S&P 500 Slides as Nvidia and Global Economic Risks Weigh Heavy | Daily Market Analysis

Key events:

- Australia - RBA Interest Rate Decision (Dec)

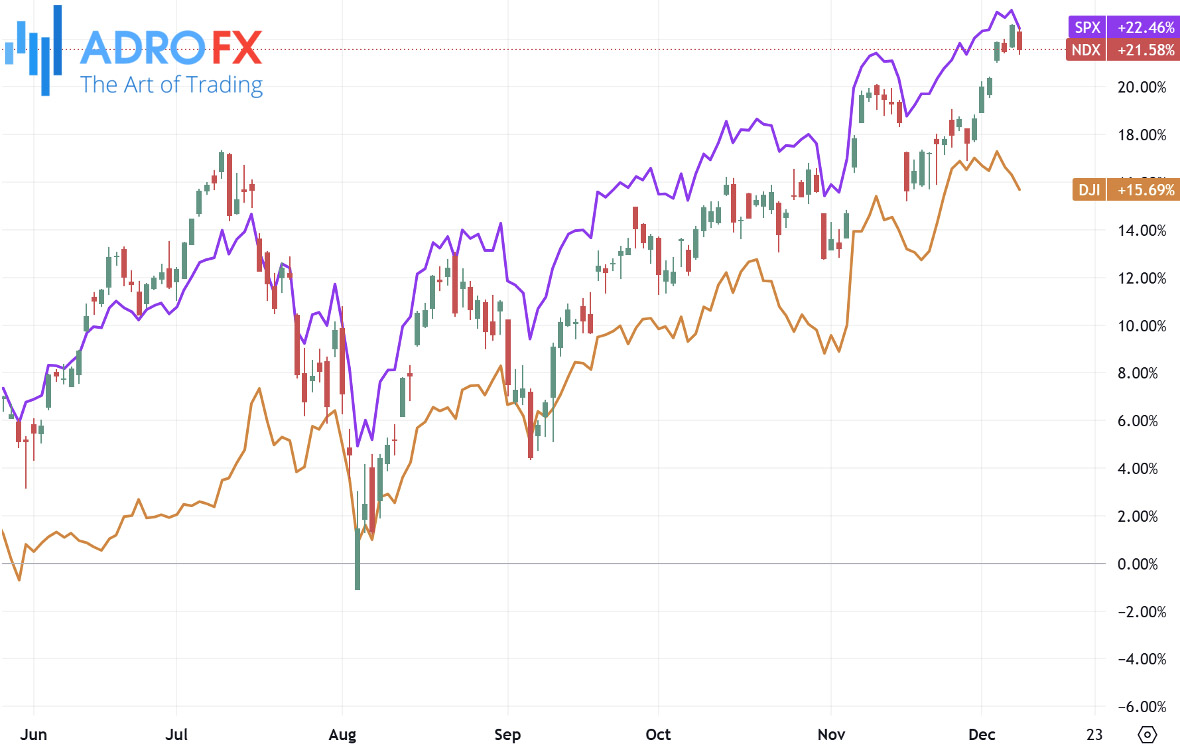

The S&P 500 experienced a downturn on Monday as technology stocks, led by Nvidia, came under pressure just ahead of significant inflation data set for release this week.

The Dow Jones Industrial Average fell by 240 points, or 0.5%, while the S&P 500 dropped 0.6%, and the Nasdaq Composite also declined by 0.6%.

Nvidia’s stock took a notable hit, sliding 2.6% after China initiated an investigation into the company over alleged breaches of anti-monopoly laws. This action is widely seen as a response to Washington’s recent restrictions on chip exports, adding tension to an already complex global semiconductor landscape.

Meanwhile, in the Asian trading session, the Japanese Yen struggled to maintain gains against the US Dollar after a slight bounce from a one-week low.

Speculation surrounding the Bank of Japan’s next moves added to the uncertainty. While BoJ Governor Kazuo Ueda hinted at a possible rate hike in December, reports suggested the central bank might hold off on any policy changes. Additionally, dovish comments from BoJ board member Toyoaki Nakamura, emphasizing the need for caution in tightening monetary policy, undermined confidence in the Yen. This hesitation allowed the USD/JPY pair to remain range-bound despite the fluctuating expectations.

The USD/CAD pair reached levels not seen since April 2020 during Tuesday’s session, although it failed to sustain momentum above the 1.4200 mark. A combination of factors favored bullish sentiment for the pair. The Canadian Dollar remained under pressure due to mounting expectations of a significant interest rate cut from the Bank of Canada. The rise in Canada’s unemployment rate for November added weight to these predictions. Additionally, a modest decline in crude oil prices further weakened the commodity-linked Canadian Dollar, providing additional support for the USD. However, the lack of follow-through buying of the USD kept gains in check.

Sterling continued to trade steadily around 1.2750 for the second consecutive day, with the GBP/USD pair showing limited movement during the Asian session. The pair’s stability comes amid cautious optimism ahead of the release of US Consumer Price Index (CPI) data, a key indicator that could shape Federal Reserve policy decisions. Despite the lack of significant activity, the Pound remains near four-week highs as markets anticipate positive economic data from the UK later this week. The upcoming figures are expected to indicate economic recovery in October, particularly within the manufacturing sector. Meanwhile, the Bank of England is widely predicted to keep interest rates unchanged at its December meeting.

BoE Deputy Governor Sir Dave Ramsden, addressing the current economic landscape, underscored the importance of remaining vigilant in the face of persistent uncertainties. His remarks highlight the central bank’s cautious approach as it navigates a period of elevated risks, particularly in light of inflation trends and broader economic performance.

The Australian Dollar faced additional downward pressure as the Reserve Bank of Australia opted to maintain its Official Cash Rate at 4.35% during its final policy meeting of the year. RBA Governor Michele Bullock explained that while inflationary risks have eased, they still require close monitoring. The decision to hold rates at a 12-year high reflects the RBA’s cautious stance, with officials emphasizing the importance of incoming economic data, including employment figures, in shaping future policy moves.

In the realm of trade, China reported a rise in its trade surplus for November, which reached CNY 692.8 billion, up from the previous month’s CNY 679.1 billion. Exports grew modestly by 1.5% year-over-year, a significant slowdown from October’s 11.2% jump, while imports reversed their previous decline, increasing by 1.2% year-over-year. These figures offer a mixed view of China’s economic recovery as the country grapples with global demand fluctuations and domestic challenges.

The US Dollar extended its rally for a third straight day, benefiting from a cautious market environment ahead of Wednesday’s CPI release. The data is anticipated to show a slight increase in inflation, which could influence the Federal Reserve’s policy outlook.

Current market pricing suggests an 85.8% probability of a quarter-point rate cut at the Fed’s upcoming meeting, according to the CME FedWatch Tool. This expectation has provided additional tailwinds for the greenback, even as traders weigh the broader implications of the inflation data for monetary policy trajectories.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates