US Retail Sales Drop 1% as Fed Predicts More Rate Hikes | Daily Market Analysis

Key events:

- Eurozone – ECB President Lagarde Speaks

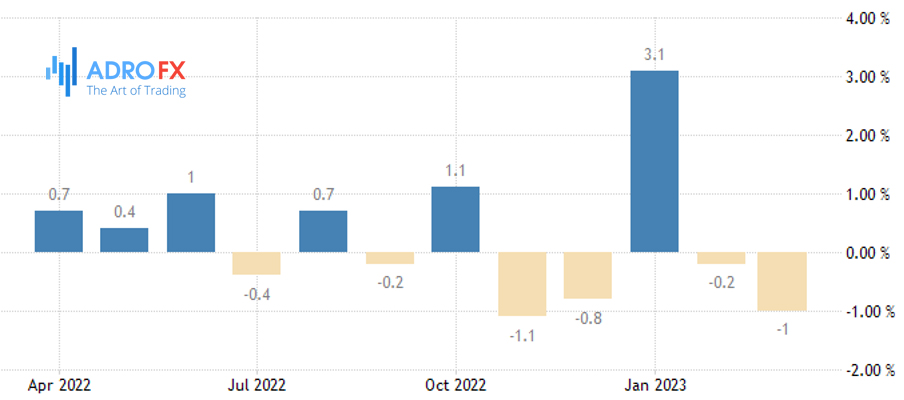

In March, there was a significant drop of 1% in US retail sales and consumer sentiment remained at a low point reminiscent of the Great Recession. Despite low inflation numbers being the focus of the markets last week, it may be worth it because both core inflation and inflation expectations have actually increased. This is likely to be concerning for the Federal Reserve, and the recent data trend is more likely to keep them on a tightening trajectory rather than cause them to change direction. The data from last week was negative for the economy but positive for Fed rate hikes, indicating that there will be several more rate hikes to come. This is why, despite reaching new highs in New York on Friday, the market is beginning to tire again. These high valuations are unlikely to persist given the current state of the real world's fundamentals.

The latest economic data showed signs of a cooling economy after the Federal Reserve's sharp reaction to inflation through successive interest rate hikes. Futures traders expect another quarter-point rate hike at the Fed's next meeting in May.

Atlanta Fed Chairman Rafael Bostic said Friday that a quarter-point rate hike could mean the central bank could end its tightening cycle with some confidence in pushing inflation toward the 2 percent target.

The US stock market rallied after record earnings data from JPMorgan Chase (NYSE: JPM) opened the first-quarter reporting season and retail sales data was weaker than expected.

JPMorgan, Citigroup (NYSE: C), and Wells Fargo (NYSE: WFC) beat expectations for a quarter that was marred by turmoil from the collapse of two major banks.

Following the release of the data, Dollar shorts became nervous and tried to cover their positions heading into the weekend. EUR/USD dropped 0.44% to 1.0987 after trading at a high of 1.1067.

The Greenback slightly rose against the Japanese Yen to 133.85 from 133.65. Incoming Bank of Japan Governor Ueda stated that the central bank would maintain the current low-interest rates.

US Treasury yields rose, with the benchmark 10-year treasury bond rate increasing to 3.51% from 3.39%. The 2-year US bond yield settled at 4.10% (3.96%). Other global bond rates also rose but to a lesser extent.

The Australian Dollar fell to 0.6700 from 0.6775 Friday. New Zealand's Kiwi declined to 0.6210 from 0.6300. USD/CAD remained almost unchanged at 1.3360.

GBP/USD decreased to 1.2415 (1.2445). Against the Asian and Emerging Market currencies, the US Dollar mostly rose. USD/CNH increased to 6.8710 from 6.8670.

The upcoming week's economic calendar has a light start with New Zealand's Business NZ Services Index, and China's PBOC-Year Medium Term Lending Facility Rate expected to remain unchanged. Italy's Annual Final March Inflation Rate will be the first European data, followed by China's March Foreign Direct Investment data. Canada will release its Final February Wholesale Sales report, while the US will release its New York Empire State Manufacturing Index for April. The rest of the week will be busier with the release of Australia's RBA Meeting Minutes, China's Retail Sales, Industrial Production, and Fixed Asset Investment, as well as GDP. Germany will release its April ZEW Economic Sentiment Index, and various European nations including the UK will release their inflation rates and producer prices.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates