Global Stock Markets Rally on Passage of US Debt Ceiling Bill, US Treasury Yields Decline Amid Cooling Labor Market | Daily Market Analysis

Key events:

- USA - Average Hourly Earnings (MoM) (May)

- USA - Nonfarm Payrolls (May)

- USA - Unemployment Rate (May)

On Thursday, global stock markets experienced a rise following the passage of a bill by the US House of Representatives to increase the federal debt ceiling. Concurrently, US Treasury yields declined as data indicated a cooling labor market, diminishing the likelihood of an interest rate hike by the Federal Reserve.

The bill, which suspends the $31.4 trillion debt ceiling, successfully passed through the House of Representatives on Wednesday. This achievement averted the potential of a catastrophic government default. Despite opposition from staunch members of both the Democratic and Republican parties, the measure received support from a majority of representatives in both parties. The bill will now be considered by the US Senate as the next step in the process.

Both the Nasdaq and S&P 500 indices soared to their highest closing levels in nine months. This surge was fueled by indications of decreasing wage pressures, which raised hopes that the Federal Reserve would halt its interest rate hikes. The Nasdaq and S&P 500 reaching their highest levels since August 2022 demonstrates investor enthusiasm for a resilient labor market, along with optimism regarding the Federal Reserve's ability to navigate an economic soft landing.

Additionally, investors reacted positively to a congressional vote.

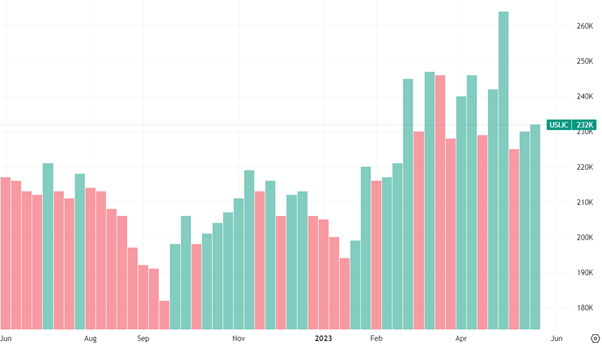

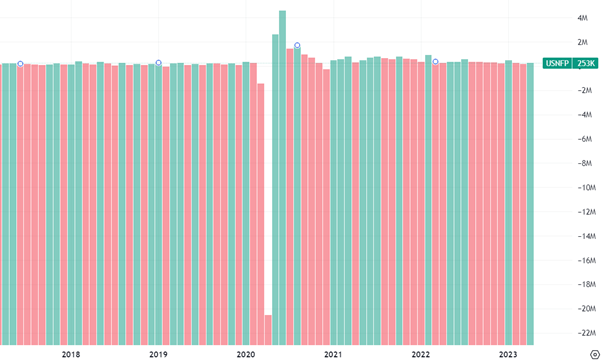

While the number of Americans filing new claims for unemployment benefits saw a modest increase last week, private payrolls experienced higher-than-anticipated growth in May. These factors indicate that the labor market remains tight, potentially leading the Federal Reserve to maintain elevated interest rates.

Investor attention now turns to the release of the Labor Department's highly anticipated unemployment report for May as this data will play a crucial role in determining whether the Federal Reserve will continue with its aggressive rate hikes.

Ahead of today's US Payrolls report, the US Dollar experienced a decline as traders unwound speculative long positions. This move was prompted by comments from Federal Reserve officials, including Philadelphia President and FOMC member Harker, who suggested that the central bank should forego a rate hike in June. These remarks boosted risk appetite in the market, leading to an increase in stock prices.

The Dollar Index (DXY) registered a decrease of 0.64% and closed at 103.56 (compared to 104.20 the previous day).

Meantime, Eurozone inflation has undergone a significant decline since its peak of 10.6% year-on-year in October of the previous year. This descent has been occurring at a similar pace to its earlier surge. Recent data from various member states, released earlier this week, indicates a noteworthy drop in Eurozone inflation during May. The rate fell to 6.1% year-on-year, down from 7.0% in April, which is below the expected consensus of 6.3% reported by Reuters. The decrease in inflation can be attributed to the base effects resulting from last year's price increase, as well as a reduction in price pressures across various categories as the impact of imported cost shocks diminishes. This trend is expected to persist throughout 2023.

The nonfarm payrolls figures for May, released today, may follow the pattern of the past few months, wherein the headline numbers consistently surpassed forecasts. The median expectations for the Payrolls report anticipate a rise of 190,000 to 193,000 jobs. If the number surpasses 200,000, there could be a significant rebound in the value of the US Dollar compared to other currencies, followed by a period of stabilization. On the other hand, if the Payrolls figure falls below 185,000 or lower, it would be perceived as weak, leading to a reduction in bets favoring the US Dollar in the markets.

It is also important to pay attention to the data on Wages (Average Hourly Earnings). Forecasts suggest a decrease of 0.3% from the previous 0.5%. If the Wages number falls below 0.3%, it would exert pressure on the US Dollar.

Additionally, the statements made by Federal Reserve officials will be crucial. If their rhetoric continues to indicate a desire to forgo a rate increase in June, it would further weigh on the US currency.

Monitoring the Payrolls report, Wages data, and Fed communications will provide valuable insights into the potential impact on the US Dollar and currency markets.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates