S&P 500 Hits New High Amid Fed's Rate Cut Signals | Daily Market Analysis

Key events:

- USA - Initial Jobless Claims

- USA - PPI (MoM) (May)

- USA - 30-Year Bond Auction

On Wednesday, the S&P 500 achieved an intraday record high before closing with a gain, despite the Federal Reserve indicating only a single rate cut for this year. Positive sentiment was buoyed by data revealing that May's inflation was cooler than anticipated.

The Dow Jones Industrial Average experienced a slight decline, dropping 30 points, or 0.1%, while the S&P 500 climbed 1%, reaching a record peak of 5,446.53. The NASDAQ Composite saw an impressive increase of 1.8%.

The NZD/USD pair continues its rally around 0.6195, even as the US Dollar weakens during the early Asian session on Thursday. Despite a softer-than-expected US CPI inflation report for May, which pushed the USD Index down to 104.25, the Federal Reserve's hawkish hold has helped the DXY regain some stability.

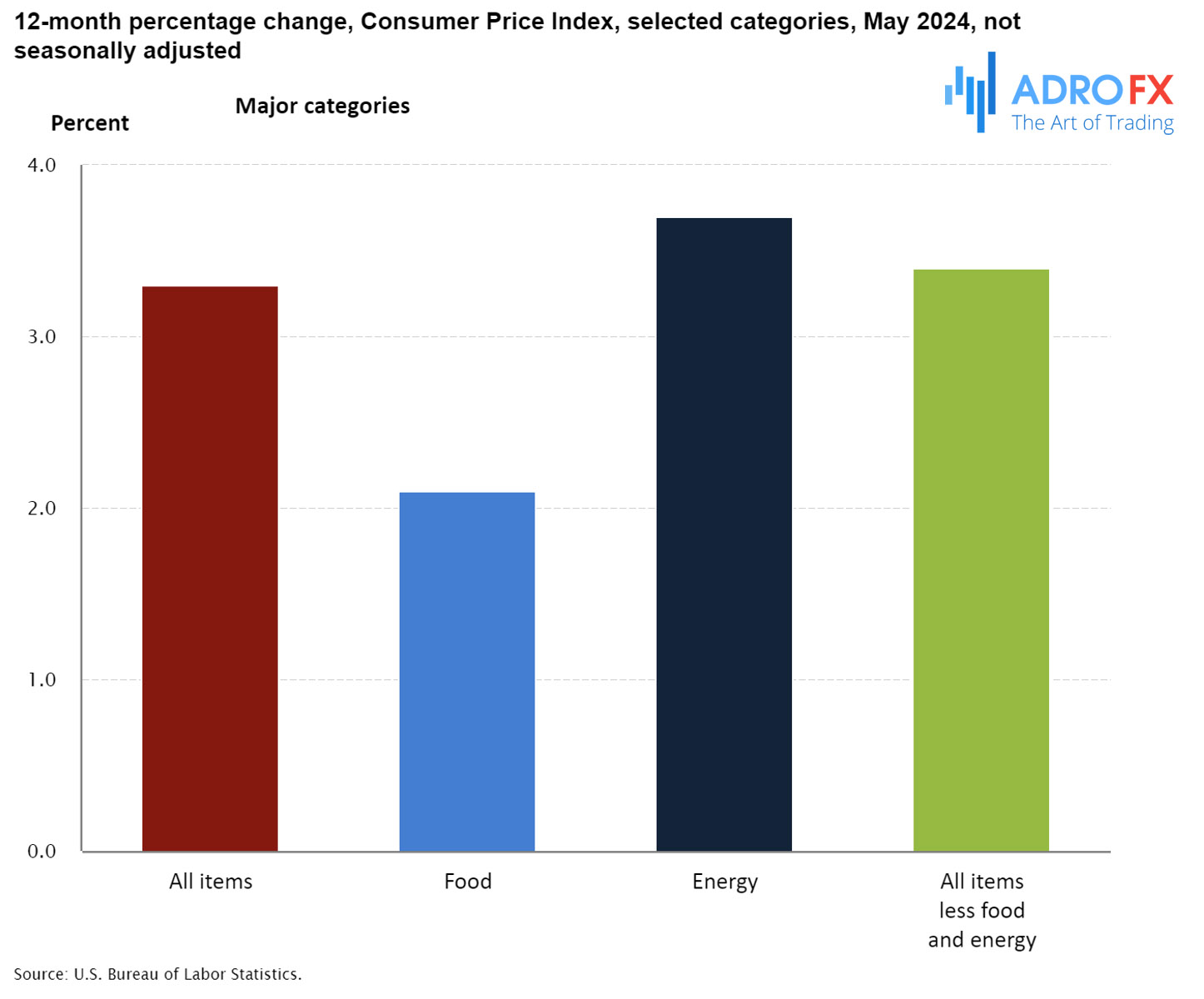

On Wednesday, the US Bureau of Labor Statistics reported that inflation in the United States cooled more than anticipated in May. The CPI rose 3.3% year-over-year, compared to the previous reading and expectations of 3.4%. Monthly, the CPI held flat in May, marking the first time since July 2022, as opposed to a 0.3% gain in April.

Core CPI, which excludes volatile food and energy prices, increased 3.4% year-over-year in May, down from 3.6% in April and below the 3.5% estimate. Monthly, core CPI rose by 0.2% in May.

This softer CPI report has increased the likelihood of Fed rate cuts this year, putting selling pressure on the USD. According to the CME FedWatch tool, investors now see a 73% chance of a rate cut from the Fed in September, up from 53% prior to the CPI data release.

Meanwhile, the Fed held interest rates steady at their current range of 5.25% to 5.5% during its June meeting on Wednesday, as expected by market participants. Fed Chair Jerome Powell stated that the restrictive monetary policy is effectively addressing inflation, but the Fed will wait for sufficient progress before making further adjustments. Following the Fed's hawkish hold, the Greenback recovered some lost ground.

In contrast, China’s CPI inflation remained steady at 0.3% year-over-year in May, falling short of the expected 0.4% growth. China’s PPI declined by 1.4% year-over-year in May, an improvement from the previous 2.5% drop and better than the forecasted 1.5% decrease. However, this mixed Chinese economic data had little effect on the New Zealand Dollar, despite China being New Zealand's largest trading partner.

The Reserve Bank of New Zealand's hawkish approach continues to bolster the Kiwi, providing a positive momentum for the NZD/USD pair. The RBNZ is vigilant about ongoing domestic inflation and signals a heightened possibility of future rate hikes. It is anticipated that the New Zealand central bank will maintain its current policy until at least mid-2025.

Despite favorable employment data, the Australian Dollar slipped on Thursday. Employment figures showed an increase of 39.7K jobs in May, exceeding the anticipated rise of 30.0K and the previous month's increase of 38.5 K. The Unemployment Rate also improved to 4.0%, down from April's 4.1%.

Australian Treasurer Jim Chalmers emphasized the importance of Chinese Premier Li Qiang's visit to Australia, pointing out underlying weaknesses in China's economy and advising against expecting an immediate recovery. Additionally, Australia's NAB Business Confidence index dropped to -3 points in May, the lowest in six months and the first negative reading since last November. Business Conditions also declined to 6 points, slightly below the long-term average.

The Japanese Yen gave up recent gains on Thursday as the US Dollar advanced following the Federal Reserve's hawkish stance, boosting the USD/JPY pair. The Yen may experience limited downside as traders exercise caution ahead of the Bank of Japan’s policy decision on Friday. The BoJ is likely to leave interest rates unchanged, but traders will be alert for any announcements about potential cuts in the central bank's monthly bond purchases.

Gold prices encountered fresh supply during the Asian session on Thursday, ending a three-day winning streak and retreating from the weekly high around the $2,341-$2,342 region. The Fed's hawkish stance increased US Treasury bond yields, supporting the USD's recovery from a multi-day low and negatively impacting gold prices. However, geopolitical tensions in the Middle East and renewed political uncertainty in Europe may help prevent deeper losses for gold.

The USD/CAD pair ended its three-day losing streak, trading around 1.3730 during early Asian hours on Thursday. Bank of Canada Governor Tiff Macklem noted that there is a limit to how far the Canadian central bank can diverge from the Fed's rate policies, though they are not yet close to that limit. Recently, the BoC lowered its benchmark rate by 25 basis points to 4.75%, and markets are pricing in nearly 150 basis points of additional cuts over the next few years. This divergence in interest rates between Canada and the US could support the USD against the Canadian Dollar in the near term.

Investors are keenly awaiting the release of the US weekly Initial Jobless Claims and PPI on Thursday to gain more insights into the economic conditions in the United States.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates