Global Markets React as Dow Hits Milestone, Yen Weakens, and Shutdown Clouds US Outlook | Weekly Market Analysis

Key events this week:

Wednesday, October 8, 2025

- New Zealand - RBNZ Interest Rate Decision

- USA - Crude Oil Inventories

- USA - 10-Year Note Auction

- USA - FOMC Meeting Minutes

Thursday, October 9, 2025

- USA - Fed Chair Powell Speaks

- USA - Initial Jobless Claims

- USA - 30-Year Bond Auction

Friday, October 10, 2025

- USA - Average Hourly Earnings (MoM) (Sep)

- USA - Nonfarm Payrolls (Sep)

- USA - Unemployment Rate (Sep)

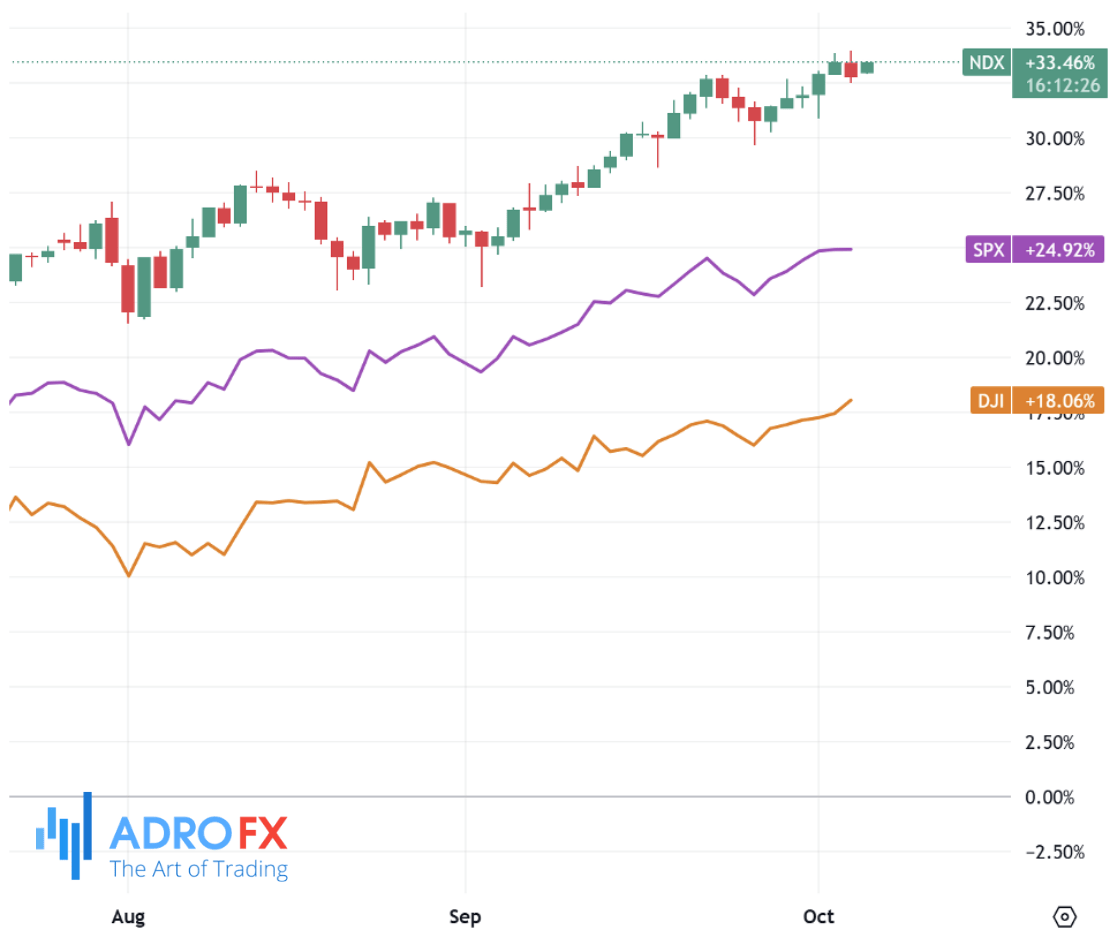

The Dow Jones Industrial Average delivered an impressive performance on Friday, climbing more than 480 points at its peak, marking a gain of over 1% before paring back some of the advance. For the first time, the index briefly surpassed the psychological 47,000 level, only to retreat and close with a more moderate rise of approximately 250 points, or 0.55%. This move underscored investors’ confidence even in the face of political and economic uncertainty, although the broader S&P 500 finished flat and the Nasdaq Composite edged lower by 0.3% after late-session weakness in high-profile technology names such as Palantir, Tesla, and Nvidia. Despite the pullback, all three benchmarks touched new intraday records, reflecting ongoing resilience in equity markets.

Much of the optimism in stocks comes from investors largely brushing aside the impact of the ongoing US government shutdown. While the closure has created disruptions, particularly by halting the release of crucial federal data, sentiment remains supported by expectations that the shutdown will not extend for long. The absence of Nonfarm Payrolls data has left the Federal Reserve with fewer indicators to guide its upcoming policy moves. However, traders still anticipate that the central bank is likely to cut interest rates again later this month. With the labor market showing cracks, particularly after the steep decline in ADP private-sector employment figures earlier in the week, rate markets are almost fully pricing in a quarter-point cut on October 29, building on the move the Fed made in September.

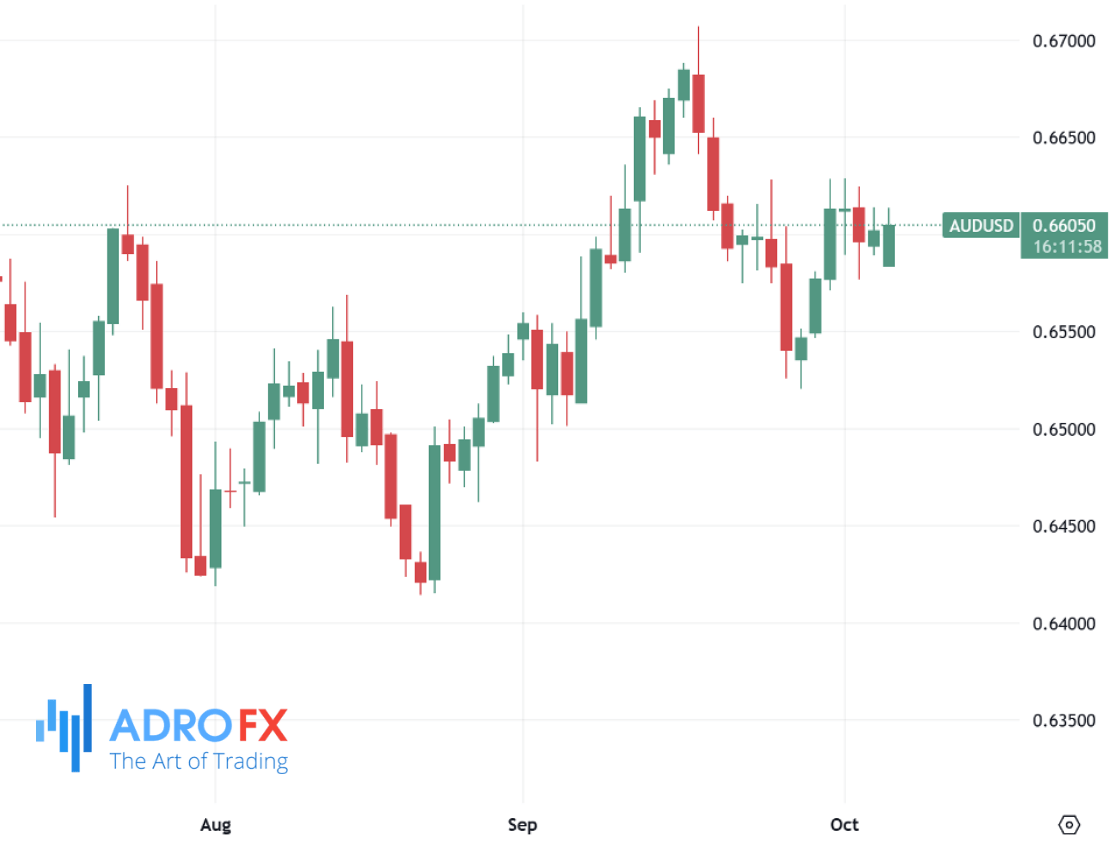

Meanwhile, in the currency market, the Australian Dollar began the week on firmer footing against the US Dollar after the TD-MI Inflation Gauge showed stronger-than-expected price pressures. The September reading rose 0.4% from the prior month, reversing a decline of 0.3% in August. On an annual basis, the indicator increased to 3% from 2.8%, signaling that inflation is persisting despite the Reserve Bank of Australia’s attempts to contain it within its 2–3% target band. Investors are now paying close attention to remarks from RBA officials, as the central bank maintained its cash rate at 3.6% during its September meeting and warned that service-sector inflation remains stubbornly high, while labor market conditions remain tight. These signals make a near-term rate cut less likely, offering support to the Aussie as markets await more clarity.

The Japanese Yen, by contrast, weakened sharply as a new political chapter unfolded in Tokyo. The ruling Liberal Democratic Party’s leadership election positioned Sanae Takaichi to become Japan’s first female prime minister. Widely perceived as fiscally dovish, she is expected to resist further monetary tightening from the Bank of Japan. This development, coupled with improved risk appetite globally, fueled aggressive selling in the safe-haven Yen, driving USD/JPY back toward the 150.00 level last seen in August. Still, the downside for the Yen may not be unlimited. Bank of Japan Governor Kazuo Ueda recently reiterated that rate hikes remain on the table if inflation and growth align with forecasts, and markets are already anticipating an increase in borrowing costs early next year. That stance highlights the growing divergence between a potentially more hawkish BoJ and a Federal Reserve seen as ready to ease further.

Elsewhere, the New Zealand Dollar found modest support in early Monday trading, with NZD/USD hovering around 0.5825. However, traders remain cautious ahead of Wednesday’s Reserve Bank of New Zealand meeting, where a rate cut is widely expected. Markets have priced in a 25-basis-point reduction, with some betting on a deeper 50-point cut. With recent GDP data weaker than projected, economists interpret the RBNZ’s path as a dovish pivot, signaling more easing ahead. While this may pressure the Kiwi over time, short-term dynamics will likely depend on US Dollar flows and global risk sentiment.

The Euro, meanwhile, saw a modest retreat, slipping back to trade near 1.1720 after advancing late last week. The inability of the US Senate to resolve the government shutdown for the fourth time has added to concerns about US fiscal stability, but the suspension of federal data releases has created an additional layer of uncertainty for currency traders. Without key updates, the dollar’s strength has fluctuated, allowing the Euro to benefit in recent sessions. The European Central Bank remains in the spotlight, with policymakers signaling that current interest rates are appropriate for the time being. Martins Kazaks recently emphasized that uncertainty is still very high, meaning the ECB needs flexibility in future decisions. Traders are preparing for comments from ECB Vice President Luis de Guindos and Executive Board member Philip Lane, which could guide expectations heading into upcoming data releases such as Eurozone Sentix Investor Confidence and retail sales figures.

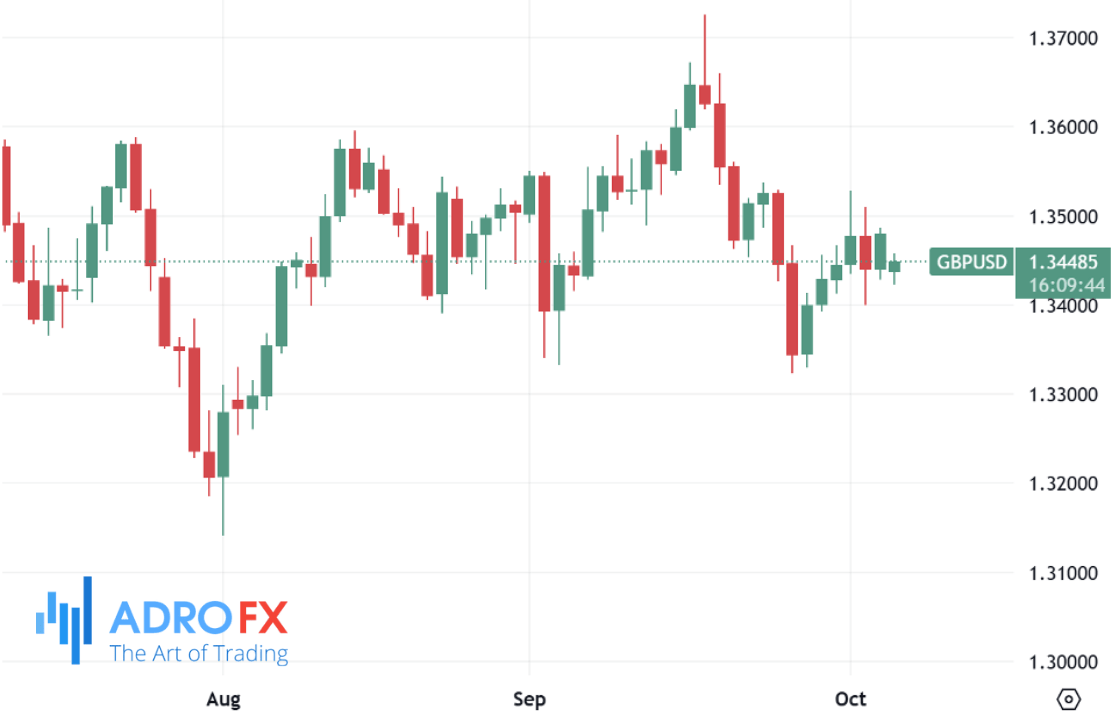

In the UK, the British Pound lost momentum after a strong rally on Friday. GBP/USD opened the week with a bearish gap, slipping below the mid-1.3400s amid a stronger US Dollar. Although the pair has avoided deeper declines, it remains under pressure. Money markets anticipate the Bank of England will hold interest rates steady at 4% through the rest of the year, with inflation proving sticky and the economy showing resilience. This stance could ultimately provide support for Sterling, but traders are cautious, awaiting new catalysts. Attention will soon turn to the UK Construction PMI release and a speech from Bank of England Governor Andrew Bailey, both of which could influence market sentiment and Sterling’s near-term trajectory.

Broader market dynamics also continue to highlight the divergence in central bank strategies. While the Federal Reserve is leaning toward more cuts, both the ECB and BoE appear set to hold steady for now, while the BoJ edges closer to potential tightening under new political leadership. These differences are creating sharp moves across currency pairs as traders position for the months ahead.

Looking ahead, the lack of US data due to the government shutdown will make central bank communication even more critical. Investors are closely watching scheduled remarks from Fed officials, including Governor Christopher Waller and regional presidents Beth Hammack, Alberto Musalem, John Williams, and Raphael Bostic. Their comments could provide clarity on how the Fed views the balance between cooling growth, labor market weakness, and still-elevated inflation. For now, markets appear to be holding onto a cautiously optimistic stance, with equity gains offsetting political uncertainty and global currencies reacting to a shifting landscape of monetary policy.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates