US Stocks Show Resilience Despite Weaker Data; Attention Shifts to August Job Report | Daily Market Analysis

Key events:

- China - Manufacturing PMI (Aug)

- Eurozone - CPI (YoY) (Aug)

- USA - Core PCE Price Index (YoY) (Jul)

- USA - Core PCE Price Index (MoM) (Jul)

- USA - Initial Jobless Claims

On Wednesday, US stocks displayed resilience despite encountering weaker-than-expected economic data, with investor focus shifting towards the upcoming August job report set to be released on Friday.

The S&P 500 index reached its highest point in almost three weeks, propelled by an ADP National Employment report. This report revealed that private payrolls grew by 177,000 jobs in August, falling short of estimates of 195,000 and indicating a potential softening in the labor market. Simultaneously, the Nasdaq secured its strongest closing since August 1st.

Signs of a labor market slowdown persisted as the data demonstrated that the economy generated fewer jobs than anticipated in August. ADP's report indicated the creation of around 177,000 new private-sector jobs, a considerable decline from the 371,000 increase observed in July. This easing in job growth tempered concerns that a tight labor market could drive up wages and inflation.

Nela Richardson, Chief Economist at ADP, noted that after enjoying exceptional gains driven by the recovery over the past two years, the economy is transitioning towards more sustainable growth in employment and wages as the pandemic's economic impacts diminish.

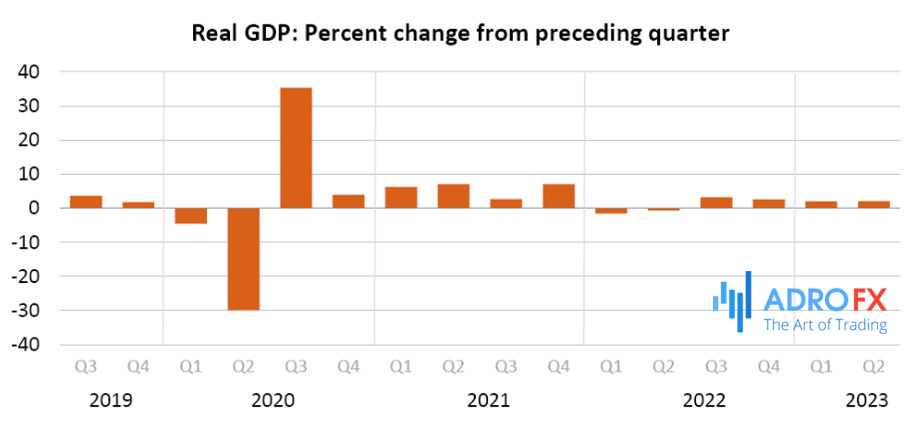

Alongside indications of a weakening labor market, the most recent evaluation of second-quarter economic growth was revised downward to 2.1% from the initial 2.4% reading. The updated gross domestic product figures revealed that the US economy expanded by 2.1% in Q2, marking a slower pace compared to the preliminary estimate of 2.4% growth.

Tech giant Apple Inc (NASDAQ: AAPL) spearheaded the tech sector's upward movement with an almost 2% surge. This rally followed Citigroup's reaffirmation of its buy rating on the stock, driven by optimism surrounding the upcoming launch of the iPhone 15 on September 12th. Citigroup's analysis suggested that Apple might raise prices for the iPhone 15 by $100 to $200, predicting that the release could prompt a wave of consumer upgrades among iPhone 12 users.

On the other hand, HP Inc (NYSE: HPQ) encountered a setback, experiencing a nearly 7% decline. The company revised its annual profit and free cash flow guidance downward and reported second-quarter sales that fell below estimates. This performance was attributed to a slower-than-expected recovery in PC demand in China.

Gold prices maintained their position near three-week highs on Thursday, propelled by underwhelming economic data from the US. These lackluster readings intensified speculation that the Federal Reserve's capacity to raise interest rates further might be limited.

Throughout the week, the precious metal recorded robust gains, benefitting from subdued US GDP and employment figures, which consequently exerted downward pressure on both the dollar and Treasury yields. Additionally, gold experienced heightened demand as a safe-haven asset amid escalating concerns about a potential economic slowdown in China. As data depicting China's economic weakness continued to emerge, the attractiveness of gold as a safe-haven investment surged.

The dollar's performance registered a decline of almost 1% over the week, and Treasury yields retreated from their recent peaks. These shifts were prompted by uninspiring economic indicators, fostering expectations of a more dovish stance from the Federal Reserve.

Currently, market attention is firmly fixed on the impending release of personal consumption expenditures data, a metric preferred by the Fed to gauge inflation. This data release is expected to provide further insights into the central bank's monetary policy direction.

Looking ahead, the upcoming nonfarm payrolls data for August, scheduled for release on Friday, is anticipated to reveal a further cooling in the job market. This scenario would diminish the Fed's motivation to continue raising interest rates.

However, historical trends have demonstrated that gold's response to nonfarm payrolls tends to be modest, particularly this year, given the consistently positive surprises in the figures.

Nevertheless, despite the US economy showing signs of cooling, the future of gold remains uncertain due to the prospect of enduring higher US interest rates. This uncertainty is compounded by the persistent stickiness of inflation in recent months.

The prevailing trend of rising rates elevates the opportunity cost associated with investing in non-yielding assets such as gold. This trend has contributed to the challenges gold faced throughout the past year.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates