Equities Stay Resilient Amid Weak Consumer Sentiment and Shifting Currency Trends | Weekly Market Analysis

Key events this week:

Tuesday, September 16, 2025

- USA - Core Retail Sales (MoM) (Aug)

- USA - Retail Sales (MoM) (Aug)

Wednesday, September 17, 2025

- UK - CPI (YoY) (Aug)

- Eurorzone - CPI (YoY) (Aug)

- Canada - BoC Interest Rate Decision

- USA - Crude Oil Inventories

- USA - FOMC Economic Projections

- USA - FOMC Statement

- USA - Fed Interest Rate Decision

- USA - FOMC Press Conference

Thursday, September 18, 2025

- UK - BoE Interest Rate Decision (Sep)

- USA - Initial Jobless Claims

- USA - Philadelphia Fed Manufacturing Index (Sep)

Friday, September 19, 2025

- Japan - BoJ Interest Rate Decision

The US stock market ended last week with mixed results as investors balanced optimism with fresh concerns. The S&P 500 managed to extend its two-week winning streak, although Friday’s session saw a modest pullback triggered by climbing Treasury yields and consumer sentiment data that pointed to lingering worries about the health of the economy. The Dow Jones Industrial Average, which had pushed above 46,000 for the first time ever last Thursday, retreated by 273 points the next day, settling lower by about 0.6%. Even with this decline, the Dow remained more than 500 points higher compared to the start of the week, notching a gain of over 1.1% across the five sessions. The S&P 500 dipped just 0.1% on Friday after briefly touching a fresh intraday peak of 6,594.67, while the tech-heavy Nasdaq Composite managed to close the session with a 0.5% increase, underscoring the resilience of growth stocks.

While Wall Street indices looked firm, the consumer backdrop showed renewed strain. The University of Michigan’s Consumer Sentiment Index fell to 55.4 from 58.2 previously, reflecting growing anxieties among lower and middle-income households. Although respondents were slightly more optimistic about durable goods purchases, nearly all other components of the survey weakened. Concerns were highlighted about labor market conditions, inflationary pressures, and overall business stability. A notable 60% of survey participants spontaneously mentioned the negative effect of tariffs under the Trump administration, signaling broad unease about trade policy and its impact on household finances. Many also expressed concerns about falling incomes and reduced purchasing power, raising questions about the strength of consumer spending going into the last quarter of the year.

The currency markets opened the new week with significant movement. The euro faced fresh headwinds, slipping to around 1.1730 against the US dollar as Fitch Ratings downgraded France’s sovereign credit rating from “AA-” to “A+,” the lowest level on record for the country at a major agency. The downgrade followed political upheaval after Prime Minister François Bayrou stepped down following a lost confidence vote over an austerity budget. This political instability has stoked concerns about governance in the eurozone’s second-largest economy, with potential spillover effects on the shared currency. Traders are now weighing whether ongoing turmoil in France could exacerbate weakness in the euro over the near term.

In contrast, the Australian dollar clawed back some ground against the US dollar after suffering losses late last week. The AUD/USD pair gained modestly despite weaker-than-expected Chinese economic data, including a softer 3.4% year-over-year rise in retail sales versus expectations of 3.8%, and industrial production climbing just 5.2% against forecasts of 5.8%.

The National Bureau of Statistics in Beijing acknowledged that August data signaled a generally stable economy, but warned of a “severe external environment” and difficulties for many businesses. Even so, the Australian dollar found support from diminishing expectations of further rate cuts by the Reserve Bank of Australia. Swaps now suggest an 86% probability that the RBA will hold policy steady in September, buoyed by a robust trade surplus, firmer second-quarter GDP, and above-target inflation readings in July. Adding to the hawkish tilt, Australia’s consumer inflation expectations rose in September, signaling stronger domestic demand and renewed concern about overheating price pressures. RBA Governor Michele Bullock pointed to improved private-sector activity as another positive development.

The Japanese yen, often sought as a safe-haven asset, showed mild strength against a soft US dollar during Asian trading hours, though its moves remained constrained within the familiar range of recent weeks. Political developments in Tokyo have injected uncertainty into the outlook. Prime Minister Shigeru Ishiba’s resignation earlier this month cast doubt on the trajectory of government policy and by extension the Bank of Japan’s monetary stance. Market participants now speculate that the BoJ could delay tightening further, given the fragile political backdrop and subdued domestic conditions. This prospect, combined with a generally upbeat global risk tone, limited yen gains as investors rotated into equities.

In North America, the Canadian dollar eased slightly after modest advances in the prior session, with USD/CAD trading near 1.3840. Traders are awaiting Tuesday’s consumer price index data, which will serve as a key precursor to Wednesday’s Bank of Canada policy decision. The likelihood of a rate cut has grown following August labor market data showing a loss of approximately 65,500 jobs and a jump in the unemployment rate to 7.1%. These indicators strengthen the argument that the central bank may need to ease monetary conditions to support the labor market and broader economy.

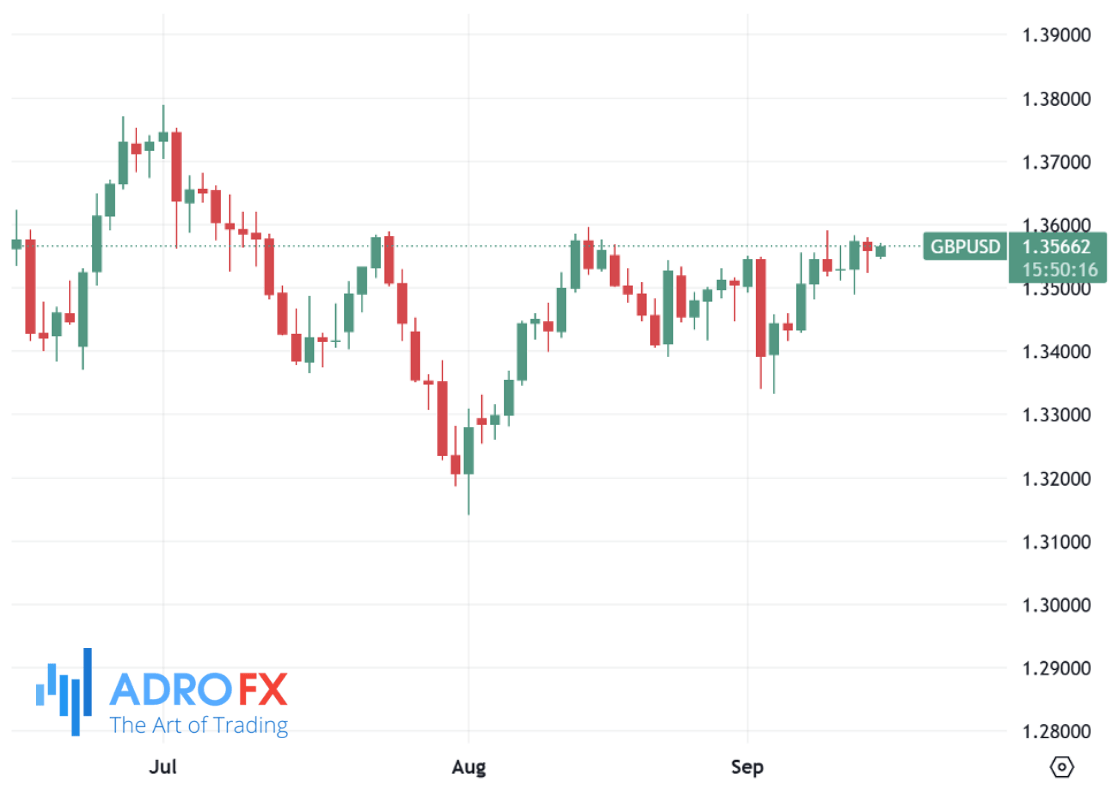

The British pound showed slight resilience, with GBP/USD edging toward 1.3555 in the early Asian session. Still, underlying sentiment toward the currency remains fragile. Weak economic releases in July, including disappointing GDP growth and factory output figures, added to worries about the UK’s trajectory. Markets now price in roughly a one-third probability of another rate cut from the Bank of England before year’s end, reflecting expectations that policymakers may need to act to prevent a deeper downturn. Traders are cautious, balancing short-term gains against the broader risks surrounding Britain’s economic outlook.

Meanwhile, the gold market opened the week on uneven footing. Spot gold dipped in early Asian hours toward $3,627 per ounce but recovered quickly, trading back near the top of its one-week range. Market participants appeared reluctant to take large directional bets ahead of the highly anticipated Federal Open Market Committee decision later this week, which is expected to set the tone for dollar dynamics and safe-haven flows. Growing speculation that the Federal Reserve could adopt a more aggressive easing stance has already weighed heavily on the greenback, keeping it near its lowest level since late July. This has, in turn, provided a strong tailwind for the non-yielding metal. On top of monetary policy expectations, geopolitical risks have also underpinned gold demand. However, the prevailing risk-on mood in equity markets prevented bullion from retesting its recent record peak above $3,675. Even so, the fundamental landscape appears supportive of further upside, with any corrective dips likely to be viewed as buying opportunities by investors seeking a hedge.

Taken together, the picture across global markets remains one of cautious optimism, where strong equity momentum coexists with persistent economic and political risks. Investors are closely monitoring central bank decisions in the US, Canada, and Australia, alongside evolving conditions in Europe and Asia. With consumer sentiment softening in the United States, political instability weighing on the euro, and ongoing questions about global growth, volatility may remain elevated. Yet the resilience of equity markets, the appeal of gold as a hedge, and shifting expectations for monetary policy continue to define the trading landscape.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates