S&P 500 Stumbles, US Dollar Index Seeks Recovery Amid Risk Aversion and Economic Indicators | Daily Market Analysis

Key events:

- USA - ADP Nonfarm Employment Change (Jul)

- USA - Crude Oil Inventories

Tuesday witnessed a stumble in the S&P 500, with consumer stocks bearing the brunt of the pressure, as investors absorbed the latest round of quarterly earnings reports.

The S&P 500 declined by 0.3%, while the Dow Jones Industrial Average managed to edge up by 0.2%, or 71 points. In contrast, the Nasdaq experienced a 0.4% decline.

The US Dollar Index (DXY) is seeing renewed buying interest, attempting to recover from its first daily loss in three sessions, and currently trading at its highest level since early July. The recent surge in risk aversion has contributed to the market's concerns, compounded by fears stemming from the downgrade of the US government credit rating by global rating agency Fitch Ratings. The downgrade, which lowered the rating from AAA to AA+, was driven by anxieties surrounding the ongoing debt crisis.

Investor sentiment is further influenced by anticipation ahead of the release of the US Automatic Data Processing (ADP) Employment Change report, which serves as an early indicator for the highly significant Nonfarm Payrolls (NFP) data to be released on Friday. These factors have come together to bolster the US Dollar against six major currencies, as market participants seek safe-haven assets.

In response to the credit rating downgrade, the White House and US Treasury Secretary Janet Yellen have swiftly criticized the move and defended the US Dollar. Despite their efforts, the Greenback has faced some challenges in maintaining its strength amid the prevailing uncertainties.

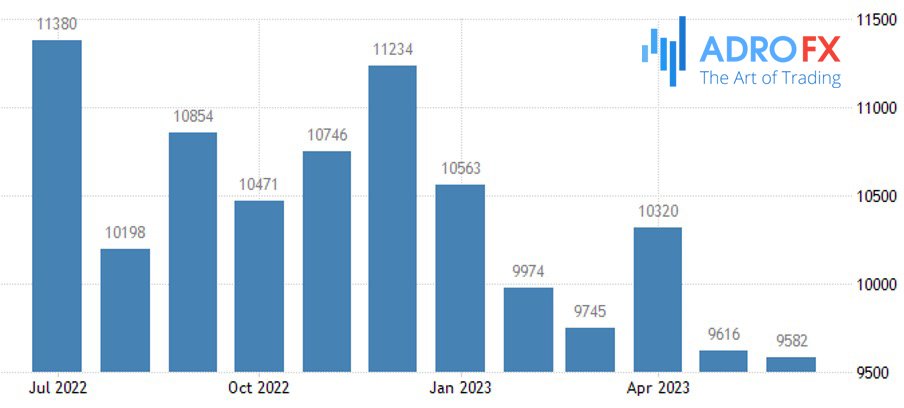

On the economic front, the labor market showed signs of easing, with the number of job openings in June dropping more than anticipated to 9.58 million, compared to 9.61 million openings in May.

The indication of weaker labor demand is likely to be positively received by the Federal Reserve, reinforcing the belief that resuming rate hikes is unlikely in the near future.

The latest data releases in the eurozone on Monday revealed contrasting trends in growth and inflation. The euro area experienced slightly higher-than-expected growth, with a year-on-year increase of 0.6% (quarter-on-quarter growth of 0.3%) in the second quarter. On the other hand, inflation slowed to 5.3% in July, in line with consensus forecasts, with core inflation remaining unchanged at 5.5%.

Of particular interest to the European Central Bank (ECB) is the inflation dynamics, specifically the pressure from service prices. While goods inflation has been easing, service price pressure has been on the rise, fueled by wage growth and increased demand.

Looking ahead, the ECB's attention will likely be focused on these inflationary trends. However, August is expected to be a quiet month for ECB speakers, with only remarks from dove Fabio Panetta later in the week. Consequently, EUR/USD's movements will likely be primarily driven by the dollar's performance and upcoming US data releases for the rest of the week. There may be some downside risks for the EUR/USD pair, potentially affecting the 1.0900 handle. As the market continues to assess economic developments and central bank actions, investors will closely monitor these factors for potential impacts on the currency pair.

As widely anticipated, the Reserve Bank of Australia (RBA) maintained its interest rates unchanged in its recent meeting, defying consensus expectations for a rate hike. The central bank emphasized the effectiveness of the current higher interest rates in achieving a more balanced relationship between supply and demand in the economy. As a result, the RBA chose to take a pause in its tightening cycle to assess incoming economic data more comprehensively.

The RBA's new Consumer Price Index (CPI) forecasts indicate a decline in inflation to 3.25% by the fourth quarter of the next year, with a subsequent return to the target range by the end of 2025. This could be interpreted as a dovish signal, suggesting that the current pace of tightening is appropriate to bring inflation back to target within a reasonable time frame.

Nevertheless, the RBA has demonstrated a heightened sensitivity to economic data, and it is likely to continue closely monitoring incoming information. A scenario where inflation readings remain elevated might prompt the RBA to implement another rate hike before reaching its tightening peak.

The prevailing outlook remains for one final 25 basis point increase in interest rates, which is expected to be delivered in September. Notably, the potential for an inflation surprise driven by electricity tariffs could be a key factor in influencing the RBA's decision at that time.

As a result of the current RBA stance, the Australian Dollar (AUD) may exhibit weaker performance compared to other currencies such as the New Zealand Dollar (NZD) and the Scandinavian currencies (Scandies) until a more bullish outlook emerges in September, contingent on the RBA's decision to proceed with the final rate hike. Investors will closely monitor economic developments and central bank actions to gauge the future direction of the AUD against its peers.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates