Tech Sector Lifts S&P 500 Amid Earnings Anticipation; Aussie Dollar Gains on Improved Risk Sentiment | Daily Market Analysis

Key events:

- USA - Durable Goods Orders (MoM) (Mar)

- USA - Crude Oil Inventories

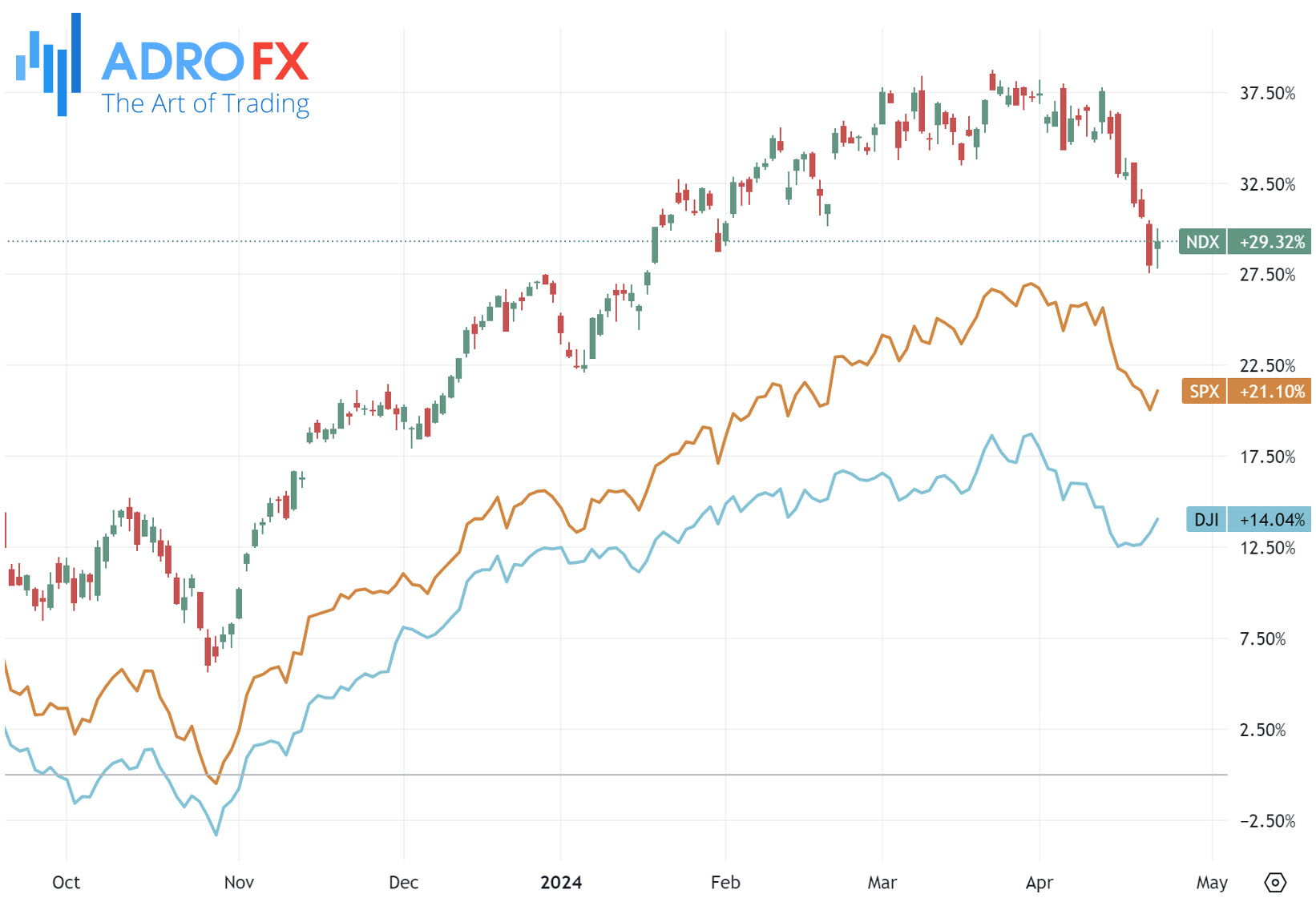

The S&P 500 surged on Monday, driven by strength in the technology sector, marking a rebound from its most significant weekly decline since March of the previous year. Investors turned their attention to upcoming quarterly earnings reports from major tech companies.

The Dow Jones Industrial Average climbed by 292 points, or 0.8%, while the S&P 500 gained 0.9%, and the NASDAQ Composite rose by 1%. Last week, the S&P 500 experienced its sixth consecutive weekly loss, recording its largest decline since March 2023.

The resurgence in the technology sector led the broader market rebound following a recent downturn, with investors eagerly anticipating earnings reports from four of the "Magnificent 7" stocks scheduled for this week.

Tesla is set to report on Tuesday, followed by Meta Platforms, the parent company of Facebook, on Wednesday, and then Microsoft and Alphabet, the parent company of Google, on Thursday.

Before its earnings announcement, Tesla saw a decline of over 3% after announcing price cuts in key markets like China and Germany, following similar reductions in the United States. This move raised concerns about a potential price war in the electric vehicle market.

Meanwhile, the yield on the 2-year Treasury briefly surpassed 5%, continuing recent gains as investors awaited a plethora of key data releases, including manufacturing data, preliminary Q1 economic growth figures, and the Fed's PCE price index data – the central bank's preferred measure of inflation – later in the week.

Expectations for rate cuts have diminished, with only two cuts now anticipated, below the Fed's projection. The Federal Reserve is expected to maintain its current rate at its upcoming meeting on May 1. However, market focus will be on Chairman Jerome Powell's remarks for further insights into the Fed's future rate outlook.

The Australian Dollar maintains its upward trajectory for the second consecutive session on Tuesday, driven by an improved risk appetite in the market. This positive sentiment follows a de-escalation of geopolitical tensions in the Middle East, with an Iranian official indicating last week that there are no immediate plans for retaliation against Israeli airstrikes, as reported by Reuters.

Supporting the Australian Dollar's rise is the release of Australia's Judo Bank PMI data on Tuesday. The Composite PMI surged to a 24-month high of 53.6 in April, marking an improvement from the previous month's 53.3. This suggests a rapid expansion in the Australian private sector during the second quarter, with substantial growth driven by the services sector.

In contrast, the Japanese Yen struggles to capitalize on its modest gains during the Asian session, remaining near a 34-year low against the US Dollar. The Bank of Japan signaled a cautious approach to policy normalization, while the Fed is expected to delay interest rate cuts amid persistent inflation. This divergence in interest rates between the US and Japan, coupled with reduced geopolitical tensions in the Middle East, continues to undermine the safe-haven appeal of the JPY.

Meanwhile, the US Dollar remains close to its highest level since November, supported by hawkish Fed expectations. This dynamic acts as another catalyst for the USD/JPY pair. However, caution prevails among investors ahead of the BoJ decision on Friday and significant US macro data releases later in the week.

The USD/CAD pair extends its decline near 1.3695 despite lower crude oil prices. Strong US economic data and the Fed's hawkish stance may limit the pair's downside. Investors are keenly awaiting the US S&P Global PMI ahead of key economic indicators like US GDP and US Core PCE later in the week.

Several Fed policymakers have expressed a preference for maintaining current borrowing costs, citing slow progress on inflation and the resilience of the US economy. This sentiment may further support the USD. Additionally, the release of Canadian Industrial Produce Prices data aligns with market expectations, while declining WTI prices exert downward pressure on the Canadian Dollar.

Investors are anticipated to closely monitor the US S&P Global PMI for indications of sectoral improvements. Attention will shift to the Australian Monthly Consumer Price Index and quarterly RBA Trimmed Mean CPI data on Wednesday.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates