Markets Struggle for Direction as Inflation, Trade, and Jobs Data Take Center Stage | Daily Market Analysis

Key events this week:

Tuesday, March 11, 2025

- Japan - GDP (QoQ) (Q4)

- USA - JOLTS Job Openings (Jan)

Wednesday, March 12, 2025

- USA - Core CPI (MoM) (Feb)

- USA - CPI (YoY) (Feb)

- USA - CPI (MoM) (Feb)

- USA - Crude Oil Inventories

- Canada - BoC Interest Rate Decision

- USA - 10-Year Note Auction

Thursday, March 13, 2025

- USA - Initial Jobless Claims

- USA - PPI (MoM) (Feb)

- USA - 30-Year Bond Auction

Friday, March 14, 2025

- UK - GDP (MoM) (Jan)

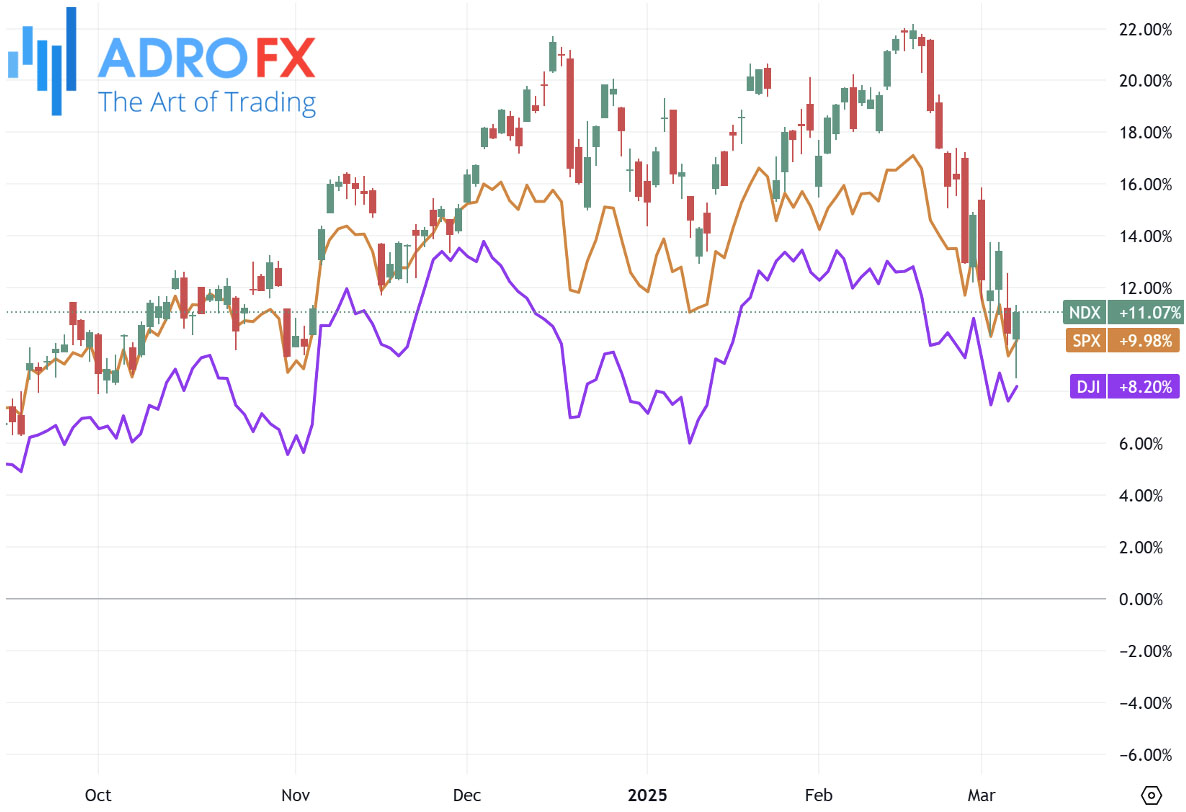

The S&P 500 rebounded on Friday, reversing earlier losses, but despite the recovery, the index still closed the week in negative territory. Investors grappled with mixed signals from the labor market and heightened trade uncertainty, leading to another volatile week on Wall Street.

By the end of the trading session, the S&P 500 advanced by 0.5%, while the NASDAQ Composite gained 0.7%. The Dow Jones Industrial Average climbed by 222 points, marking a 0.5% increase. Even with these gains, the broader market indices remained on track for weekly declines, largely due to concerns over trade policy instability and its potential effects on consumer spending and business investment.

Market jitters intensified following reports that the US was considering imposing reciprocal tariffs on Canada as early as Friday. This development came much sooner than the previously announced deadline of April 2, adding to the uncertainty surrounding the economic impact of recent trade measures. Earlier in the week, President Trump granted a temporary exemption for Canadian and Mexican imports under the United States-Mexico-Canada Agreement, delaying a planned 25% tariff increase until April 2. In response, Canada postponed its second wave of retaliatory tariffs, originally set to target $125 billion worth of US goods, until the same date.

Compounding the uncertainty, reports emerged that the White House is exploring a potential relaxation of energy sanctions on Russia. This initiative aims to encourage Moscow to agree to a ceasefire in Ukraine, though it remains unclear whether such measures will materialize or impact global energy markets in a meaningful way.

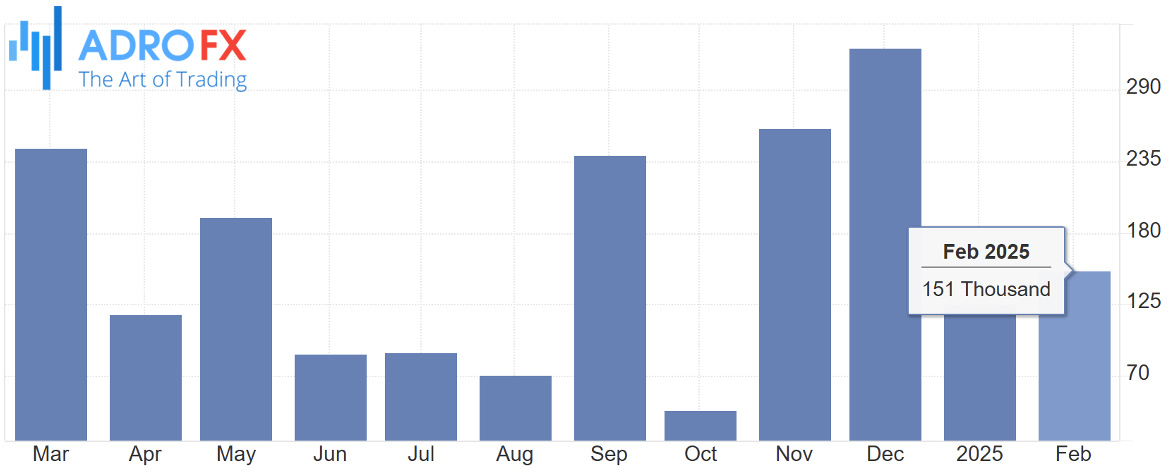

The US labor market report released on Friday signaled a slowdown in job growth, reinforcing expectations of further monetary easing by the Federal Reserve. Nonfarm payrolls data showed that the US economy added 151,000 jobs in February, falling short of the 160,000 forecast. Additionally, January’s payroll figures were revised downward to 125,000 from the initially reported 143,000. The unemployment rate unexpectedly edged higher to 4.1% from 4.0% in January, overshadowing a modest increase in average hourly earnings, which rose to 4% from a revised 3.9% in the previous month. This data reinforced market expectations that the Federal Reserve will maintain a dovish stance and consider multiple rate cuts throughout the year.

Meanwhile, in currency markets, the Australian Dollar rebounded on Monday, recovering from losses sustained in the previous two sessions against the US Dollar. The rally was fueled by growing concerns about a potential economic slowdown in the US, which weighed on the greenback. However, broader market sentiment remained cautious as escalating global trade tensions dampened investor risk appetite. China implemented retaliatory tariffs on US agricultural products in response to last week's US decision to raise tariffs on Chinese imports from 10% to 20%. Given China’s crucial role as Australia’s largest trading partner, such trade disputes have the potential to influence the Australian economy significantly.

Despite global uncertainty, the Aussie found support from strong domestic economic data. Last week’s GDP growth and trade figures exceeded expectations, boosting investor confidence. Additionally, the Reserve Bank of Australia’s latest meeting minutes suggested a cautious approach to further interest rate cuts. The central bank clarified that its February rate reduction should not be interpreted as a commitment to ongoing monetary easing.

On the global trade front, tensions escalated further over the weekend as China announced fresh tariffs on Canadian agricultural products. The Chinese government revealed plans to impose a 100% tariff on Canadian rapeseed oil, oil cakes, and peas, along with a 25% tariff on aquatic products and pork. These measures were introduced in retaliation for tariffs imposed by Canada last October, adding another layer to the ongoing trade conflicts sparked by US policies. The new tariffs are set to take effect on March 20, further complicating the geopolitical trade landscape.

Apart from that, the Japanese Yen remained strong against the US Dollar through Monday’s Asian session. The USD/JPY pair hovered just above its lowest level since October, a decline triggered by Friday’s disappointing US jobs report. Fresh economic data from Japan showed base pay in the country surged to a 32-year high in January, while real cash earnings fell by 1.8% due to persistent inflation. These developments reinforced the belief that last year’s substantial wage hikes would continue into 2024, increasing speculation that the Bank of Japan may pursue further interest rate hikes.

Market sentiment surrounding the BoJ’s policy stance has fueled higher Japanese government bond yields. The narrowing rate differential between Japan and other major economies has driven investors toward the Yen, traditionally considered a safe-haven asset. Additionally, persistent concerns about the economic fallout from US trade policies have strengthened demand for the Yen as global trade risks remain elevated. The growing expectation that the Federal Reserve will implement multiple rate cuts this year has also kept the US Dollar near multi-month lows, further weighing on the USD/JPY pair.

Elsewhere, the USD/CHF pair continued its downward trend for the third consecutive day, trading near 0.8790 during Monday’s Asian session. The greenback remained under pressure amid increasing fears of a US economic slowdown. However, downside momentum for the pair may be limited due to rising US Treasury yields. The Swiss Franc benefited from renewed safe-haven demand as trade tensions between the US and China escalated. In response to the latest US tariff hikes, China implemented new duties of 10% to 15% on select US agricultural goods, effective Monday.

Adding to trade concerns, China imposed a 100% tariff on Canadian agricultural products over the weekend, further intensifying the global trade dispute. Meanwhile, Bloomberg reported that US Commerce Secretary Howard Lutnick confirmed late Sunday that the planned 25% tariffs on steel and aluminum imports would take effect on Wednesday, with no delays expected.

Economic data from Switzerland also influenced market sentiment. The country's inflation rate eased to 0.3% in February, marking its lowest level since April 2021 and down from 0.4% in January. Additionally, the Swiss economy grew by just 0.2% in the fourth quarter of 2024, slowing from 0.4% in the previous quarter. This weaker economic performance has fueled speculation that the Swiss National Bank (SNB) could cut interest rates as early as March, with another potential reduction in June.

The USD/CAD pair remained steady after gaining in the previous session, hovering around 1.4360 during Asian trading hours on Monday. The Canadian Dollar faced pressure due to ongoing trade uncertainties. Adding to market speculation, reports suggested that Canadian Prime Minister Mark Carney might call an early election as soon as Monday. While Canada’s federal election is officially scheduled for October 2025, political analysts believe an early election could take place by late April or early May, introducing another layer of uncertainty to the markets.

This week’s economic calendar is packed with key events that could significantly influence market sentiment and trading dynamics. Investors will closely monitor Japan’s Q4 GDP data on Tuesday for insights into the country’s economic performance, while US JOLTS job openings will provide an update on labor market conditions. The spotlight shifts to Wednesday, with the release of US inflation data, including Core CPI and CPI figures, which will be crucial in shaping expectations for the Federal Reserve’s next policy moves. Additionally, the Bank of Canada’s interest rate decision could impact the Canadian Dollar, while the US crude oil inventories report may drive volatility in the energy market.

Thursday’s focus will be on US jobless claims and the Producer Price Index (PPI) for February, offering further clarity on inflationary pressures and labor market trends. The week wraps up on Friday with the UK’s monthly GDP report, which could influence expectations for the Bank of England’s monetary policy path. Given these high-impact events, traders should brace for potential market fluctuations and adjust their strategies accordingly.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates