S&P 500 and Dow Climb on Cooling Inflation, Global Currencies React to Fed Outlook | Weekly Market Analysis

Key events this week:

Monday, September 29, 2025

- USA - Fed Waller Speaks

- UK - MPC Member Ramsden Speaks

- USA - FOMC Member Williams Speaks

- USA - US President Trump Speaks

Tuesday, September 30, 2025

- China - Manufacturing PMI (Sep)

- Australia - RBA Interest Rate Decision (Sep)

- UK - GDP (QoQ) (Q2)

- UK - GDP (YoY) (Q2)

- USA - Chicago PMI (Sep)

- USA - CB Consumer Confidence (Sep)

- USA - JOLTS Job Openings (Aug)

Wednesday, October 1, 2025

- Eurozone - CPI (YoY) (Sep)

- USA - ADP Nonfarm Employment Change (Sep)

- USA - S&P Global Manufacturing PMI (Sep)

- USA - ISM Manufacturing PMI (Sep)

- USA - ISM Manufacturing Prices (Sep)

- USA - Crude Oil Inventories

Thursday, October 2, 2025

- USA - Initial Jobless Claims

Friday, October 3, 2025

- USA - Average Hourly Earnings (MoM) (Sep)

- USA - Nonfarm Payrolls (Sep)

- USA - Unemployment Rate (Sep)

- USA - S&P Global Services PMI (Sep)

- USA - ISM Non-Manufacturing PMI (Sep)

- USA - ISM Non-Manufacturing Prices (Sep)

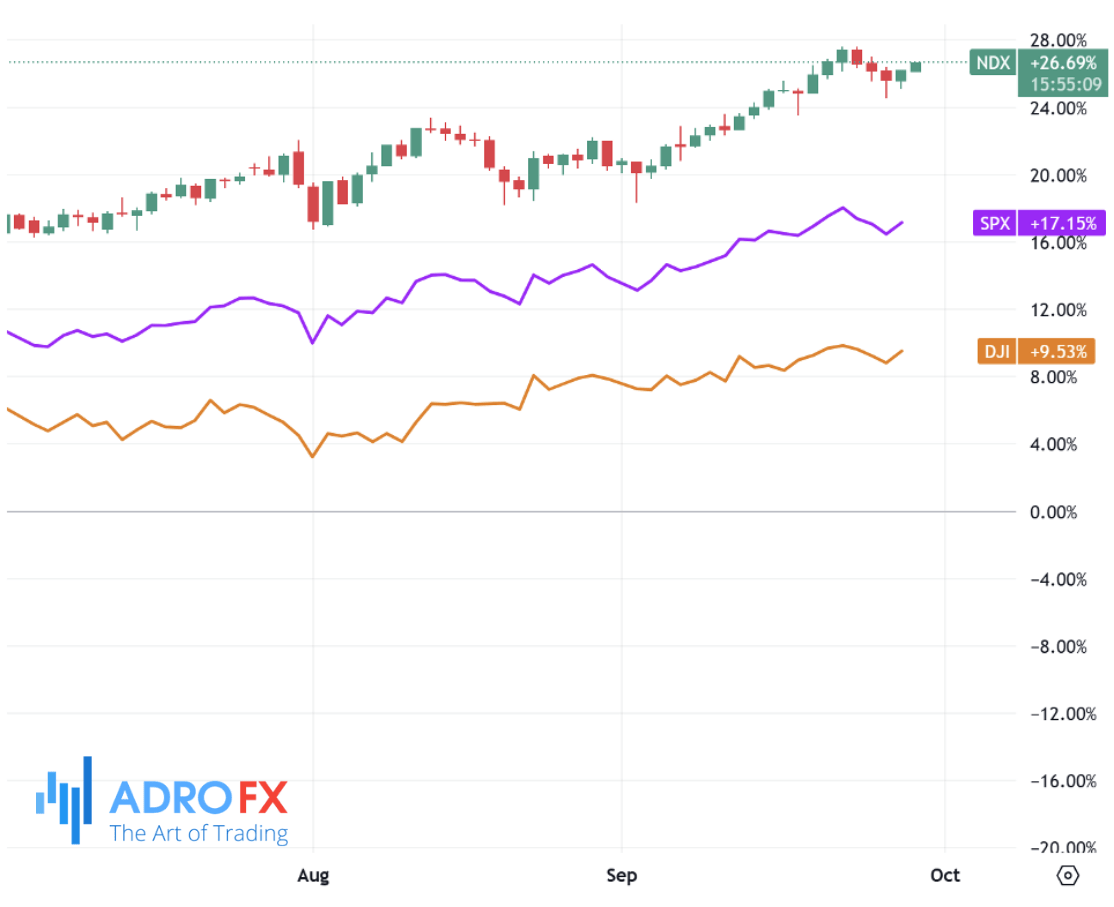

Wall Street ended the week on firmer ground as major US equity indices shook off a three-day losing streak. Investors cheered a softer bond market, with Treasury yields retreating after the latest inflation data landed in line with expectations. The S&P 500 jumped 0.6%, while the Dow Jones Industrial Average added 350 points, or 0.8%, to notch a strong daily performance. The Nasdaq Composite also pushed higher, climbing 0.4%, with technology shares benefiting from a more risk-friendly environment.

Market sentiment turned positive despite fresh trade tariffs announced by President Donald Trump, which had initially weighed on investor confidence earlier in the week.

The rebound was closely tied to the latest reading on the Federal Reserve’s preferred inflation gauge, the Personal Consumption Expenditures index. Core PCE inflation remained steady at 2.9% year-on-year, exactly in line with forecasts, while the monthly pace held flat at 0.2%. Headline PCE showed a slight acceleration to 0.3% month-on-month and 2.7% annually. Though inflationary pressures remain above the Fed’s target, markets welcomed the fact that the figures did not surprise to the upside, calming fears of a renewed hawkish pivot. Analysts noted that the US economy has now absorbed nearly eight months of tariff-driven price pressures, with core inflation returning to levels last seen in March 2024.

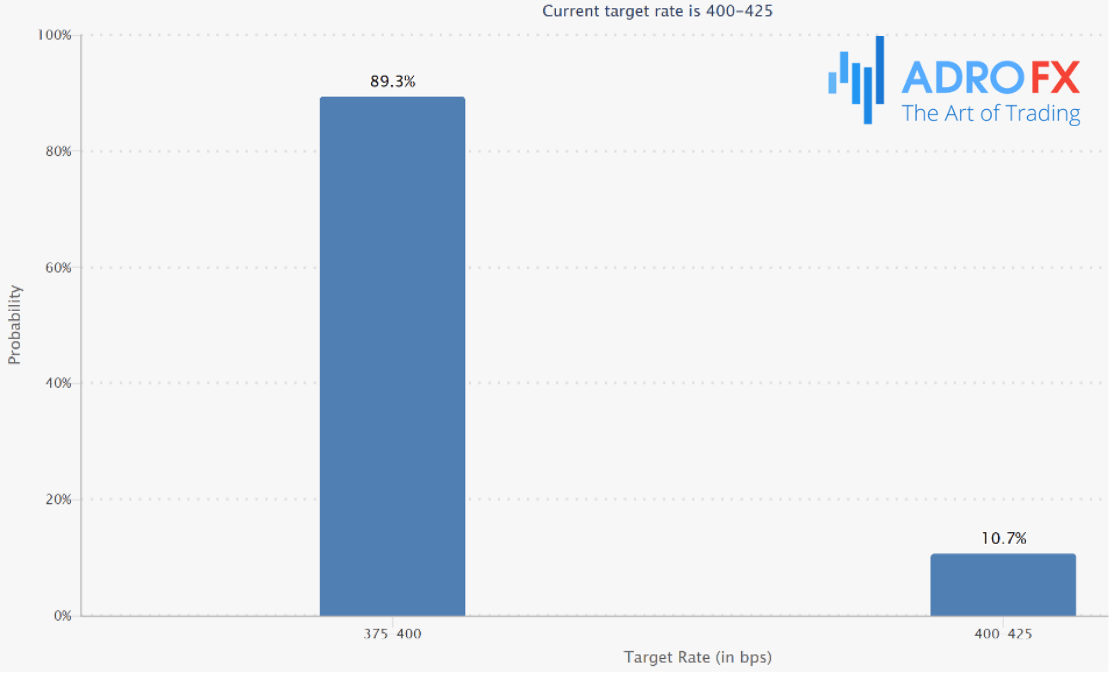

This backdrop leaves the central bank on course to ease policy further, as the labor market continues to show signs of cooling. Futures markets tracked by the CME FedWatch tool point to nearly 90% odds of another 25-basis-point rate cut at the October 25 meeting. Such a move would follow September’s reduction, marking two consecutive trims as policymakers attempt to balance moderating growth with still-sticky price levels. Fed Chair Jerome Powell and other officials have made clear that decisions remain data dependent, but traders are increasingly confident that the easing cycle has room to extend into year-end.

CME Group, target rate probabilities for 29 Oct 2025 Fed meeting

On the currency front, the US dollar slipped against several peers as investors braced for political uncertainty at home. The looming risk of a government shutdown beginning October 1 weighed on the greenback, sparking demand for higher-yielding currencies. The Australian dollar advanced for a second straight session, building momentum against its US counterpart. Support for the Aussie was bolstered by fading expectations of near-term policy easing from the Reserve Bank of Australia. August consumer price data surprised to the upside, prompting traders to assign only a small probability of cuts at the September meeting and slightly higher odds for November.

Domestic fiscal news also influenced sentiment, as Canberra reported a budget deficit of A$10 billion for the year ending June 2025. While a deficit replaced two consecutive surpluses, the shortfall was substantially smaller than the Treasury’s forecast of nearly A$28 billion, suggesting fiscal conditions remain healthier than feared.

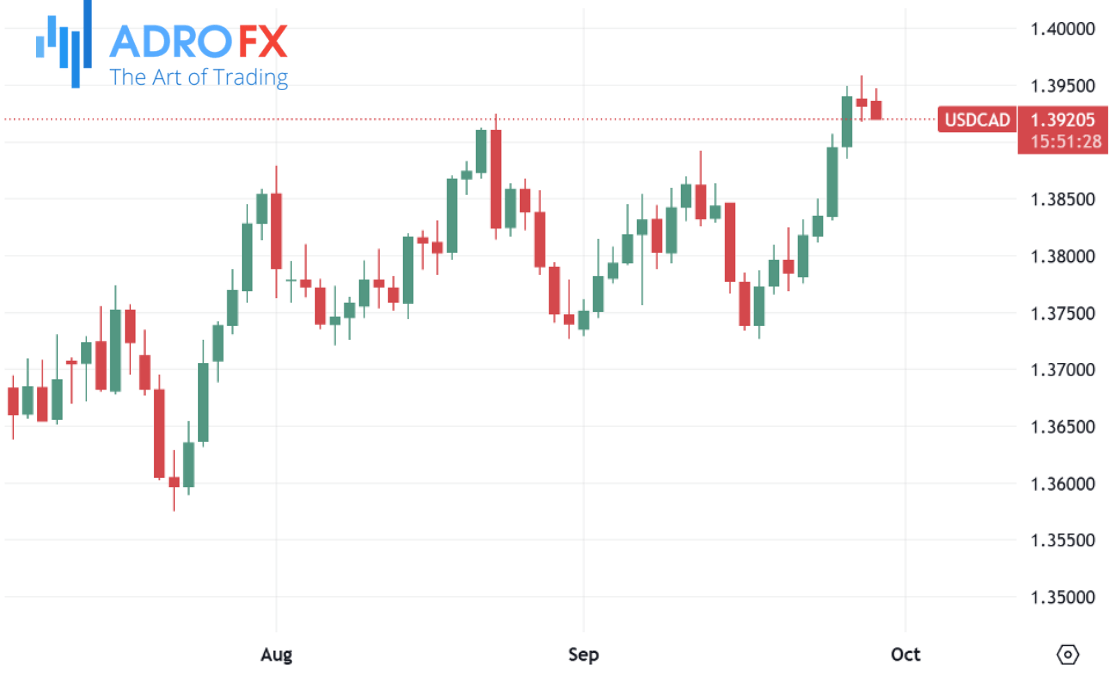

The Canadian dollar, however, paused its recent rally. After five straight sessions of gains, USD/CAD edged lower to 1.3920 following a retreat from Friday’s four-month peak of 1.3958. The pair was influenced by the US inflation report and weakening dollar, though the downside remained limited by energy market headwinds. Crude oil prices hovered near $65 per barrel, reflecting concerns about oversupply. Iraq’s Kurdistan region resumed exports for the first time in two and a half years under a deal with Baghdad and international firms. Initial flows of up to 190,000 barrels per day are set to reach Turkey’s Ceyhan port, adding barrels to an already saturated global market.

Meanwhile, the New Zealand dollar held modest gains around 0.5770 in early Asian trading. The Kiwi benefited from dollar softness tied to shutdown fears, though its longer-term outlook remains weighed down by expectations for additional Reserve Bank of New Zealand rate cuts. Weak second-quarter GDP data and a widening trade deficit have heightened pressure on policymakers to loosen policy further. Anna Breman is set to take over as RBNZ Governor in December, but acting Governor Christian Hawkesby will preside over the upcoming October and November meetings, where additional easing is now the base case.

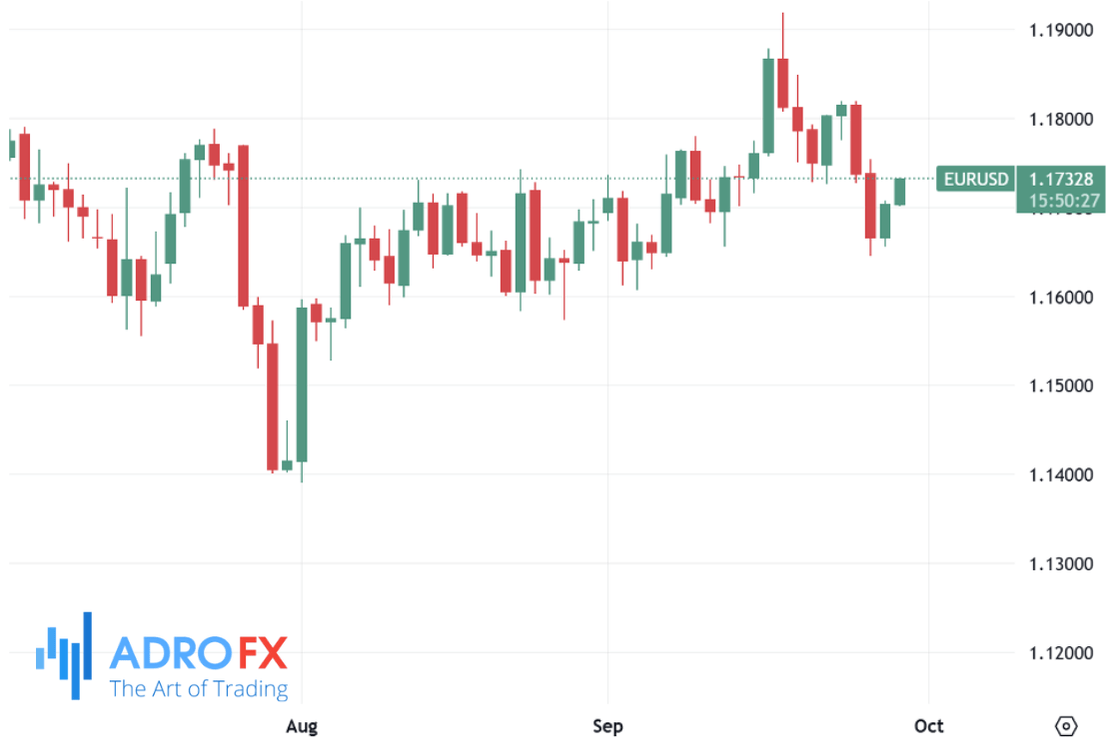

The euro also found support, extending its recovery for a second day and trading near 1.1720. Markets are increasingly convinced that the European Central Bank has reached the latter stages of its easing cycle after opting for a second consecutive rate hold in September. Eurozone data continues to paint a mixed picture, with services rebounding modestly while manufacturing remains under strain. Investors are closely monitoring the next steps from policymakers, who face the challenge of nurturing growth while avoiding a prolonged period of below-target inflation.

Sterling managed to edge higher as well, with GBP/USD climbing toward 1.3415. The pound has been resilient on expectations that the Bank of England will keep rates steady at 4.0% for the rest of the year. Persistent inflationary pressures in the UK economy make immediate cuts unlikely, lending support to the currency. Traders are watching upcoming domestic data closely to gauge whether the central bank will be able to hold its line amid ongoing cost-of-living concerns.

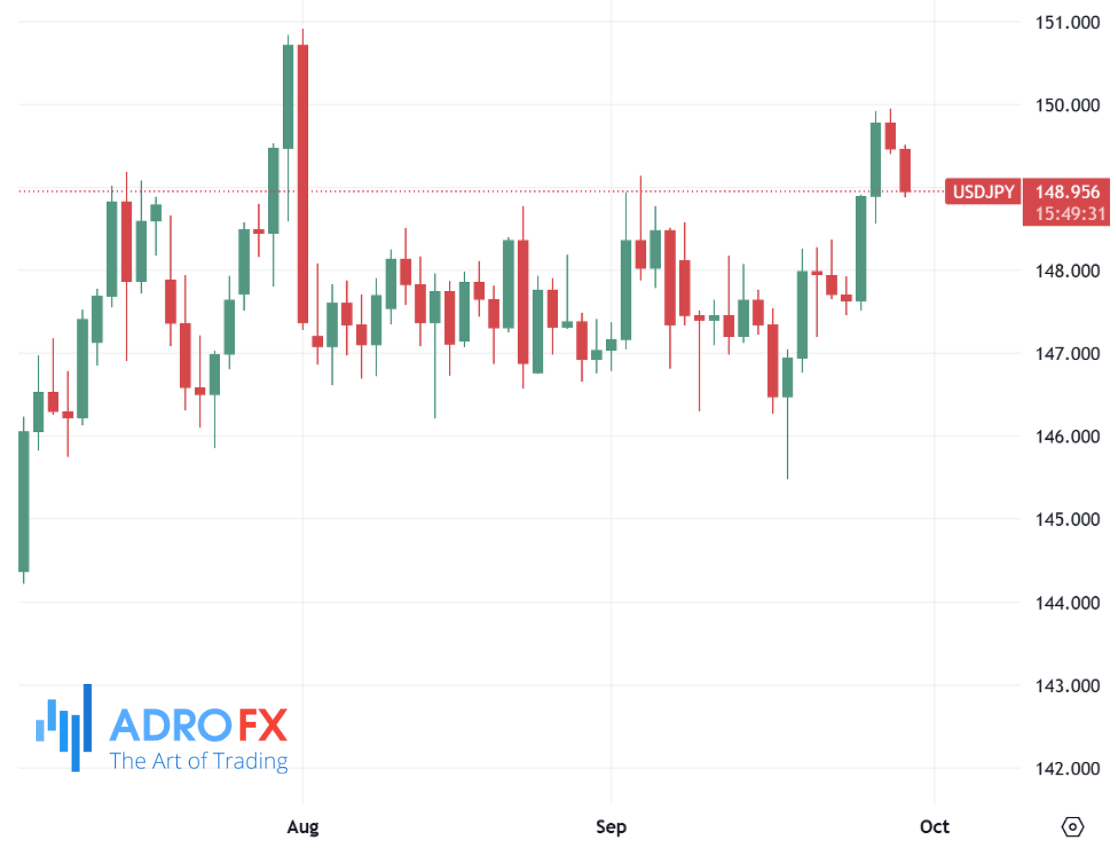

In Asia, the Japanese yen weakened slightly, with USD/JPY slipping to around 149.50. Domestic political uncertainty has added a new layer of complexity for yen traders. The ruling Liberal Democratic Party is scheduled to hold leadership elections on October 4, and the outcome could have implications for monetary policy. A dovish-leaning winner might encourage the Bank of Japan to delay its next rate hike, keeping yields low and limiting the yen’s attractiveness. Still, with US yields softening, the pair remains vulnerable to further volatility.

As the week gets underway, investor attention will shift back to US monetary policy communications. Several Federal Reserve officials are scheduled to speak on Monday, including Governor Christopher Waller, Cleveland Fed President Beth Hammack, St. Louis Fed President Alberto Musalem, New York Fed President John Williams, and Atlanta Fed President Raphael Bostic. Their remarks could provide further clarity on how the central bank views inflation, employment trends, and the risks posed by political uncertainty in Washington.

The combination of easing inflation, shifting interest rate expectations, and geopolitical developments has left global markets finely balanced. Equities are finding support from the prospect of further Fed easing, while currencies are adjusting to domestic policy divergences and political risks. Commodities, meanwhile, remain caught between demand concerns and supply fluctuations. As traders look ahead, the interplay between central bank policy paths, fiscal headlines, and global trade will continue to set the tone for both risk sentiment and asset price direction.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates