Resurgence in US Stocks Driven by Encouraging Economic Data | Daily Market Analysis

Key events:

- USA – Fed Chair Powell Speaks

- USA – Crude Oil Inventories

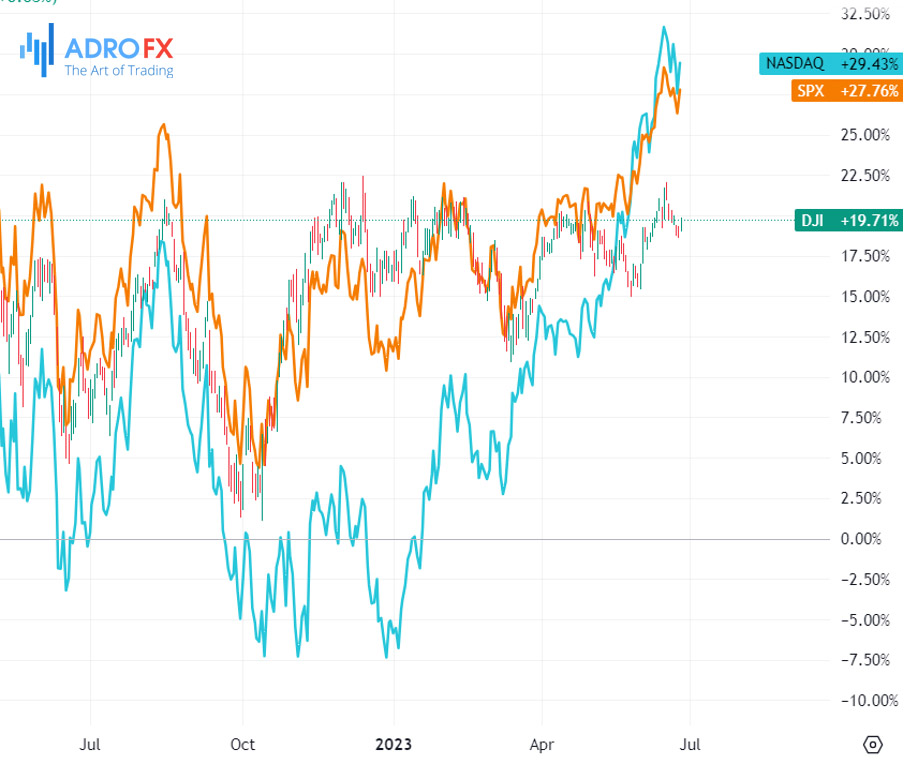

Tuesday saw a resurgence in US stock indices, marking a recovery from a recent series of losses. This rebound was driven by encouraging economic data, which alleviated concerns among investors about an imminent recession resulting from the Federal Reserve's aggressive interest rate hikes.

On Tuesday, the Dow Jones Industrial Average, consisting of highly regarded blue-chip stocks, put an end to its six-day period of losses. Meanwhile, the Nasdaq Composite, primarily composed of technology-related companies, was on track to achieve its strongest performance in the first half of a year in four decades. Additionally, the S&P 500 rebounded after experiencing declines in five out of the last six trading sessions.

Notably, separate reports revealed unexpected growth in new orders for vital US-manufactured capital goods in May. Additionally, sales of new single-family homes experienced a significant surge during the same month, while US consumer confidence reached a nearly 1-1/2 year high in June.

The positive data provided investors with a compelling reason to reenter the stock market following a period of a significant correction in the preceding sessions. Mark Luschini, the chief investment strategist at Janney Montgomery Scott in Philadelphia, characterized this recent correction as a "pretty vicious" one.

Yesterday, the euro exhibited strong performance following a hawkish stance adopted by ECB President Christine Lagarde and several other members of the ECB governing council regarding future interest rate increases. It appears that the central bank has now committed to another rate hike in July, with the possibility of another increase in September. Lagarde has also dismissed the likelihood of rates decreasing swiftly, although her previous U-turns on such matters have not been forgotten. One memorable instance was her declaration at the end of 2021 that there was a low probability of rate hikes in 2022.

The pound has also experienced a slight increase as traders intensify their expectations for a rate hike that could push the Bank of England to raise rates above 6%.

On the other hand, the Japanese yen continues to face significant pressure, leading to a decline against the US dollar, with the exchange rate reaching 144.00, as well as reaching an 8-year low against the pound.

Meanwhile, the Canadian dollar (CAD) has demonstrated exceptional strength among G10 currencies in the past month and is maintaining most of those gains leading up to the release of the Consumer Price Index (CPI) data today. During the overnight session, USD/CAD reached its lowest level since September 2022, and while there has been a slight uptick in European trading, the downward trend observed in June remains intact. The focus for the Canadian dollar now shifts to the upcoming release of May CPI data in Canada.

According to HSBC economists, there is an anticipation of a 0.5% month-on-month increase in price pressures (compared to the consensus estimate of 0.4%). This rise is expected to be driven by persistent upward pressure on mortgage interest costs and a seasonal uptick in food prices. If the actual price pressures surpass expectations on the upside, it could reinforce the likelihood of a quarter-point interest rate hike at the Bank of Canada's July meeting. Such a move would further strengthen the Canadian dollar through the impact on interest rates. At present, swap markets are pricing in a 15-basis point increase in rates.

However, it is worth noting that the year-on-year inflation rates for both headline and core measures are projected to slow down from the levels seen in April, as the influence of base effects becomes more pronounced.

This week, there is anticipation for additional economic data, including a crucial inflation indicator, as well as a speech by Fed Chair Jerome Powell at the European Central Bank Forum in Sintra, Portugal. These events are expected to offer insights into the future direction of interest rates.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates