Wall Street Ends Volatile Day with Losses Amid Healthcare Struggles and Interest Rate Concerns | Daily Market Analysis

Key events:

- Eurozone - CPI (YoY) (Jul)

After a day of volatile trading, the primary indices on Wall Street concluded with losses due to setbacks in the healthcare sector overshadowing gains made by Cisco and energy stocks. The backdrop of encouraging economic data further heightened apprehensions about the prolongation of elevated interest rates.

The S&P 500 was notably burdened by a sharp 8% decline in CVS Health (NYSE: CVS) following reports of Blue Shield of California's intent to diminish its reliance on CVS as its pharmacy benefit manager (PBM).

Instead, Blue Shield plans to collaborate with other entities, including Amazon.com (NASDAQ: AMZN). This development also impacted the shares of prominent health insurers UnitedHealth (NYSE: UNH) and Cigna (NYSE: CI), both of which possess PBM divisions. Their stocks registered declines of 1.9% and 6.4% respectively, consequently exerting downward pressure on the broader S&P 500 healthcare index, which experienced a 0.8% decrease.

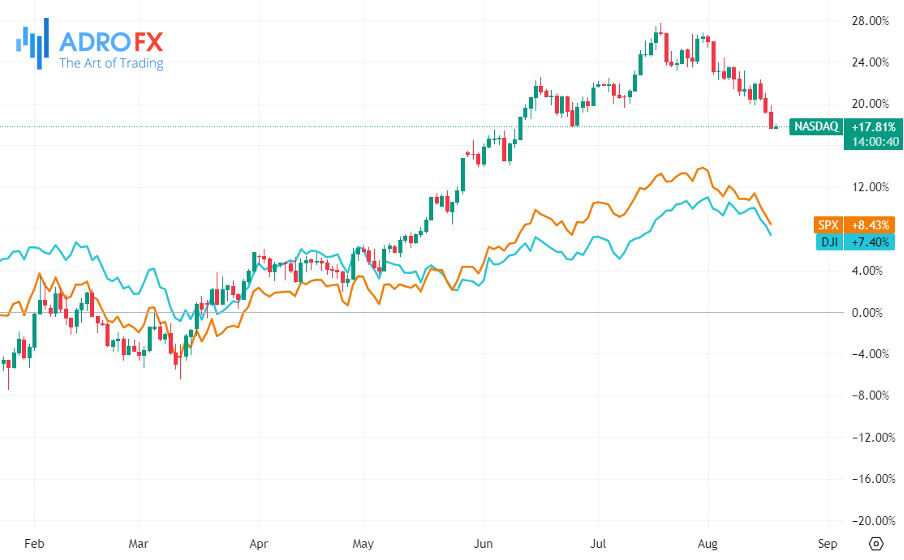

The day's performance translated into a loss of 33.97 points, equivalent to 0.77%, for the S&P 500, which closed at 4,370.36. Simultaneously, the Nasdaq Composite suffered a dip of 143.75 points, signifying a decline of 1.07%, as it concluded at 13,330.88.

The S&P 500's recent trajectory indicates a decline of 2.7% across the last three sessions, marking its most substantial three-session decrease since mid-March. Likewise, the Nasdaq's three-day drop of 3.4% is the most pronounced experienced since February.

The Dow Jones Industrial Average also found itself on the losing end, recording a decrease of 290.91 points, corresponding to a 0.84% decline, with the index settling at 34,474.83.

The energy sector received a boost from escalating oil prices, propelling the shares of Exxon Mobil (NYSE: XOM) and Chevron (NYSE: CVX) upwards by 1.9% and 1.7% respectively. This positive movement was partly attributed to optimism stemming from China's central bank's purported efforts to fortify the property market and the broader economy, thereby aiding commodities.

Adding to the headwinds facing equities, the yield on the 10-year US Treasury notes reached its highest point since October. This escalation was driven by a succession of robust economic indicators throughout the week, instigating concerns that the Federal Reserve might prolong the current level of interest rates.

Mitigating the extent of declines, Cisco Systems (NASDAQ: CSCO) achieved a 3.3% increase in its stock value. This rise followed the release of the networking equipment manufacturer's fourth-quarter results, which surpassed expectations. Moreover, the company's CEO highlighted the potential presented by opportunities in artificial intelligence.

Meanwhile, Pfizer (NYSE: PFE) observed a rise of 2.9% in its shares. This upswing was prompted by the company's announcement regarding its updated COVID-19 vaccine. Pfizer's updated vaccine is presently undergoing testing against emerging variants of the virus. In a study conducted on mice, the vaccine displayed neutralizing activity against the "Eris" subvariant.

Gold prices experienced a modest increase on Friday, rebounding from a five-month low. This recovery was prompted by a decline in the dollar due to profit-taking. However, persistent concerns about the potential escalation of US interest rates continued to exert downward pressure on precious metal markets.

During Asian trading, the dollar registered a 0.3% decrease as a result of profit-taking, following a period during which the greenback surged to its highest levels in over two months against a basket of currencies.

Over the course of the week, the dollar was poised to achieve a 0.5% rise, propelled by robust economic indicators from the United States and hawkish signals derived from the minutes of the Federal Reserve's July meeting. These factors heightened expectations that US interest rates would remain elevated for an extended duration.

Despite the Fed signaling just one more rate hike within the current year, the prospect of sustained higher US rates works against the favor of gold markets. This is because it amplifies the opportunity cost associated with holding non-yielding assets. This trend negatively impacted gold throughout 2022, and its influence has thus far limited significant gains in the precious metal during this year.

Looking ahead, the anticipation of forthcoming monetary policy announcements and economic insights to emerge from the Jackson Hole Symposium next week maintained a tilt toward the dollar in terms of investor positioning, simultaneously engendering caution within metal markets.

Additionally, gold encountered pressure due to a notable increase in US Treasury yields, with the 10-year rate surging to levels that mirror those observed during the 2008 financial crisis.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates