Global Markets React to Shifting Monetary Policy and Geopolitical Tensions | Weekly Market Analysis

Key events this week:

Tuesday, September 2, 2025

- Eurozone - CPI (YoY) (Aug)

- USA - S&P Global Manufacturing PMI (Aug)

- USA - ISM Manufacturing PMI (Aug)

- USA - ISM Manufacturing Prices (Aug)

Wednesday, September 3, 2025

- USA - JOLTS Job Openings (Jul)

Thursday, September 4, 2025

- USA - ADP Nonfarm Employment Change (Aug)

- USA - Initial Jobless Claims

- USA - S&P Global Services PMI (Aug)

- USA - ISM Non-Manufacturing PMI (Aug)

- USA - ISM Non-Manufacturing Prices (Aug)

- USA - Crude Oil Inventories

Friday, September 5, 2025

- USA - Average Hourly Earnings (MoM) (Aug)

- USA - Nonfarm Payrolls (Aug)

- USA - Unemployment Rate (Aug)

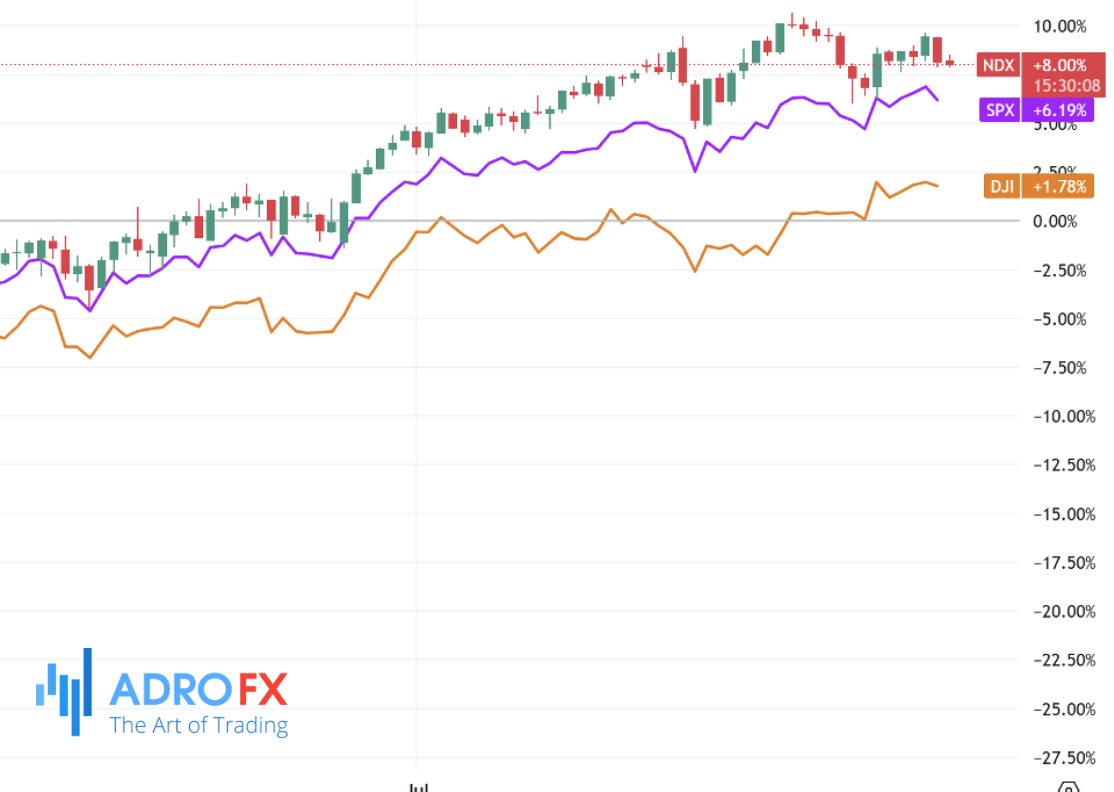

The Dow Jones Industrial Average began the week on a softer note, pulling back modestly yet still holding near record territory. Despite losing 91 points, or 0.2%, the index remains within sight of its historic highs above 45,760.

The broader market also faced selling pressure, with the S&P 500 declining 0.6% and the Nasdaq Composite sliding 1.2%, as investors reassessed the balance between monetary policy expectations and persistent geopolitical risks. Even though the recent bullish momentum has cooled, the Dow has continued to find support near the 45,500 zone, suggesting that the long-term uptrend is far from broken.

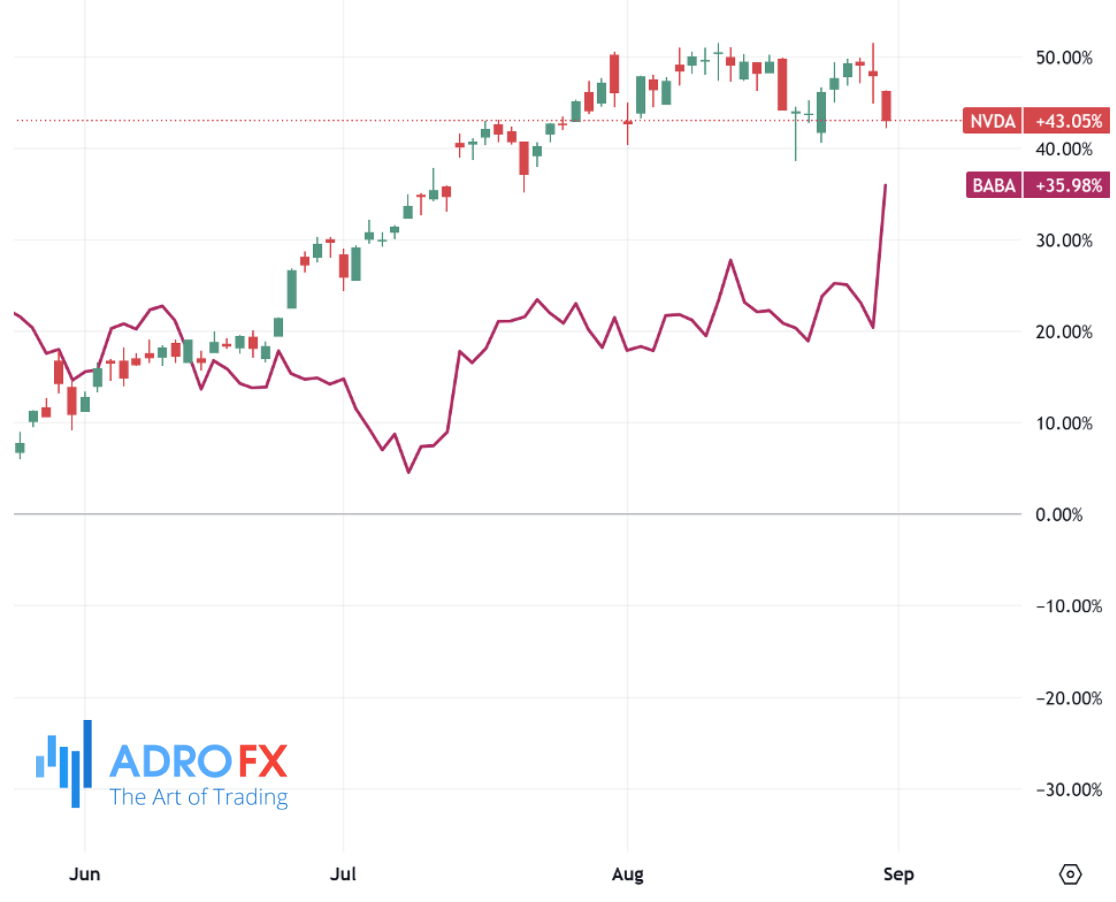

Technology stocks were among the laggards, with NVIDIA Corporation shedding over 3% as uncertainty around its sales to China weighed heavily. US restrictions on chip exports remain a key concern for the company, especially as Beijing accelerates efforts to lessen dependence on American suppliers. Alibaba contributed to the story by introducing a homegrown chip tailored for AI inferencing, a development seen as a clear indication of China’s drive to strengthen its semiconductor independence. Although inferencing chips are less complex than those used in AI training - the area where China remains vulnerable - the development illustrates the strategic priority given to technological self-sufficiency.

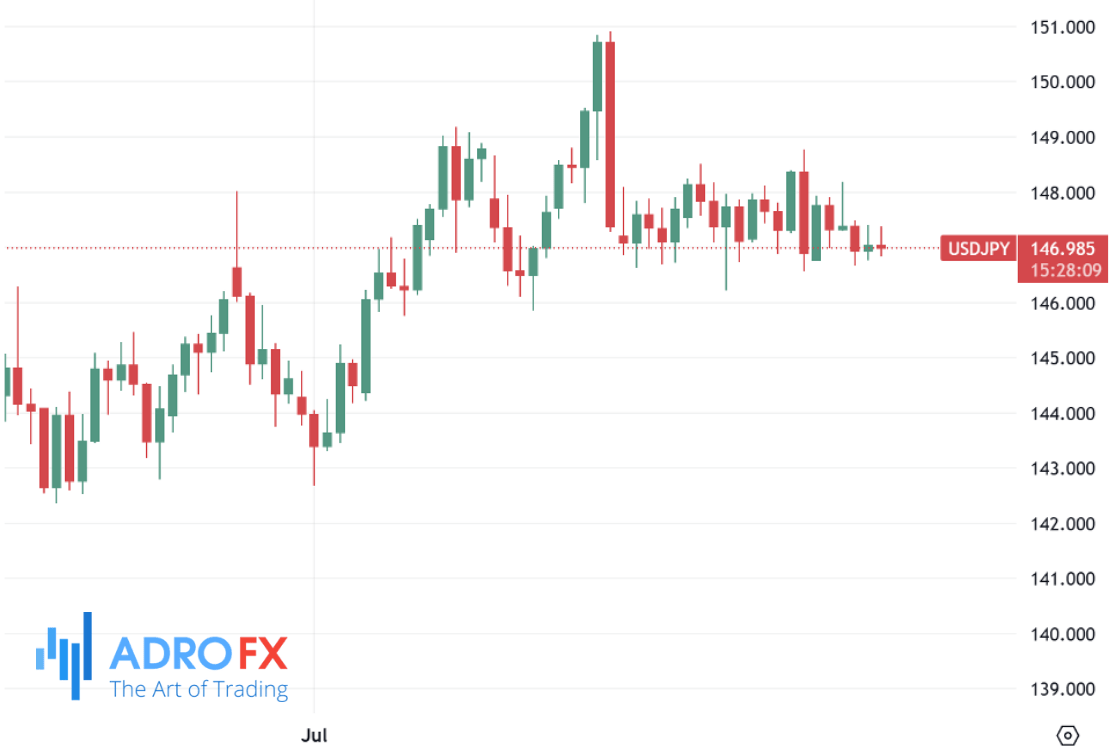

On the currency front, the Japanese yen started the week with limited momentum, trading just below the mid-147 level. While safe-haven demand could offer some support due to the intensifying conflict in Ukraine and ongoing instability in the Middle East, the yen has struggled to make meaningful gains. Expectations of a Bank of Japan rate hike continue to circulate, reflecting optimism that wage growth is spreading across sectors. This contrasts sharply with growing bets that the Federal Reserve will deliver two rate cuts before the end of 2025. The divergence between central bank paths is keeping a lid on USD/JPY upside as traders weigh hawkish signals from Tokyo against the prospect of easier US monetary policy.

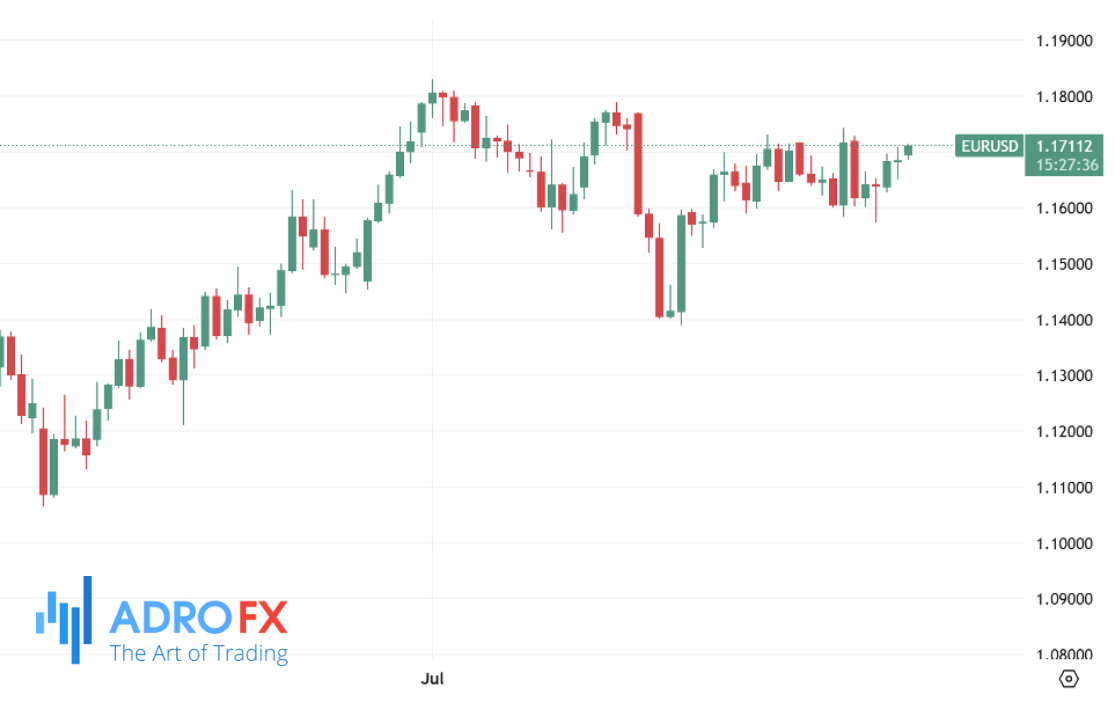

The euro has remained steady near 1.1705 against the US dollar, supported by growing market bets that the Federal Reserve may soon reduce interest rates. Data from the latest US inflation release showed the Personal Consumption Expenditures (PCE) Index climbing 2.6% year-over-year in July, while the core reading came in at 2.9%, both matching expectations. Although inflation remains somewhat elevated, traders largely anticipate a September rate cut, an outlook strengthened by dovish signals from Fed Chair Jerome Powell during the Jackson Hole symposium and further echoed by Governor Christopher Waller, who noted that more aggressive easing could be warranted if labor market conditions continue to deteriorate.

Market pricing via the CME FedWatch tool now assigns nearly an 89% likelihood to a 25 basis-point cut next month, slightly higher than before the PCE release. Even so, the euro’s trajectory remains clouded by political and security risks. European Commission President Ursula von der Leyen revealed that member states are preparing detailed plans for potential military support in Ukraine, backed by US commitments. The continuation of the Russia-Ukraine conflict raises energy security concerns, which could weigh on the common currency in the months ahead.

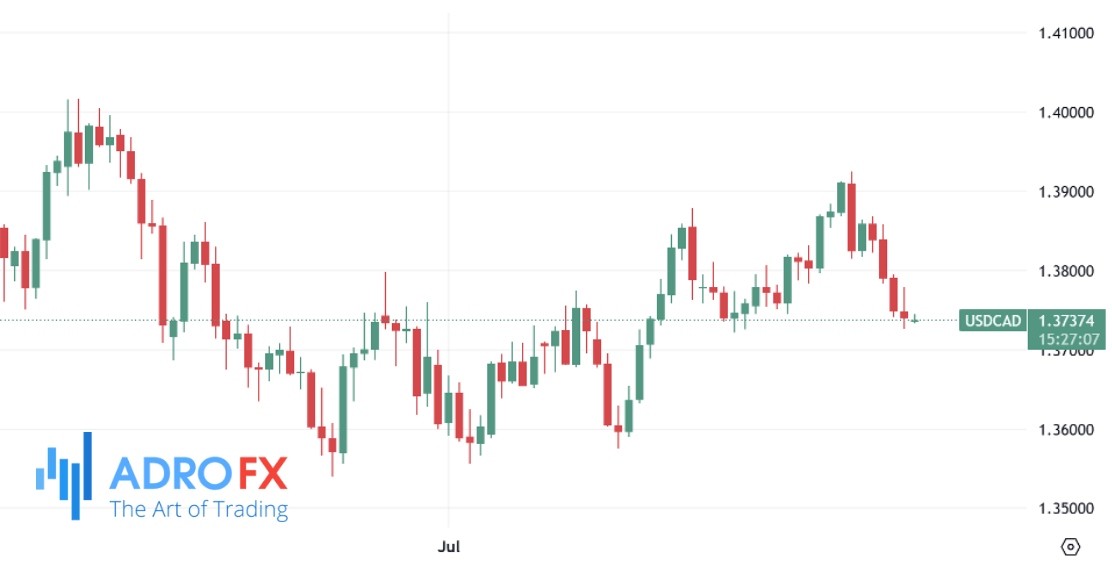

In North America, the Canadian dollar extended its winning streak, with USD/CAD dropping for a fifth straight session to around 1.3740. The move has been largely fueled by broad dollar softness tied to Fed easing bets. However, the loonie’s gains remain capped by the decline in crude oil prices. West Texas Intermediate futures slipped to roughly $63.50, pressured by worries over oversupply and sluggish demand. Given Canada’s position as the largest oil exporter to the US, energy market dynamics remain a decisive factor for the currency’s direction.

The Australian dollar paused after a four-day rally, easing slightly as traders digested weaker domestic housing data. July building permits fell 8.2% month-over-month, more than forecast, reversing the sharp gains from the previous month. Nevertheless, the broader trend for AUD/USD appears constructive, supported by China’s economic readings. The Caixin manufacturing PMI moved back into expansion territory at 50.5, compared with 49.5 in July, highlighting signs of stabilization in the Chinese industry. Since China is Australia’s largest trading partner, any improvement in Beijing’s economy often provides indirect support for the Aussie. Domestic inflation data has also been firmer than expected, with consumer prices rising 2.8% year-on-year, lowering the likelihood of near-term rate cuts by the Reserve Bank of Australia.

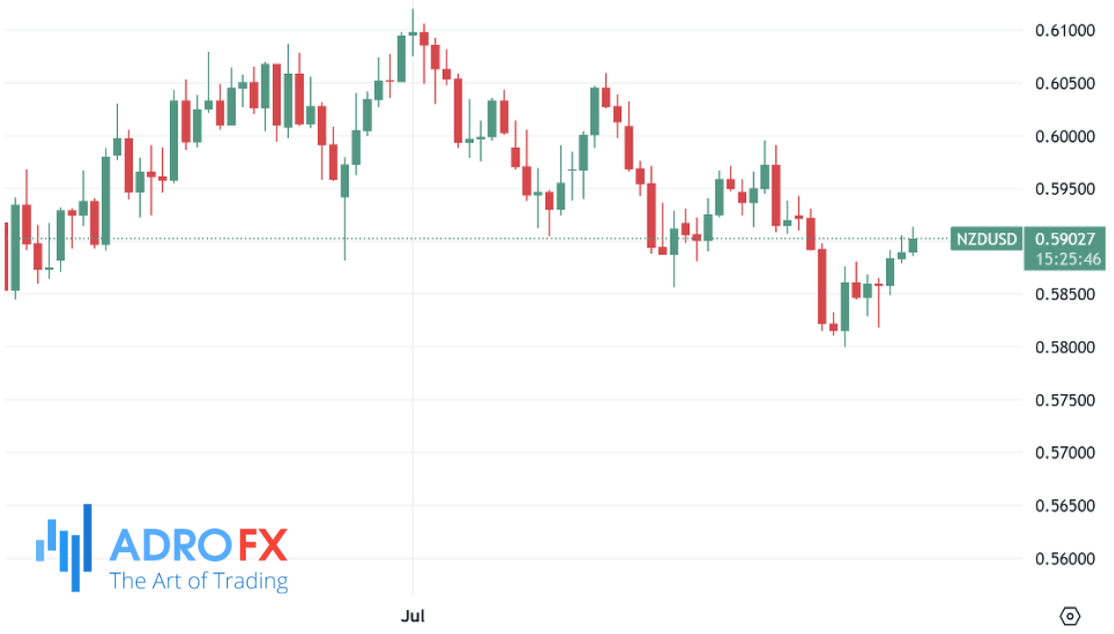

New Zealand’s currency also found some buyers, with NZD/USD climbing toward 0.5905. The uptick came after the Chinese PMI data, but optimism remains tempered by trade frictions. Recent warnings from Washington about imposing heavier tariffs on strategic Chinese exports, including rare-earth materials, rekindled fears of a renewed trade war. A US court ruling last week that questioned the legality of several unilateral tariffs has only complicated the outlook further. For New Zealand, which is highly exposed to global trade dynamics, escalating US-China tensions could quickly reverse the kiwi’s gains.

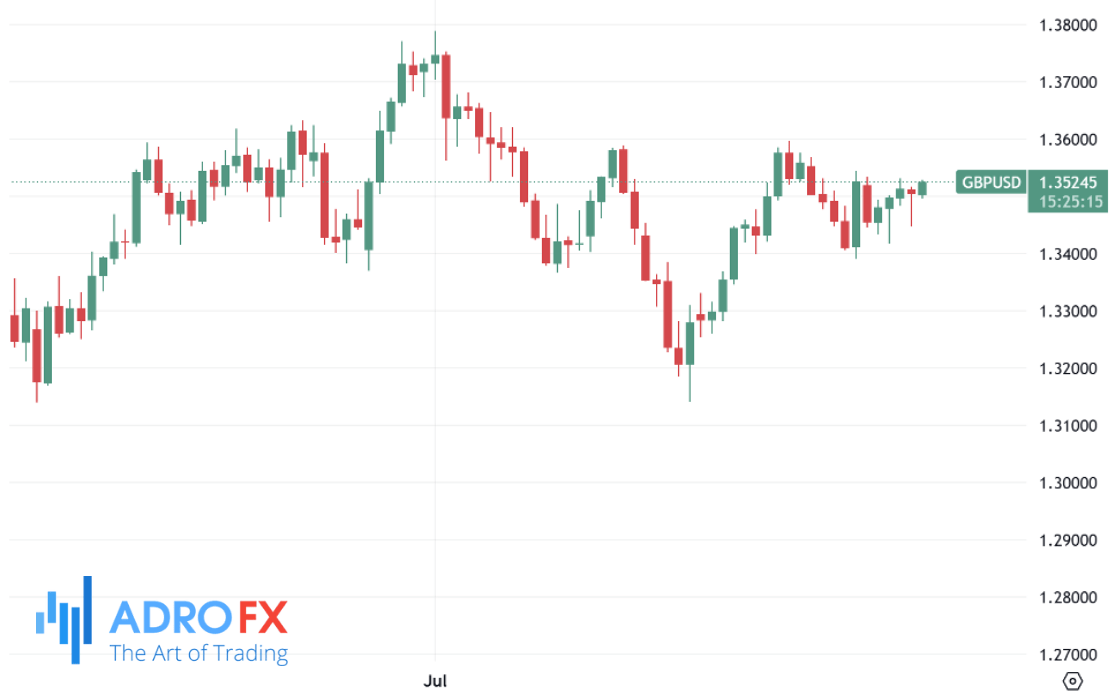

The British pound started the week on a stronger note, consolidating above the 1.3500 level. Sterling continues to benefit from the Bank of England’s cautious stance on policy easing. While the BoE implemented a modest rate cut earlier, it has signaled a slower, more deliberate approach compared with expectations for more aggressive action from the Fed. This divergence has underpinned GBP’s relative resilience. Still, the currency faces short-term headwinds, particularly from fluctuations in US dollar sentiment and incoming data releases. Traders are now focused on the final reading of the UK Manufacturing PMI as well as the all-important US nonfarm payrolls report due at the end of the week. These updates will play a pivotal role in shaping expectations around both the dollar and broader risk sentiment.

In commodities, oil’s weakness has been a recurring theme, adding another layer of uncertainty to global markets. Demand outlook remains fragile, with signs of slowing industrial activity in major economies and persistent oversupply concerns. On the other hand, precious metals continue to draw attention as investors balance inflationary risks with the likelihood of lower interest rates. While gold prices have edged down in recent sessions, the potential for Fed easing and ongoing geopolitical volatility could provide underlying support for the yellow metal in the weeks ahead.

The overarching narrative is that volatility remains elevated as traders seek clarity on the Federal Reserve’s next steps and the persistence of geopolitical shocks. While short-term swings are inevitable, markets continue to price in a supportive environment for risk assets if central banks follow through with easing cycles. Yet, external risks - from conflicts in Eastern Europe and the Middle East to trade disputes and energy instability - remain capable of reversing sentiment rapidly.

As September approaches, all eyes will be on the Federal Reserve, labor market data, and global diplomatic developments to determine the next decisive move in markets.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates