Market Retreats as US Stocks Decline, Investors Await Powell's Testimony | Daily Market Analysis

Key events:

- UK - CPI (YoY) (May)

- USA - Fed Chair Powell Testifies

On Tuesday, US stocks experienced a decline, closing with negative results as investors took the opportunity to secure profits after a sustained rally. The market displayed signs of weakening global demand, prompting cautious behavior at the start of the holiday-shortened week.

Investors are closely watching Federal Reserve Chairman Jerome Powell's congressional testimony scheduled for Wednesday, as it has the potential to impact market dynamics and serve as a significant market mover.

All three major US equity indices concluded the session in negative territory, although they recovered slightly from the session lows. Notably, oil super-majors Exxon Mobil Corp and Chevron Corp weighed on the S&P 500 and the Dow, contributing to the overall decline.

The broad sell-off occurred following the Nasdaq's longest weekly winning streak since March 2019 and the S&P 500's longest winning streak since November 2021.

Despite the setback on Tuesday, the benchmark S&P 500 has still achieved a notable 14.3% gain year-to-date, showcasing overall positive performance thus far in the year.

The upcoming congressional testimony provides Federal Reserve Chair Jerome Powell with an opportunity to offer further guidance on monetary policy, building on the discussions from the recent Fed meeting. However, considering the relatively short time frame between these two events, it is unlikely that Powell will provide significant new insights. The Federal Reserve adopts a data-dependent approach, making decisions on a meeting-by-meeting basis. Therefore, their next decision, scheduled for July 26, will likely depend on various factors, including the forthcoming CPI release on July 12 and the employment report on July 7.

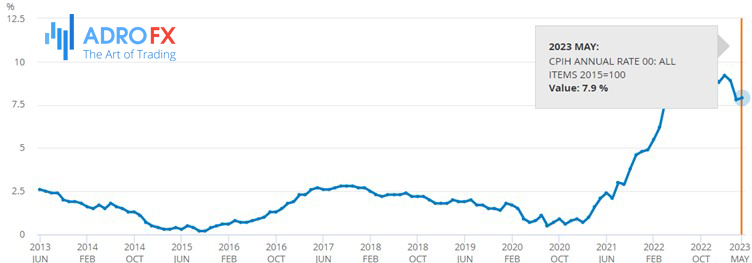

The GBP/USD currency pair experienced a significant surge of 60 pips, pushing it above the 1.2800 level, but later retreated to 1.2760. This movement occurred as market participants reevaluated the UK inflation data in anticipation of the London open on Wednesday.

The May Consumer Price Index (CPI) in the UK surpassed market expectations of 8.4%, reaching a year-on-year figure of 8.7%. However, the Core CPI, which excludes the impact of volatile food and energy prices, aligned with analysts' predictions, indicating a stagnant inflation increase of 6.8% year-on-year.

Nevertheless, the GBP/USD buyers face difficulties as the US Dollar continues its upward grind for the fourth consecutive day, despite recent inaction. This challenges the bullish stance on the GBP/USD pair, even with the favorable UK inflation data supporting the Bank of England (BoE) hawks.

Meanwhile, the US Dollar Index (DXY) remains defensive around 102.60, maintaining its four-day uptrend without showing significant inclination to advance further. The recent strength of the US Dollar can be attributed to hawkish comments made by Federal Reserve policymakers, particularly the nominees, as well as robust US housing data. Furthermore, concerns over geopolitical tensions between the US and China weigh on market sentiment, providing support for the safe-haven appeal of the US Dollar.

Apart from that, the Australian dollar underwent significant fluctuations overnight, resulting in a decline in the AUD/USD exchange rate, approaching the 0.6800 level. The sell-off of the Australian dollar occurred following the release of the minutes from the Reserve Bank of Australia's (RBA) previous policy meeting held on June 6th. Surprising market participants, the RBA decided to implement another 25 basis points hike, bringing the policy rate to 4.10%. This updated guidance regarding the likelihood of further rate hikes aimed to achieve the inflation target.

However, the recently published meeting minutes have raised uncertainties regarding the RBA's future stance on rate increases. It was revealed that the RBA deliberated on the possibility of pausing rates at the last policy meeting but ultimately determined that the arguments were "finely balanced" in favor of implementing a rate hike.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates