Dow Jones, S&P 500, and Global Currencies React to Fed’s First Rate Cut Since December | Weekly Market Analysis

Key events this week:

Tuesday, September 23, 2025

- USA - S&P Global Manufacturing PMI (Sep)

- USA - S&P Global Services PMI (Sep)

- USA - Fed Chair Powell Speaks

Wednesday, September 24, 2025

- USA - New Home Sales (Aug)

- USA - Crude Oil Inventories

Thursday, September 25, 2025

- Switzerland - SNB Interest Rate Decision (Q3)

- USA - Durable Goods Orders (MoM) (Aug)

- USA - GDP (QoQ) (Q2)

- USA - Initial Jobless Claims

- USA - Existing Home Sales (Aug)

Friday, September 26, 2025

- USA - Core PCE Price Index (MoM) (Aug)

- USA - Core PCE Price Index (YoY) (Aug)

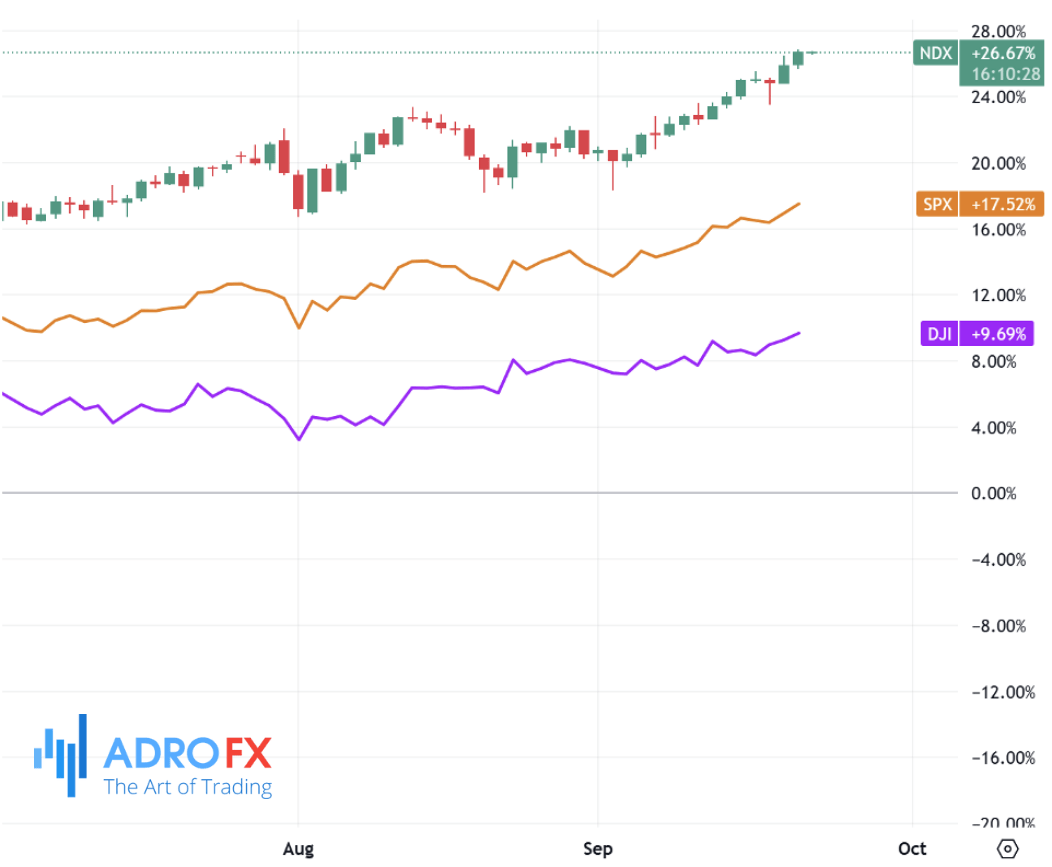

The final trading session of last week brought another milestone for Wall Street as the S&P 500 advanced to a fresh record high. The index climbed steadily on Friday, supported by optimism surrounding Apple’s latest rally and growing hopes that the Federal Reserve’s rate cut cycle will continue after it delivered its first reduction since December. The move reinforced market sentiment that the Fed is shifting toward a looser monetary stance, even though policymakers emphasized a cautious pace in the months ahead.

The Dow Jones Industrial Average also posted a modest but significant increase, closing at a record level, with a gain of 172 points, or 0.4%. That brought the blue-chip index’s weekly advance to nearly 1%, underscoring a strong September performance. Historically, September has been one of the weaker months for equities, yet this year has defied expectations. The Dow is already more than 1.6% higher for the month and is heading toward its fifth consecutive positive monthly close. Meanwhile, the tech-heavy Nasdaq Composite outperformed, rising 0.7%, while the S&P 500 added 0.3% to settle at 6,664.39. Taken together, these gains demonstrate the resilience of US equities even as investors weigh shifting interest rate dynamics and a slowing global economy.

In commodities, gold struggled to build on Friday’s move higher and opened the new week in a narrow trading range just below the $3,700 threshold. The precious metal remains supported by long-term fundamentals but faces immediate pressure from a firmer US dollar. The greenback strengthened last week after rebounding from its lowest level since mid-2022, a move triggered by the Fed’s dovish cut. The dollar’s recovery, combined with upbeat equity sentiment, has capped demand for safe-haven assets. Still, gold continues to trade near record territory, reflecting investors’ appetite for protection against lingering inflation and geopolitical risks.

In the foreign exchange markets, the Japanese yen failed to hold onto its recent gains that followed the Bank of Japan’s more hawkish tone. At the start of the new week, the yen came under renewed pressure as political uncertainty at home and concerns over US tariffs clouded the outlook. Investors are wary that these challenges may slow the BoJ’s path toward policy normalization. Even so, the central bank remains on course to gradually move away from its ultra-loose stance, a notable contrast to the Fed’s dovish direction. This divergence could limit further downside for the yen, although short-term momentum currently favors the dollar.

The Australian dollar extended its losing streak, sliding for a fourth consecutive session against its US counterpart. Traders remain cautious after the Fed signaled it would not rush into deeper rate cuts, keeping the dollar on the front foot. Domestically, Reserve Bank of Australia Governor Michele Bullock acknowledged that the labor market has loosened slightly, with unemployment edging higher, but emphasized that conditions remain near full employment. She added that recent policy easing should help support both household consumption and business investment, though the RBA remains alert to potential risks and ready to act if necessary.

In China, the People’s Bank of China kept its benchmark Loan Prime Rates unchanged, holding the one-year rate at 3.00% and the five-year at 3.50%. The decision to stand pat highlights policymakers’ cautious approach as they attempt to stabilize growth without fueling excess financial risks.

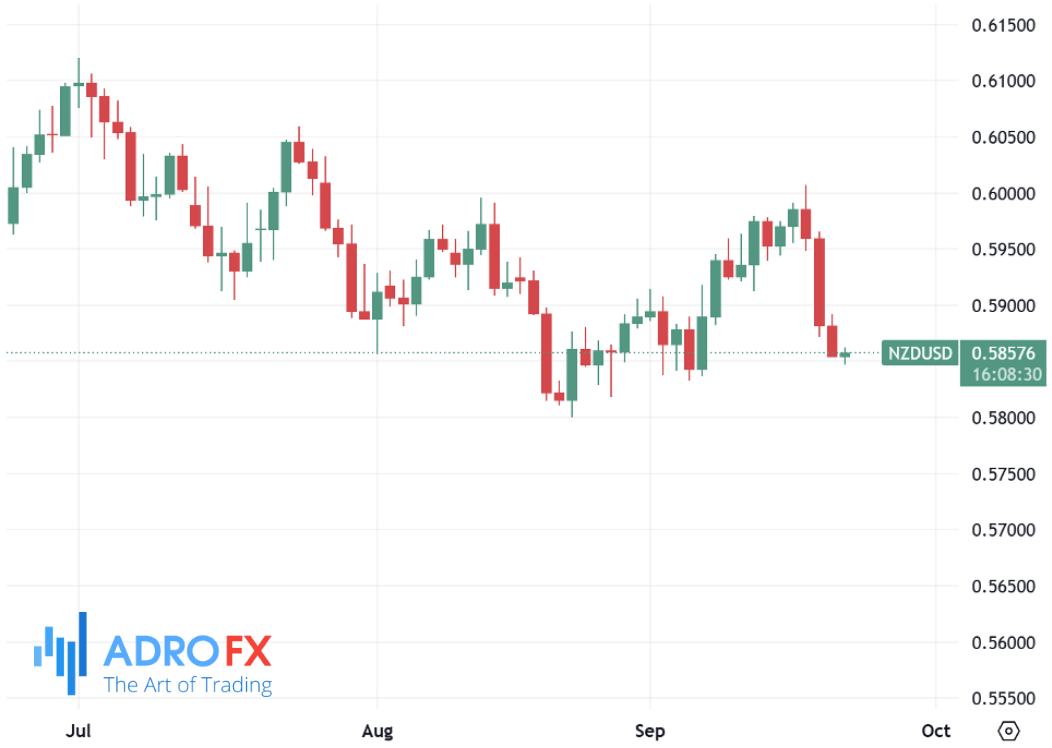

The New Zealand dollar mirrored the Australian dollar’s weakness, declining for a fourth straight session and hovering around 0.5860 in Asian trading hours. The currency has been pressured by dovish expectations for the Reserve Bank of New Zealand, with markets fully pricing in a 25-basis-point rate cut in October. Weak second-quarter economic data, including a sharper-than-expected contraction and a widening trade deficit, have even raised the possibility of a larger 50-basis-point move.

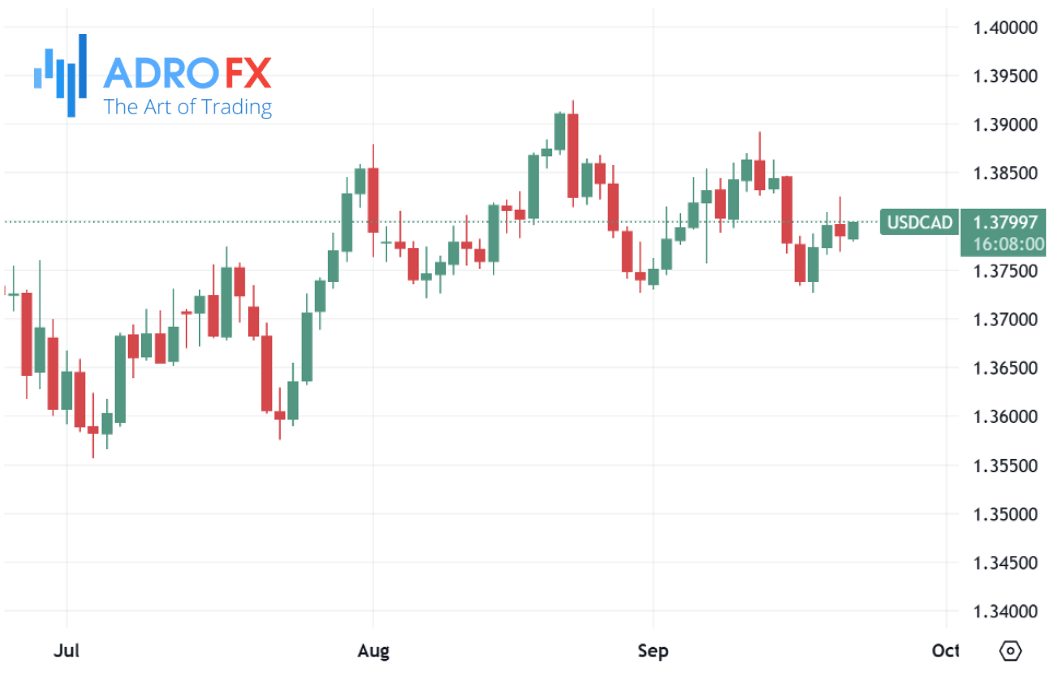

The Canadian dollar, by contrast, showed more resilience, with USD/CAD pulling back to around 1.3800. The loonie found support from stronger-than-expected August retail sales, which advanced 1.0% after July’s 0.8% drop. This positive data eased concerns of an aggressive Bank of Canada easing cycle, particularly as the central bank already delivered a 25-basis-point cut to 2.50% last week. Policymakers cited a softening labor market and moderating inflation pressures as key reasons for easing, though Canada’s decision to withdraw most retaliatory tariffs has also reduced inflationary risks.

Turning to Europe, the euro struggled against the US dollar, with EUR/USD sliding for the fourth straight session and trading near 1.1730. The pair’s weakness reflects dollar strength but also domestic headwinds in Europe. Political unrest in France has weighed on investor confidence, with massive protests urging President Emmanuel Macron and the new prime minister to roll back spending cuts. Meanwhile, European Central Bank officials have signaled that another rate cut may be forthcoming. Governing Council member Mario Centeno stated that inflation risks remain tilted to the downside, making further easing likely if consumer prices stay subdued.

Federal Reserve Chair Jerome Powell addressed reporters after last week’s meeting, explaining that growing signs of labor market weakness drove the decision to cut rates for the first time in nearly a year. Powell stressed that the Fed is not committed to a preset course of rapid cuts but will assess conditions on a meeting-by-meeting basis. The so-called “dot plot” of policymakers’ projections pointed to two more cuts this year, although Powell emphasized flexibility and data dependency.

The absence of major US economic releases on Monday leaves markets focused on upcoming Fed commentary. Several influential Federal Open Market Committee members are scheduled to speak, and their remarks could sway expectations about the timing of the next policy move. Later this week, traders will also pay close attention to the Personal Consumption Expenditures (PCE) Price Index, the Fed’s preferred inflation gauge. The report is expected to confirm subdued price pressures, which may further justify a gradual easing cycle and continue to shape the dollar’s path in global markets.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates