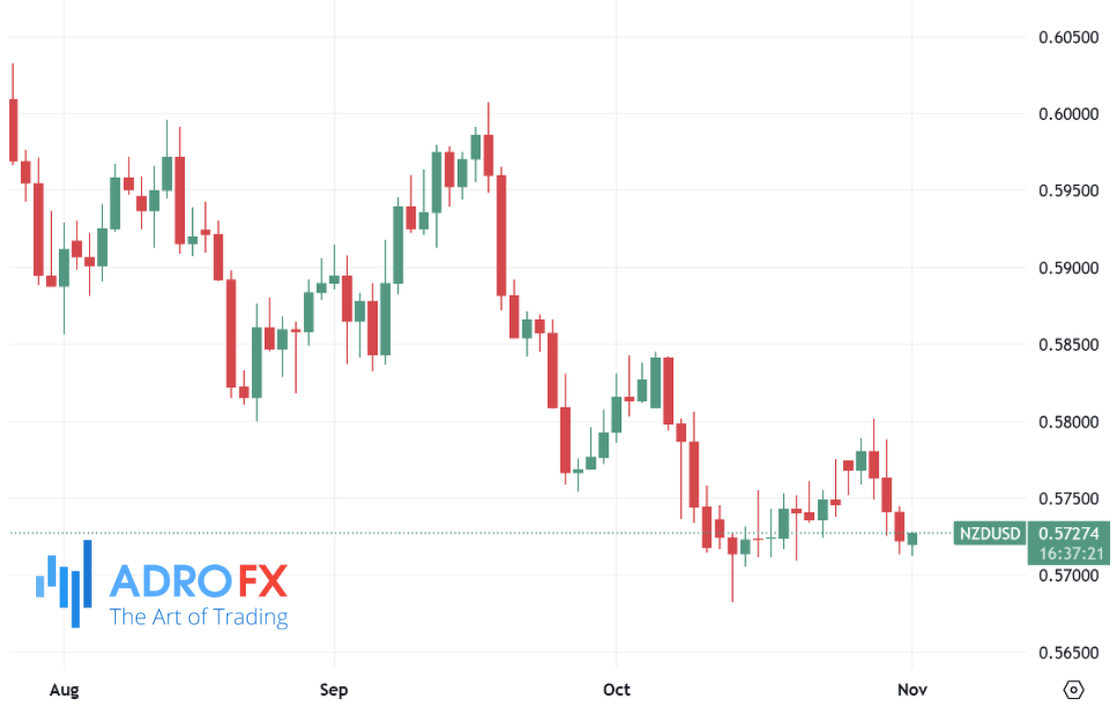

Elsewhere, the New Zealand dollar traded flat near 0.5715, limited by weaker-than-expected Chinese data. China’s October Manufacturing PMI fell to 50.6 from 51.2, missing market expectations and signaling a loss of momentum in the world’s second-largest economy. Since New Zealand’s economy is closely tied to China’s performance, the softer data weighed on the kiwi.

In Europe, the euro extended its losing streak to a fourth consecutive session, trading near 1.1530. Comments from European Central Bank officials highlighted a cautious approach toward policy adjustments. ECB policymaker Francois Villeroy de Galhau emphasized the need for flexibility amid market and geopolitical risks. At the same time, Latvia’s central bank governor, Martins Kazaks, said inflation and growth risks are becoming more balanced. The overall message suggested that while the ECB is comfortable with its current stance, it remains ready to act if necessary.

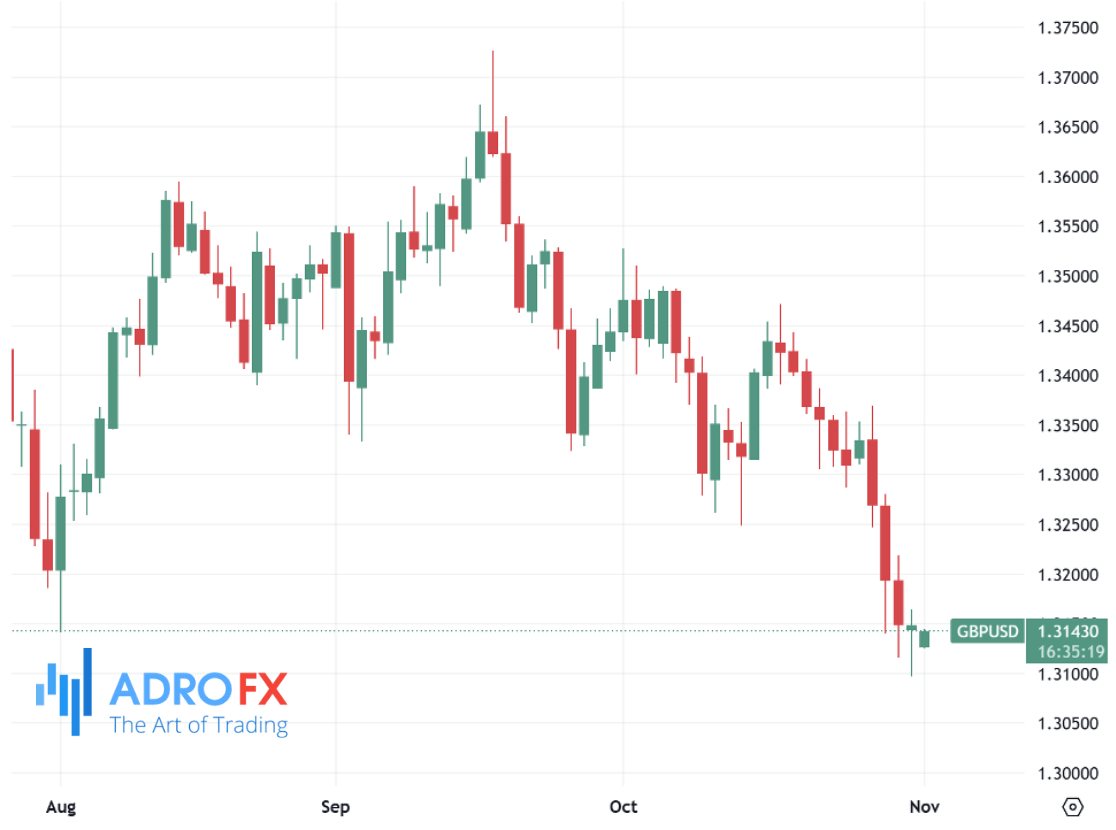

The British pound also struggled, trading near its lowest level since April amid growing fiscal and monetary uncertainty. Investors remain wary ahead of Finance Minister Rachel Reeves’ Autumn Budget scheduled for late November. Speculation is building that the Bank of England could soon begin cutting rates, with markets pricing in a one-in-three chance of a 25-basis-point reduction as early as November 6 and nearly 70% odds of a cut by year-end. Softer inflation readings, slowing wage growth, and rising unemployment have fueled expectations for policy easing. Still, traders are awaiting the BoE’s upcoming statement for clearer guidance.

Looking ahead, the focus now shifts to fresh US economic data, particularly the ISM Manufacturing PMI, which could offer further insight into industrial activity and inflationary pressures. Comments from Federal Open Market Committee members will also be closely monitored, as investors try to gauge the central bank’s next steps before year-end.

Overall, while the week ended with a mild recovery in equities and renewed confidence in select tech names, global markets remain in a delicate balance. Mixed economic signals, central bank policy shifts, and ongoing geopolitical uncertainties continue to shape investor sentiment. The coming days are likely to bring more data-driven volatility, keeping traders alert as 2025 approaches its final stretch.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates