Global Equities Surge to New Highs Amid Earnings Optimism and Rate Cut Speculation | Daily Market Analysis

Key events:

- Canada - Building Permits (MoM) (Mar)

- USA - FOMC Member Mester Speaks

Global equities surged on Friday, driving European stocks to new record highs amid robust corporate earnings and expectations of imminent central bank interest rate cuts. Despite signs of decelerating US economic growth, the dollar managed to edge higher.

European equities witnessed their most substantial weekly increase since late January, with the STOXX 600 index extending its rally for a sixth consecutive session, while London's FTSE 100 reached yet another historic peak.

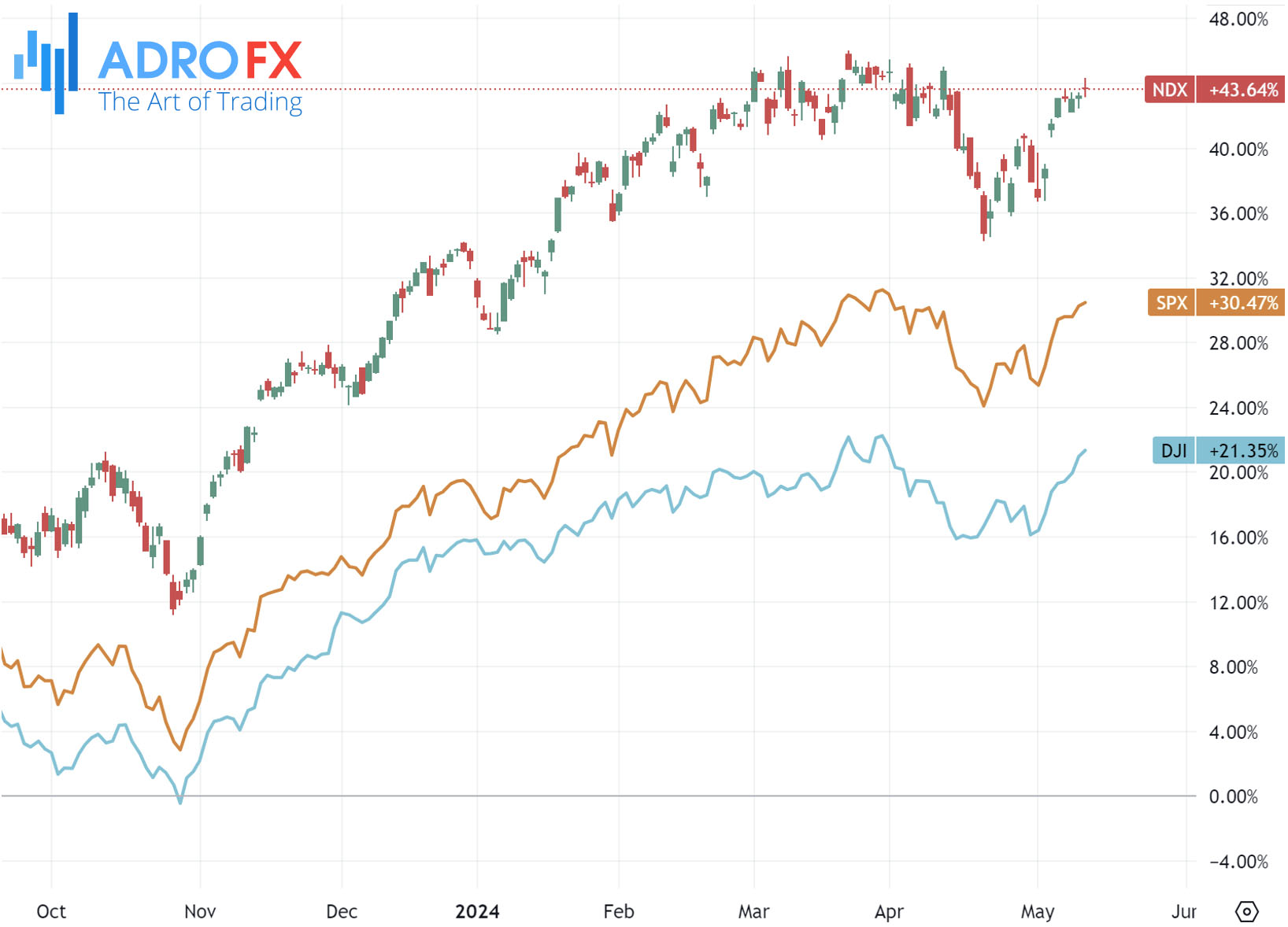

In the US, the Dow industrials index notched its eighth consecutive daily gain, contributing to overall weekly gains across the three major Wall Street indexes, although the Nasdaq ended the day marginally lower.

Strong performances across both Europe and the US, coupled with overnight gains in Asia, propelled MSCI's all-country world index to within 0.2% of a record closing high.

Investors in US equities found solace in the earnings season, with corporate results surpassing expectations on aggregate, noted Dec Mullarkey, managing director of investment strategy and asset allocation at SLC Management in Boston.

The Dow Jones Industrial Average advanced by 0.32%, the S&P 500 by 0.17%, and the Nasdaq Composite experienced a slight decline of 0.03%.

Despite initial declines, the dollar rebounded modestly as investors digested a reading on US consumer sentiment and parsed through numerous comments from Federal Reserve officials.

The University of Michigan's preliminary consumer sentiment reading for May stood at 67.4, marking a six-month low and falling short of economists' estimates of 76.0, as per a Reuters poll. Additionally, the one-year inflation expectation rose to 3.5% from 3.2%.

During the early European session on Monday, the USD/CAD pair is making a modest recovery near 1.3680. Concurrently, the USD Index maintains its positive stance around 105.30, as investors await key economic data from the United States. The final reading of the US CPI is scheduled for Wednesday, with expectations indicating a 3.4% year-over-year increase in April, compared to the 3.5% rise recorded in March.

Federal Reserve officials have emphasized the need for evidence of a downward trend in inflation before considering a reduction in the fed funds rate from its 23-year high. Dallas Fed President Lorie Logan stated that it remains unclear if current monetary policy is sufficiently tight to bring inflation down to the 2% target, advocating caution in cutting interest rates.

Meanwhile, the Canadian economy added 90,000 jobs in April, marking the most significant increase in 15 months and surpassing the estimated gain of 20,000, according to Statistics Canada. Despite this robust labor market performance, the decline in crude oil prices exerts downward pressure on the Loonie, given Canada's position as a leading oil exporter to the United States.

In another context, the Australian Dollar extended its losses on Monday, potentially influenced by the Reserve Bank of Australia's decision to maintain its interest rate at 4.35% last Tuesday. Despite speculation of a more hawkish stance following last week's inflation data surpassing expectations, the RBA opted for a neutral approach.

Moreover, New Zealand's Dollar continues to depreciate for the second consecutive session, trading around 0.6000 during the Asian session on Monday. This decline follows the release of the 2-year RBNZ Inflation Expectations (QoQ) for the second quarter, which fell to 2.33% from the previous quarter's 2.50%, sparking speculation of potential rate cuts by the Reserve Bank of New Zealand later in 2024.

In the UK, the Pound Sterling edges higher to near 1.2520 during the Asian session on Monday, possibly fueled by improved risk appetite. The GBP received a boost from higher-than-expected UK GDP figures released on Friday, indicating a 0.6% expansion in Q1 and signaling the end of a brief recession. However, dovish remarks from Huw Pill, Chief Economist at the Bank of England, hinted at possible rate cuts in the near future, tempering GBP gains.

Investors are keenly awaiting UK employment data on Tuesday, with expectations of an increase in Claimant Count Change for April. Additionally, the ILO Unemployment Rate (3M) is anticipated to reflect a rise in unemployed workers in the UK.

Furthermore, market participants are poised to closely monitor key US economic indicators scheduled for release this week, including the PPI on Tuesday, followed by reports on the CPI and Retail Sales on Wednesday.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates