S&P 500 Climbs as Investors Assess Earnings and Economic Outlook | Daily Market Analysis

Key events:

- USA - Core PCE Price Index (MoM) (Dec)

- USA - Core PCE Price Index (YoY) (Dec)

- USA - Chicago PMI (Jan)

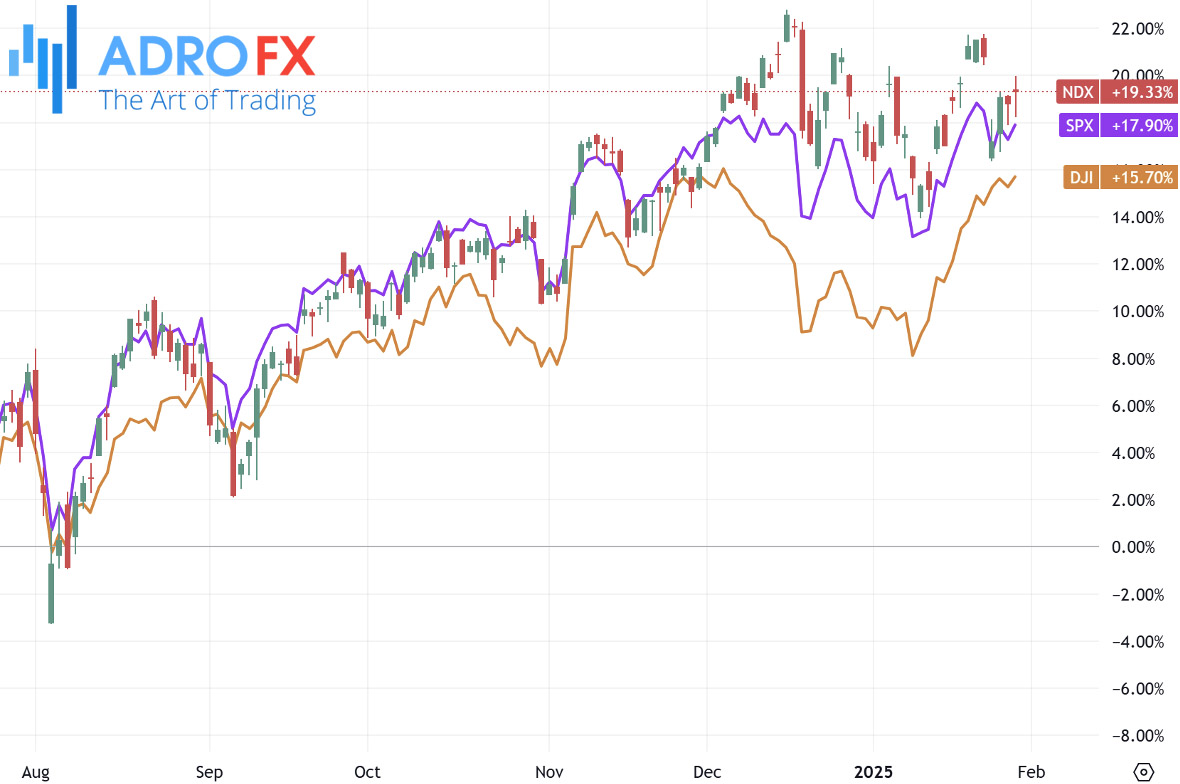

The S&P 500 ended Thursday on a positive note, although gains remained limited due to a pullback in Microsoft following its latest earnings report, which indicated slower cloud growth.

The broader market saw moderate advances, with the S&P 500 climbing 0.5%, the NASDAQ Composite increasing 0.3%, and the Dow Jones Industrial Average adding 168 points, or 0.4%. Investors evaluated earnings from major technology firms, including Microsoft and Meta Platforms, amid rising competition from a newly introduced budget-friendly Chinese AI model.

Microsoft (NASDAQ: MSFT) experienced a 6% drop in its stock price despite surpassing earnings expectations, as concerns over cloud revenue growth and AI-related spending weighed on sentiment. However, Wedbush Securities remained optimistic, highlighting that Microsoft’s AI segment exceeded estimates, generating an annualized revenue run rate of $13 billion - $1 billion higher than projected.

Attention now shifts to Apple’s (NASDAQ: AAPL) first-quarter earnings, scheduled for release late Thursday, which could set the tone for tech stocks moving forward.

The USD/CAD pair found support around the 1.4470 region during Friday’s Asian session, pausing its retreat from the previous day's peak, the highest level since March 2020. The currency pair remains near the psychologically significant 1.4500 level, on track for substantial weekly gains.

The Canadian Dollar continues to face headwinds due to the Bank of Canada’s dovish stance and concerns over US trade policy. The BoC recently implemented its sixth consecutive rate cut and announced the conclusion of its quantitative tightening measures. Adding further pressure, Trump reiterated threats of imposing 25% tariffs on Mexico and Canada, both of which are key trading partners of the United States. This geopolitical uncertainty is helping to bolster the USD/CAD pair.

The US Dollar has also retained its weekly gains, supported by the Federal Reserve’s hawkish pause on interest rates and a modest recovery in US Treasury bond yields. However, lingering concerns over US economic policy and global trade tensions have limited the greenback’s upside. Meanwhile, a rebound in oil prices has lent some support to the commodity-linked Canadian Dollar, capping further gains in USD/CAD.

The EUR/USD pair encountered selling pressure around 1.0385 during Friday’s Asian session, as expectations of further interest rate cuts by the European Central Bank continued to weigh on the Euro. Investors are also closely monitoring developments related to potential new tariffs from the US.

As widely anticipated, the ECB lowered its deposit facility rate during its January policy meeting, reducing it to 2.75%. The central bank signaled the possibility of additional rate cuts due to economic uncertainty and persistent inflation concerns, which could further drag down the Euro.

The Australian Dollar attempted to halt its four-day decline against the US Dollar on Friday but struggled amid renewed risk-off sentiment following Trump’s tariff threats against China.

Although Trump focused on imposing a 25% tariff on Canada and Mexico, he also hinted that similar measures against China were being considered. Given China’s critical trade relationship with Australia, any escalation in US-China trade tensions could place further downward pressure on the Australian Dollar.

Additionally, major Australian banks - including ANZ, CBA, Westpac, and NAB - have revised their forecasts, now expecting the Reserve Bank of Australia to implement a 25-basis-point rate cut in February, rather than in May as previously predicted. This shift in expectations stems from easing inflationary pressures toward the end of 2024, which have fueled speculation that the RBA may adjust its monetary policy sooner than anticipated. The central bank has maintained its Official Cash Rate (OCR) at 4.35% since November 2023, stressing that inflation must consistently fall within the 2%-3% target range before it considers any rate reductions.

The Japanese Yen reversed its two-day winning streak against the US Dollar, attracting some selling pressure during the Asian session. However, substantial depreciation appears unlikely due to expectations that the Bank of Japan will proceed with further rate hikes.

This sentiment was reinforced by economic data released on Friday, which showed that Tokyo’s consumer prices rose in January. Additionally, Japan’s Industrial Production registered unexpected growth in December, while Retail Sales exceeded expectations. These developments, along with ongoing geopolitical risks, could provide support for the safe-haven Yen, potentially capping the upside for the USD/JPY pair.

Traders are now turning their attention to the upcoming US Personal Consumption Expenditure (PCE) Price Index report, which may provide further direction for the currency markets.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates