S&P 500 Holds Steady Amidst Treasury Yield Surge; Gold Gains Limited by Fed's Hawkish Tone | Daily Market Analysis

Key events:

- UK - BoE Interest Rate Decision (Apr)

- UK - BoE Gov Bailey Speaks

- UK - BoE MPC Member Pill Speaks

- Eurozone - ECB's De Guindos Speaks

- USA - Initial Jobless Claims

- USA - FOMC Member Daly Speaks

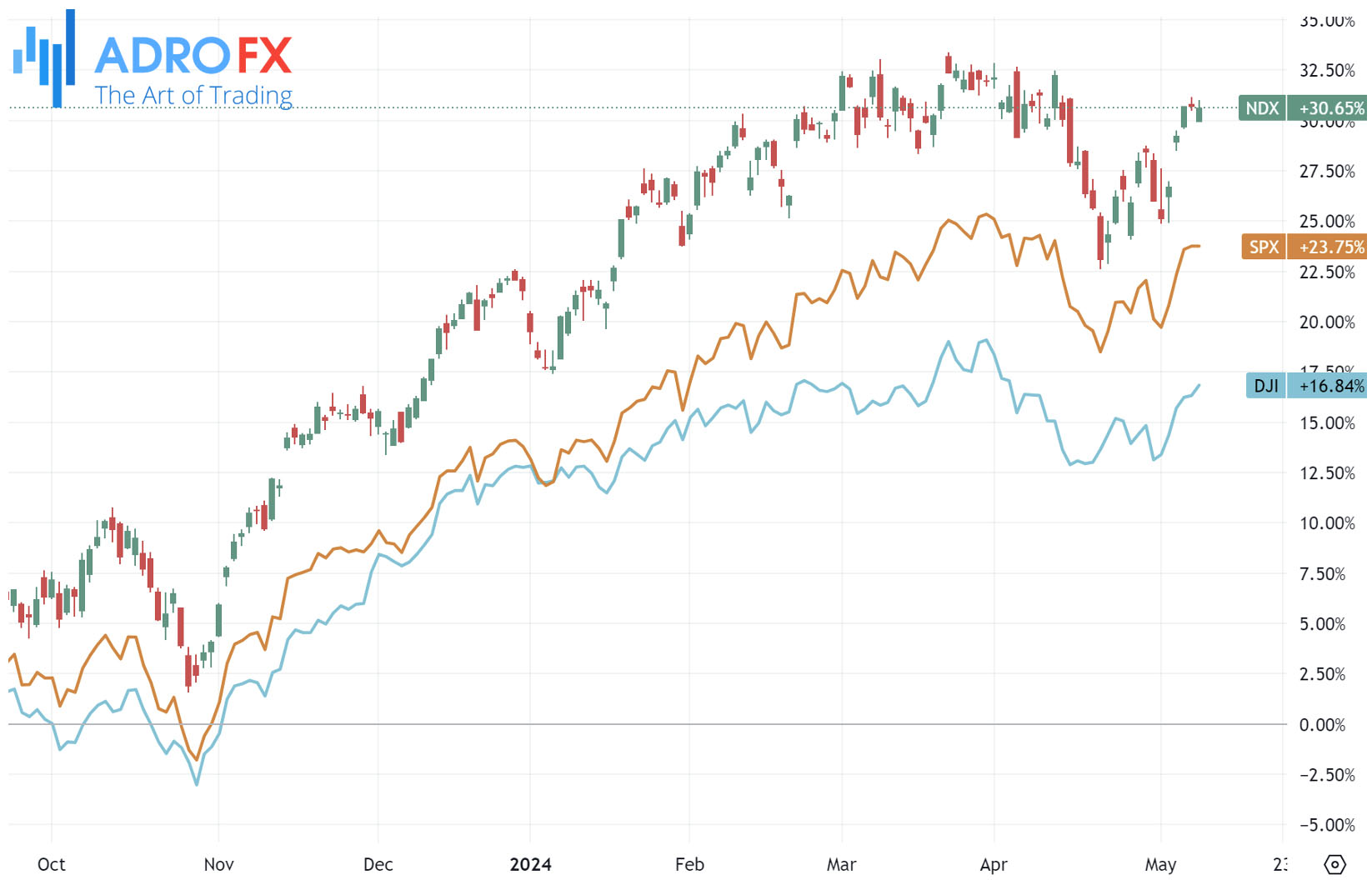

Wednesday saw the S&P 500 closing on a neutral note, with the recent market surge hitting a pause amidst the backdrop of climbing Treasury yields and a mixed bag of corporate earnings reports, dampening investor sentiment.

Meanwhile, the Dow Jones Industrial Average saw a modest uptick of 172 points, marking a 0.4% increase, while the S&P 500 ended the day unchanged, and the NASDAQ Composite experienced a slight decline of 0.2%.

The uptick in Treasury yields followed Wednesday's 10-year Treasury auction, which saw yields inching up in the face of uncertainty regarding the timing of impending rate adjustments. The auction yielded a lower-than-expected rate of 4.483%, narrowly below the pre-sale, or when-issued, rate of 4.473%. This outcome suggests a subdued investor appetite for assets within the belly of the yield curve, typically reflecting rates on securities maturing between ten and two years.

These developments unfold as Federal Reserve officials continue to affirm their commitment to maintaining steady rates in the short term, with additional Fed speakers slated to deliver remarks throughout the week.

Gold price maintains a positive trajectory on Thursday as the market awaits significant economic data releases. However, several factors, including the robust US Dollar and hawkish sentiments from the US Federal Reserve, are expected to limit the precious metal's upward potential in the short term.

Conversely, the recent growth in global gold demand stemmed from vigorous over-the-counter market investments, ongoing central bank acquisitions, and escalating demand from Asian markets, particularly China and India, according to the latest report from the World Gold Council (WGC). Additionally, amidst a risk-averse climate and escalating geopolitical tensions in the Middle East, traditional safe-haven assets like gold could experience a boost. Gold traders are eagerly awaiting fresh catalysts to drive market sentiment.

Meanwhile, the New Zealand Dollar sees continued gains for a second consecutive session, hovering around 0.6010 during Thursday's Asian session. The NZD's ascent follows the release of Chinese data, bolstered by the close trade relationship between New Zealand and China.

Chinese Imports (YoY) surged by 8.4% in April, surpassing forecasts of 5.4%, while Exports expanded by 1.5%, exceeding analysts' expectations of a 1.0% gain. Despite these positive figures, Trade Balance USD edged up to $72.35 billion from March's $58.55 billion, slightly below the anticipated $76.7 billion.

In New Zealand, the Reserve Bank of New Zealand hinted at delaying any potential monetary easing until 2025, citing higher-than-expected inflation pressures in the first quarter as justification. Such a stance could provide underlying support for the NZD.

Elsewhere, the Australian Dollar remains subdued on Thursday following the Reserve Bank of Australia's less hawkish stance, especially after last week's inflation data surpassed expectations. Although the RBA acknowledged a recent halt in controlling inflation progress, it maintained a flexible approach, opting to keep the interest rate unchanged at 4.35% on Tuesday.

Australian inflation surprised markets by ticking upward in March, diverging from expectations of stability. RBA Governor Michele Bullock underscored the need for vigilance against inflation risks, affirming that current interest rates are positioned to guide inflation toward its target range by the second half of 2025 and to the midpoint by 2026.

Meanwhile, EUR/USD faces its third consecutive session of losses, hovering near 1.0750 during Thursday's Asian trading. The driving force behind this decline is the anticipation of the Federal Reserve's commitment to raising interest rates.

In the Eurozone, March witnessed a notable rebound in monthly Retail Sales, with a 0.8% increase following a revised 0.3% decline in February. This surge marked the most significant jump in retail activity since September 2022, indicating resilience in the European consumer sector. Additionally, Retail Sales (YoY) recorded a 0.7% rise compared to February's revised 0.5% drop, signaling the first positive shift in retail since September 2022 and suggesting favorable trends in consumer spending.

However, the European Central Bank is poised to initiate a rate cut journey starting in June. ECB Chief Economist Philip Lane recently reinforced his belief that inflation is gradually moving toward the 2% target, supported by recent data.

During Thursday's early Asian session, the GBP/USD pair remained defensive around 1.2495. Traders exercised caution ahead of the Bank of England's interest rate decision, with expectations leaning toward no change. Nevertheless, speculations loom regarding a potential rate cut by the BoE amid the UK's declining inflation trajectory, possibly preceding actions by the US Fed. Market sentiment awaits speeches from BoE officials Bailey and Pill, with continued dovish remarks potentially triggering further depreciation of the Pound Sterling.

Later in the day, the US weekly Initial Jobless Claims report is scheduled, along with a speech from San Francisco Fed President Mary Daly, renowned for her dovish stance within the US central bank.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates