What Will 2023 Be Like for Major Economies? | Daily Market Analysis

Key events:

- USA – ISM Manufacturing PMI (Dec)

- USA – JOLTs Job Openings (Nov)

- USA – FOMC Meeting Minutes

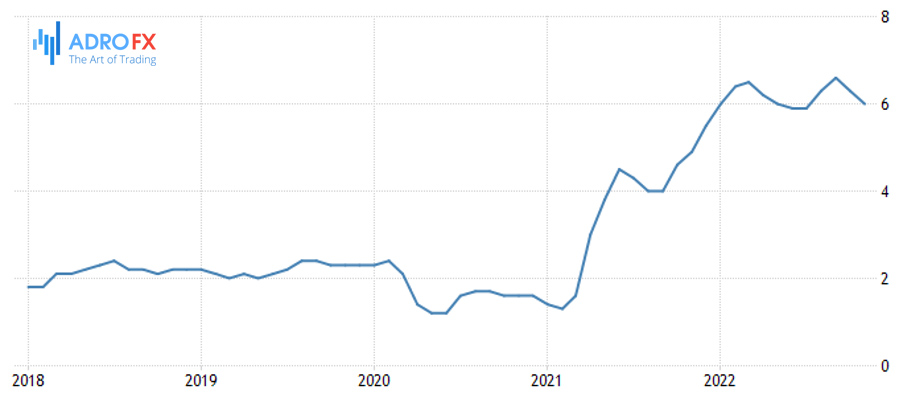

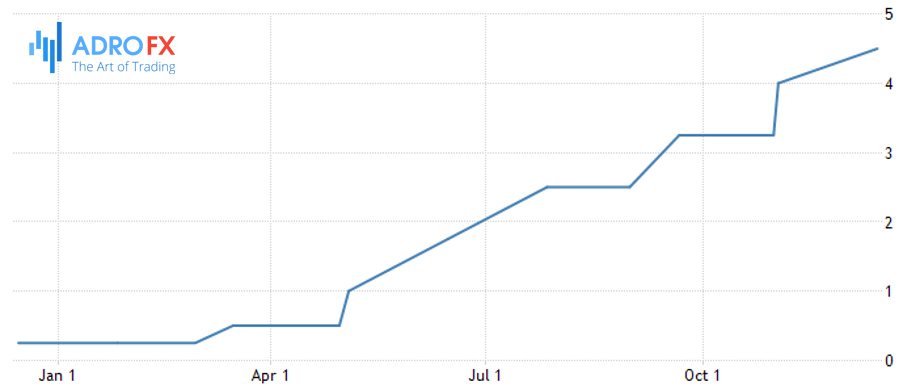

The classic year-end reviews here and there reminded us of the exceptional nature of the past year: the Russian aggression in Ukraine, the energy and food price shock, serious problems in the labor market, inflation that exceeded the central banks' target rates several times, which led to a tightening of monetary policy on the "whatever it takes" principle, etc.

Last year was a year of fundamental changes and a shift in geopolitical and economic benchmarks. Looking ahead, we can say that 2023 will see a change in the direction of key economic variables. Core inflation should fall significantly, central bank rates should reach their cyclical peak, and the U.S. and eurozone will spend part of the year in recession. 2023 can be considered a transitional year, paving the way for further disinflation, a gradual decline in rates, and a soft recovery in 2024.

Finally, the U.S. and the eurozone should spend part of the year in recession. This can be seen as the price to be paid to bring inflation back under control with tight monetary policy. Recessions are disinflationary because low demand reduces the price power of companies and slows wage growth.

This means that 2023 can be seen as a transition year, paving the way for gradual normalization in 2024. Normalization means a significant narrowing of the gap between observed and target inflation, allowing central banks to begin cutting interest rates, probably in the first half of 2024. This outlook should support investor appetite for risk and increase household and firm confidence, thereby contributing to the economic recovery.

While these general trends look very likely, the devil is in the details. The transition period in 2023 may be bumpier than expected. The baseline scenario calls for a short and shallow recession thanks to a few resilience factors, but the downturn could be more severe than expected.

Possible causes could be a new, significant, and prolonged increase in gas prices or a slower-than-expected decline in inflation, which could raise fears of rising interest rates and thereby hit demand. Rising rates in the past may also have a greater impact than expected, especially on the housing market and credit conditions.

Another question concerns normalization in 2024: What will it look like? This question is important because expectations about the nature of the economic recovery will influence the decisions of firms and households this year. The list of drivers of the recovery is long, but there is nonetheless reason to expect that the recovery will be mild, for at least two reasons. Traditionally, central banks aggressively cut interest rates when the economy enters a recession, but inflation will still be too high in this cycle. The rate cuts should come later and be more gradual than usual because of the slow decline in core inflation. This means less stimulus for final demand. Another factor is labor shortages. Companies are having trouble filling vacancies, which will likely make them reluctant to lay off staff during a recession. However, this also means slow job growth during the recovery.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates