US Market Shows Modest Gains Amid Manufacturing Concerns, Gold Prices Dip on Rate Hike Warnings | Daily Market Analysis

Key events:

- Australia - RBA Meeting Minutes

- UK - Average Earnings Index +Bonus (Mar)

- UK - Claimant Count Change (Apr)

- USA - Core Retail Sales (MoM) (Apr)

- USA - Retail Sales (MoM) (Apr)

- Canada - Core CPI (MoM) (Apr)

- Eurozone - ECB President Lagarde Speaks

On Monday, the S&P 500 and the Dow closed with slight increases following the release of manufacturing data that raised concerns about a potential slowdown in the US economy. This development could contribute to easing inflationary pressures amid ongoing discussions regarding the debt ceiling. However, the Nasdaq received a boost from the upward movement of Meta shares.

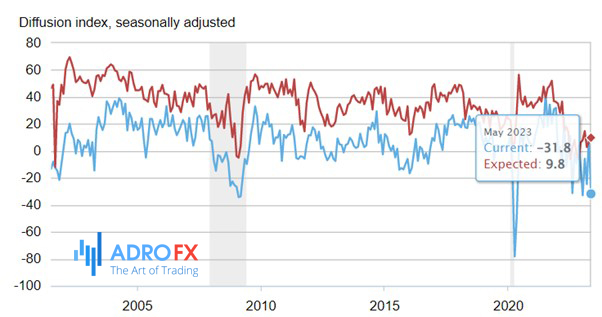

The New York Federal Reserve's "Empire State" index, which measures manufacturing activity in New York State based on current business conditions, experienced a significant decline in May. The index recorded a reading of -31.8, falling short of the anticipated -3.75.

The US economy is currently facing significant challenges. With the looming threat of the 'Great US Debt Default of 2023,' there is a glimmer of hope that the debt ceiling will be raised in time, as it has been done before.

In addition, recent comments from various Federal Reserve Presidents suggest that they expect interest rates to remain higher for a longer period. This raises questions about whether the Federal Reserve will pause its tightening cycle at the next meeting. Several Fed members expressed doubts about the sustainability of a downward trajectory for inflation.

As we have been forecasting for some time, inflation is stabilizing at an uncomfortably high level, making it an unsuitable environment for rate cuts. The belief in rate cuts this year is merely wishful thinking to avoid a full-blown banking crisis. Rate cuts may not even occur next year. We might be entering a new normal where rates can go higher than desired due to persistent inflation.

This economic reality poses significant challenges for all US asset classes. The risks of debt default, stubborn high inflation, a decline in manufacturing, ongoing large-scale layoffs, banking crises, and the prospect of higher rates for an extended period create a negative backdrop for current pricing levels.

Unfortunately, there may be an excessive amount of hope already factored into stock, bond, and property prices at their current levels, considering the projected flat, or at best, sluggish US economy in the coming years.

As for the forex market, the future movements of the EUR/USD currency pair are expected to be predominantly influenced by the performance of the US dollar. The foreign exchange markets are primarily paying attention to developments in the United States, particularly the ongoing discussions and uncertainties surrounding the debt limit, as well as speculations regarding the extent of future monetary policy easing by the Federal Reserve.

On the other hand, the economic calendar in the Eurozone remains relatively uneventful this week, except for the ZEW surveys and the release of preliminary 1Q GDP figures today.

While remarks from European Central Bank (ECB) speakers are of interest, their recent impact on the Euro has been limited.

At the same time, the Bank of England's (BoE) policy decision in June will heavily depend on two critical data releases: wages and inflation. The wage data is scheduled to be released on Tuesday, and it is important to note that wage figures have displayed significant volatility in recent times. Consequently, the outcomes of these releases are expected to have a pronounced impact on the performance of the British pound.

Few economists anticipate a slowdown in wage growth following the notable surge witnessed last month. Such a scenario could potentially sway the Monetary Policy Committee (MPC) towards maintaining the current policy stance at the June meeting. Currently, market expectations factor in a 20-basis point tightening, but there are notable downside risks for the sterling. As a result, we may see a strengthening of the Euro against the pound, with the EUR/GBP currency pair likely to rebound above 0.8800 by the end of this month.

Meanwhile, gold prices experienced a slight decline in early Asian trade on Tuesday. This dip came as a result of multiple Federal Reserve officials cautioning that interest rates might continue to increase, citing persistent inflation and a strong labor market.

Although gold saw some gains in the previous session, they were modest as traders exercised caution in anticipation of a series of important U.S. economic indicators scheduled for release this week. Among these readings, retail sales and industrial production data are expected later in the day, further contributing to the cautious market sentiment surrounding gold.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates