QT as the Fed's Last Resort | Daily Market Analysis

Key events:

- US – Martin Luther King, Jr. Day

- UK – BoE Gov Bailey Speaks

The recently released CPI is prompting investors to question the Fed's plans to raise the overnight rate above 5%. The market doesn't seem to care, and after this data coincides with the forecast, yields are falling across the curve. Thus, 2-year Treasury yields have fallen to their lowest level since October, with room to fall substantially.

If the Fed really does intend to raise rates that much and maintain tight financial conditions, then it appears that the market is not listening to the central bank and not paying attention to what it wants.

This only suggests that the Fed's forward guidance is no longer working. The Fed will have to dig into its toolbox to convince the market that it is serious. The central bank may have to talk about accelerating the pace of balance sheet reduction or outright sales of treasuries and mortgage-backed securities.

The market indicates that the Fed's interest rate hike cycle is coming to an end, with the belief that the central bank will be forced to cut rates as soon as 2023. However, the Fed continues to insist that it plans to raise rates above 5% and leave them high and financial conditions tight for a long time.

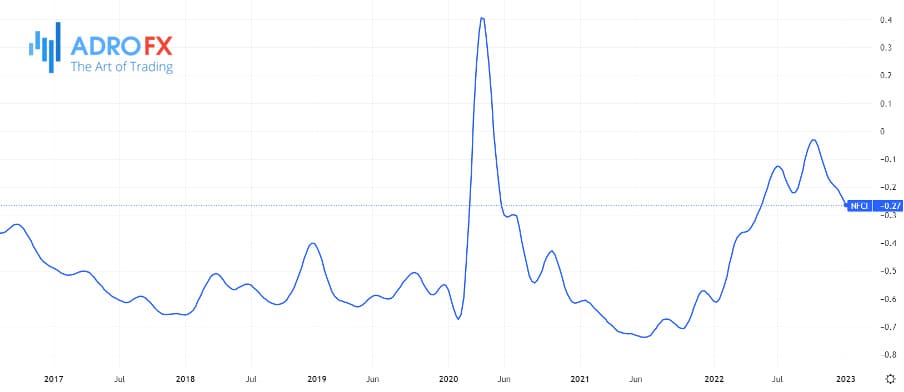

Despite the Fed's best efforts and hawkish comments, the market doesn't care. Financial conditions continue to soften, with the FRB Chicago Financial Conditions Index falling to its lowest level since May 2022.

Contrary to the Fed's intentions, 2-year Treasury yields fell to their lowest level since early October. This is the first weakening in months. Apparently, the rate cut is now embedded in the quotes of not only the federal funds rate futures market.

As a consequence, the Fed will be forced to use balance sheet talk as a last resort to ensure that rates remain elevated and the dollar remains strong enough to prevent a stronger-than-acceptable Fed easing of financial conditions.

The market, on the other hand, is trying to figure out how much pressure it can put on the Fed to maintain tight financial conditions. If the central bank is serious, sooner or later it will try to fight back. Otherwise, the Fed will lose control of the public discourse and won't be able to tell the markets what direction it thinks they should go.

Talk of a higher overnight rate is no longer having the desired effect, so the next option for the Fed is balance.

If it doesn't use that option, the markets will take it as a signal that the Fed is okay with easing financial conditions and thus gives the markets permission to continue the rally.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates