Mixed Markets, Bank of England Rate Hike, Regional Banks Falter | Daily Market Analysis

Key events:

- UK - GDP (MoM) (Mar)

- UK - GDP (YoY) (Q1)

- UK - GDP (QoQ) (Q1)

- UK - Manufacturing Production (MoM) (Mar)

- UK - Monthly GDP 3M/3M Change (Mar)

Both European and US markets had mixed sessions yesterday, with concerns over a slowdown in the Chinese and US economies leading to a selloff in commodity prices. This, in turn, had a negative impact on the basic resources and energy sectors.

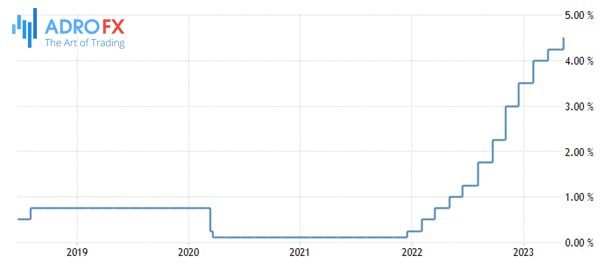

Yesterday, the Bank of England (BoE) raised rates by 25bp for the 12th time and Governor Bailey suggested that further rate hikes may be possible. Although the BoE expects inflation to fall rapidly this year, Bailey acknowledged that inflation remains too high and reiterated the need for further rate increases to bring it down. He also noted that the lagging effects of previous rate hikes will have a greater impact on the economy in the coming quarters. Furthermore, British policymakers made the most significant upgrade to their growth projections since 1997, according to Bloomberg. Despite this positive news, Cable fell and briefly dipped below the 1.25 level, mostly due to the overall strength of the US dollar.

Despite weaker-than-expected US PPI data, the highest number of jobless claims since October 2021, the greenback rallied above a bearish trend line that had been in place for two months.

Regional banks have re-entered the spotlight today as PacWest's shares plunged 20% due to a significant loss in deposits, reminding the market of ongoing issues with smaller banks. Other regional banking shares also dropped before the opening bell, leading to pressure on major indexes. While one bank's deposit decline may not indicate broader problems, the market is hypersensitive to any issues affecting this sector.

In addition, concerns surrounding the debt ceiling remain a delicate issue, as officials in Washington D.C. prepare for high-level discussions on Friday. Although there were no signs of progress after Tuesday's meeting, stock market volatility has not yet reflected any significant strain. However, approaching the June 1 deadline with no deal could change this. The market is also being affected by Walt Disney Company's weak shares following the company's quarterly results, which showed further subscriber losses for its TV streaming platform.

Is yesterday's market movement only a temporary move towards safe-haven assets or is it likely to continue? Looking at the EUR/USD chart, it seems that the inability to break through the 1.10/1.11 resistance level suggests a bearish sentiment, indicating a potential downside correction before a rebound toward the medium-term target of 1.12.

In the stock market, the S&P 500 remained mostly unchanged, while bank selloffs weighed it down. However, the Nasdaq 100 continued to climb, reaching new highs not seen since last summer, likely boosted by falling yields and an increased appetite for Big Tech stocks.

Gold's attempt to hit new record highs may have been put on hold due to recent inflation data not providing the expected boost. The gold rally was already losing steam and required something more substantial to continue. While a Fed pause is expected in June, traders are already considering when the central bank could potentially justify reversing course. The next few months will be crucial in determining that, and a slight decrease in inflation and an increase in jobless claims have not impacted that prospect.

Yesterday, Turkey's BIST100 surged almost 8% after Muhammer Ince, one of the candidates for the presidential election, withdrew from the race amidst allegations of bribery and a sex tape scandal. Although his votes will still be counted, his withdrawal increases the chances of President Erdogan's defeat in the election. Meanwhile, the USD/TRY continues to rise gradually despite Turkey's ultra-loose monetary policy and deeply negative real rates. This is due to the Central Bank of Turkey's massive FX intervention program that has kept the Turkish lira at levels above the fair market value against major currencies. However, this program may not last, and any misstep, such as an Erdogan defeat in the election, could trigger an explosion in the Turkish lira's value.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates