Markets Rally on Jobs Surprise and Renewed Hopes for US-China Trade Progress | Weekly Market Analysis

Key events this week:

Wednesday, June 11, 2025

- USA - Core CPI (MoM) (May)

- USA - CPI (MoM) (May)

- USA - CPI (YoY) (May)

- USA - Crude Oil Inventories

- USA - 10-Year Note Auction

Thursday, June 12, 2025

- UK - GDP (MoM) (Apr)

- USA - Initial Jobless Claims

- USA - PPI (MoM) (May)

- USA - 30-Year Bond Auction

US stocks surged into the weekend with a powerful rally on Friday, buoyed by encouraging employment data and a surprise announcement that US and Chinese officials will meet on Monday to revive trade talks. The news helped restore investor confidence that had been shaken in recent sessions. The S&P 500 leaped 1%, the Dow Jones Industrial Average advanced 442 points, or 1.1%, and the Nasdaq Composite gained 1.2% in a broad-based rally.

Investors responded positively to the May jobs report, which revealed that nonfarm payrolls increased by 139,000 - above the 126,000 consensus forecast, though slightly down from April’s revised 147,000 figure. Notably, the Department of Labor also revised March and April's job gains downward, painting a slightly softer labor market picture than initially thought. However, the overall tone of the report suggested resilience in employment despite global headwinds and domestic policy uncertainty. Meanwhile, average hourly wages climbed 0.1% on the month, resulting in a 0.4% year-over-year pace. This modest uptick in earnings suggested ongoing wage pressure, which could dissuade the Federal Reserve from considering rate cuts in the immediate term.

The rally gained further steam after President Trump announced an upcoming meeting between senior US and Chinese officials to resume trade negotiations. The announcement sparked optimism that a new round of talks could result in progress toward ending the prolonged trade conflict that has weighed on global markets and disrupted supply chains across multiple sectors.

Tesla shares rebounded sharply on Friday, recouping some of the losses suffered during a bruising Thursday session. CEO Elon Musk indicated a willingness to lower tensions with President Trump following a highly publicized dispute that erased nearly $150 billion from Tesla’s market capitalization within hours. Despite the White House signaling that Trump was not interested in speaking with Musk directly, the Tesla CEO appeared to extend an olive branch by softening his stance regarding the continued use of SpaceX’s Dragon spacecraft in government missions.

The rift between Musk and Trump had intensified over the past week, with the President threatening to pull government contracts from Musk’s companies, particularly SpaceX. Musk, in turn, criticized Trump’s economic policy, especially the so-called “big beautiful” tax cut package that he claimed disproportionately favored corporations without supporting innovation or the middle class. While the public back-and-forth rattled investors, Friday’s rebound in Tesla stock suggested that market participants are hopeful the feud may soon deescalate. Still, with the stock down nearly 25% in 2025 and Tesla battling declining electric vehicle sales, the company remains under significant pressure.

In currency markets, the Japanese Yen held firm following positive revisions to Japan’s first-quarter GDP data. The economy shrank less than previously estimated, contracting by an annualized 0.2% instead of the earlier 0.7%. Moreover, household consumption, a key economic component, registered a slight increase of 0.1%, offering some comfort to policymakers. These updates reinforced expectations that the Bank of Japan may continue to tighten policy, helping the Yen gain ground against the US Dollar. The USD/JPY pair slipped below the 144.50 level during early Monday trading.

The Australian Dollar also bounced back to start the new week, clawing back losses from the previous session. Support for the AUD came in part from the release of China’s Caixin Services PMI, which rose to 51.1 in May, in line with expectations. Given Australia's economic dependency on China, any improvement in Chinese demand tends to support the Aussie dollar. At home, however, Australia’s trade surplus shrank to 5.4 billion AUD in April, well below forecasts. Exports fell 2.4%, while imports rose 1.1%, narrowing the trade buffer. Meanwhile, Australia’s Q1 GDP showed slower growth at 0.2%, undercutting expectations of a 0.4% increase. Annual growth held at 1.3%, but still missed projections of 1.5%.

In North America, the Canadian Dollar inched higher, pushing the USD/CAD pair down to around 1.3680 during Asian trading hours. Friday’s robust US employment report had previously sent the greenback higher, but a Monday pullback in the USD combined with easing tensions over steel and aluminum tariffs helped the loonie stabilize. The prospect of improving US-China relations further supported risk-sensitive currencies like CAD.

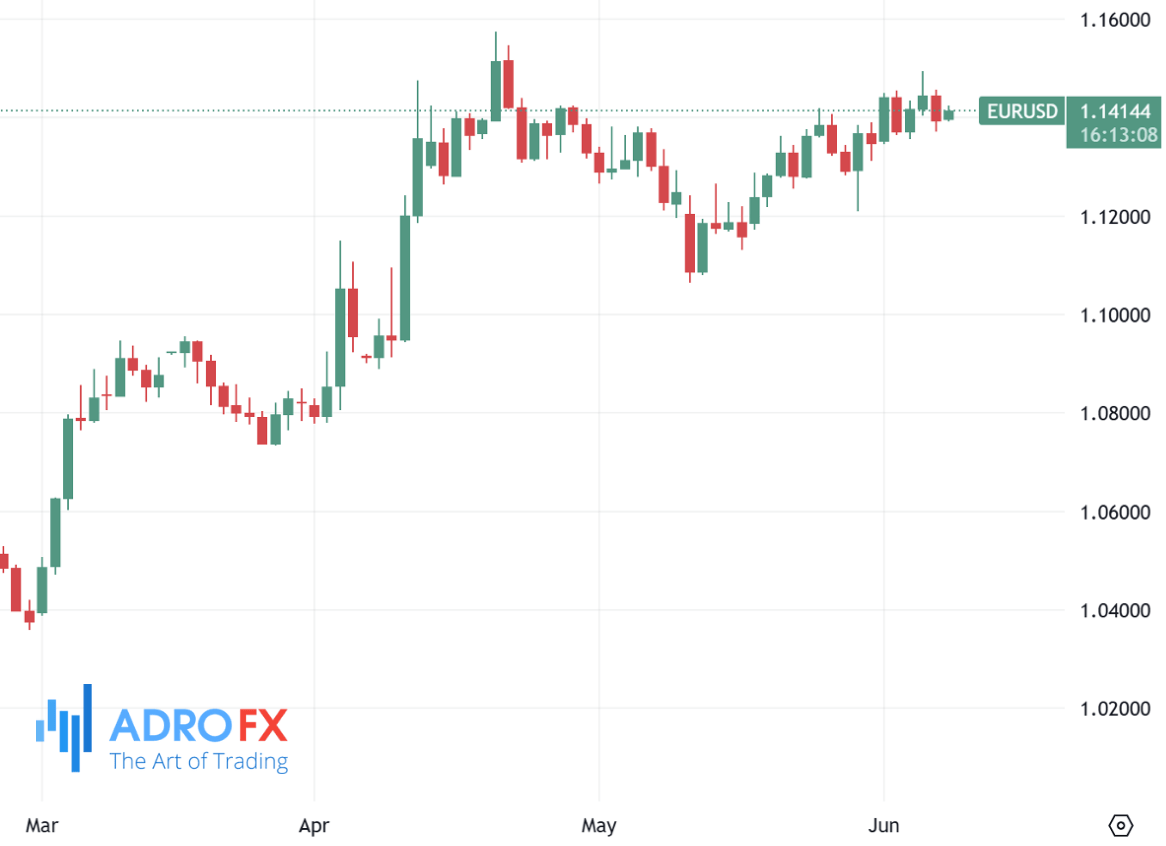

The Euro traded near 1.1400 against the Dollar following earlier losses, with market participants closely watching commentary from European Central Bank officials. ECB policymaker Yannis Stournaras said the eurozone had achieved a "soft landing" and that most of the policy easing was behind them. However, he also warned that the uncertain global trade environment - especially the risk of new US tariffs - posed challenges. ECB President Christine Lagarde echoed that message, saying monetary policy is appropriately positioned for current conditions, though she acknowledged that uncertainty remains elevated.

In the United Kingdom, the British Pound saw a slight uptick against the Dollar during Monday’s Asian session, with GBP/USD trading around the 1.3530 mark. The move comes after a pullback from last week’s high near 1.3615 - the strongest level since early 2022. With no significant UK or US economic data scheduled for release on Monday, Pound movement will likely be driven by overall market sentiment and Dollar dynamics. The lack of conviction in Monday's gains suggests traders are waiting for more definitive signals before committing to a continuation of the Pound’s two-month-long uptrend.

Across global markets, Friday’s rally and Monday’s early trading signal renewed risk appetite as investors weigh a more positive narrative around the US labor market and geopolitical developments. Still, uncertainty remains prevalent, with earnings pressure, central bank policy, and trade negotiations all capable of influencing sentiment in the days ahead.

Attention now turns to the planned US-China trade meeting in London on Monday. US Treasury Secretary Scott Bessent, alongside two other senior officials, will meet with Chinese counterparts in hopes of finding common ground on a range of contentious issues. These discussions come at a critical juncture, with both economies feeling the strain of tariff escalation and strained diplomatic relations.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates