US Stock Indices Soar on Earnings Optimism, Risk-Tolerant Investor Sentiment | Daily Market Analysis

Key events:

- Eurozone - ECB's Supervisory Board Member Jochnick Speaks

- USA - FOMC Member Williams Speaks

- USA - Core Retail Sales (MoM) (Sep)

- USA - Retail Sales (MoM) (Sep)

- USA - FOMC Member Bowman Speaks

- Eurozone - ECB's De Guindos Speaks

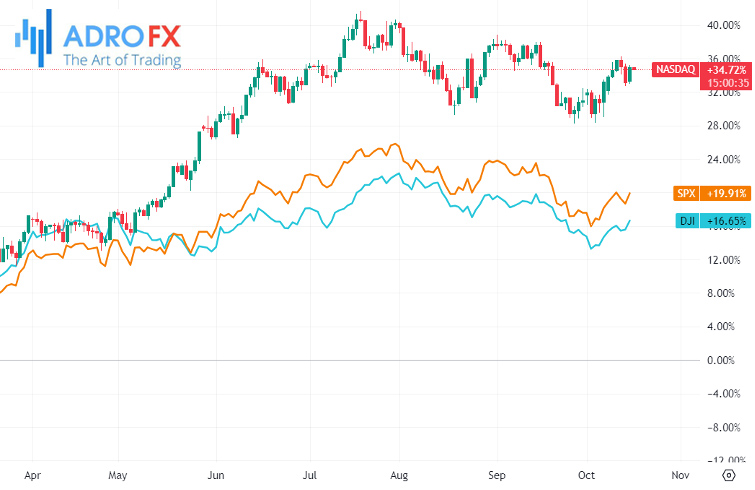

The major US stock indices ended Monday with substantial gains, driven by a wave of optimism as the earnings season commenced. Notably, transportation and small-cap shares also made significant advances during the trading day. While market observers kept a close watch on the ongoing Israeli conflict in Gaza, it was evident that investors adopted a more risk-tolerant stance on Monday.

The S&P 500 led the charge with an impressive 1.1% surge, while the Dow Jones Industrial Average gained 1%, equivalent to a remarkable 318-point increase. The Nasdaq wasn't far behind, recording a solid gain of 1.3%.

Big tech companies were at the forefront of this rally, with robust performances from Microsoft Corporation (NASDAQ: MSFT) and Alphabet Inc Class A (NASDAQ: GOOGL). Investors appeared undeterred by the increasing Treasury yields.

In contrast, Apple Inc (NASDAQ: AAPL) faced pressure due to concerns about lower sales of its iPhone 15 in China during the initial weeks following its release, in comparison to the iPhone 14, indicating subdued demand. Sales of the iPhone 15 dropped by a double-digit percentage compared to its predecessor, primarily due to stiff competition from Huawei’s Mate 60 Pro.

Jefferies' decision to upgrade Pfizer Inc (NYSE: PFE) from a "hold" to a "buy" rating made headlines, as the pharmaceutical giant's plan to cut costs by $3.5 billion was expected to boost earnings. This announcement triggered a 4% jump in Pfizer's shares. Pfizer had recently revised its full-year earnings and revenue guidance downward, citing $5.5 billion in write-downs for Q3, related to lower-than-expected sales of its COVID-19 vaccine and treatment. Remarkably, these COVID-19 vaccine-related sales accounted for less than 15% of Pfizer's overall revenue of $12.73 billion reported in the second quarter.

Turning to the precious metals market, gold prices continued to decline on Tuesday, extending losses from the previous session. This decline was primarily due to market caution ahead of several upcoming indicators related to the US economy and speeches from Federal Reserve officials.

Although gold initially saw substantial gains during the Israel-Hamas conflict, as investors sought safe havens, the trend reversed this week following a higher-than-expected US inflation reading, which raised concerns about rising interest rates. The absence of an immediate escalation in the conflict reduced short-term safe-haven demand.

The morning also brought mixed signals from Australia and New Zealand. Surprisingly hawkish minutes from the Reserve Bank of Australia meeting earlier this month led to a slight increase in the Australian dollar. In contrast, the New Zealand dollar weakened as a slowdown in inflation suggested that further rate hikes in New Zealand were now less likely.

Market attention is currently focused on US retail sales and industrial production data scheduled for later on Tuesday. Any signs of resilience, particularly in retail spending, may indicate a sustained inflationary outlook. Last week, US consumer inflation exceeded expectations, raising concerns that the Federal Reserve may maintain a hawkish stance for an extended period to address persistent inflation.

Meanwhile, the GBP/USD pair retraced recent gains and was trading lower around 1.2200 during the Asian trading session on Tuesday. This movement suggests a period of consolidation, possibly reflecting market uncertainty about the future direction of the US Federal Reserve's monetary policy.

The US Dollar Index made an attempt to recover from recent losses, trading slightly higher around 106.30 at the time of this report. However, the US Dollar remained under pressure, and this can be attributed to dovish comments made by various Federal Reserve officials. These comments implied that there are no expectations for further interest rate hikes for the remainder of 2023. The dovish stance underscores the central bank's cautious approach, indicating a reluctance to tighten monetary policy in the current economic environment.

This week, a series of Federal Reserve officials are set to deliver speeches, with particular attention on Federal Reserve Chair Jerome Powell's remarks on Thursday. Powell's comments are closely anticipated following the recent robust inflation readings, given his prior indications of prolonged higher interest rates during the Fed's previous meeting.

Higher interest rates typically negatively impact gold, as they increase the opportunity cost of investing in the precious metal. This trend has weighed on gold prices over the past year and is expected to limit substantial gains until the Federal Reserve initiates interest rate cuts.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates