Mixed Signals and Rate Speculations Dominate Investor Sentiment | Daily Market Analysis

Key events:

- Canada - New Housing Price Index (MoM) (Jul)

On Friday, the US stock market presented a mixed picture, reflecting a situation where signs of resilience in the US economy are simultaneously fueling concerns about the prolonged maintenance of elevated interest rates.

The Dow Jones Industrial Average demonstrated a modest rise of 30 points, equivalent to a 0.1% increase. Conversely, the S&P 500 experienced a slight dip of 0.2%, and the NASDAQ Composite saw a more notable decrease of 0.5%.

Losses in the technology sector were accentuated, with recent weakness compounding concerns that the upward trajectory of Treasury yields, which is particularly adverse for growth-oriented sectors like technology, might persist. This apprehension has been amplified by the expectation that Federal Reserve Chair Jerome Powell will reaffirm the need for an extended period of elevated interest rates during next week's upcoming Jackson Hole symposium.

Amid these developments, Treasury yields exhibited a momentary pause on Friday, a respite that followed closely after the 10-year Treasury yield had reached its highest level since 2007 in the previous session.

Should the current trend continue, there is a possibility that the 10-year Treasury yield could make further gains, potentially leading to a breakthrough towards the 5% mark.

As for the currencies, the dollar built upon its momentum after achieving five consecutive weeks of gains. Investors are now focused on the Federal Reserve's Jackson Hole symposium, seeking insights into the eventual settling point for interest rates beyond the ongoing hiking cycle.

During the previous week, the dollar saw a notable 0.7% appreciation against the euro. It made slight gains against the yen and experienced a significant surge of over 1% against the Antipodean currencies. This was driven by a significant leap in US Treasury yields, spurred by the anticipation of interest rates remaining at elevated levels for a prolonged period.

In the early trading hours, both the Australian dollar, at $0.6402, and the New Zealand dollar, at $0.5913, demonstrated slight declines, positioning them uncomfortably close to the nine-month lows reached last week. This decline was influenced by a rate cut in China that did not meet market expectations, causing disappointment among investors.

China's decision involved a reduction of its one-year benchmark lending rate by 10 basis points, while the five-year rate remained unchanged. This deviated from economists' forecasts, which had anticipated cuts of 15 basis points for both rates.

Despite the central bank's efforts to establish a firm trading range for the yuan, the currency slipped beyond 7.3 per dollar. Its latest trading value stood at 7.3011. However, it managed to stay above last week's lows beyond 7.31. Notably, this prompted state banks to engage in spot markets during London and New York trading hours as buyers.

Bitcoin, which experienced a significant decline to a two-month low in the previous week due to a combination of escalating US yields and China's economic deceleration prompting selling, is currently recuperating those losses and holding at a value of $26,129.

Investors are eagerly anticipating an upcoming speech by Federal Reserve Chair Jerome Powell, which is expected to shed light on both the economic trajectory and the forthcoming direction of interest rates.

Scheduled for 10:05 am ET on Friday, Powell's address follows the release of minutes from the central bank's July meeting last week. These minutes revealed that a majority of policymakers remain concerned about potential upward risks to inflation. This suggests that the possibility of further rate increases cannot be discounted.

Of particular interest to investors will be Powell's perspective on whether additional policy tightening will be necessary to counter inflationary pressures, or if the progress achieved so far is sufficient to maintain the current rate stance. Additionally, market observers will be attuned to any indications suggesting the Fed is deliberating the prospect of rate reductions in the year 2024.

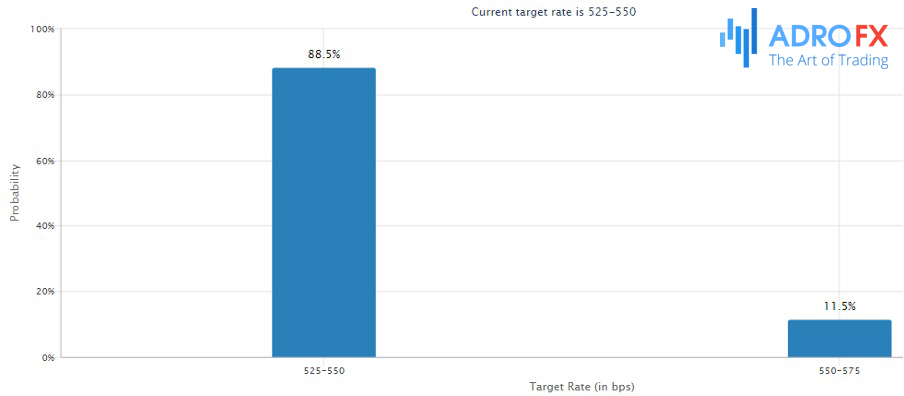

According to the CME Fed watch tool, traders are assigning an 88.5% probability that the Federal Reserve will maintain rates at their present levels during the September meeting. This underlines the current sentiment regarding the near-term trajectory of interest rates.

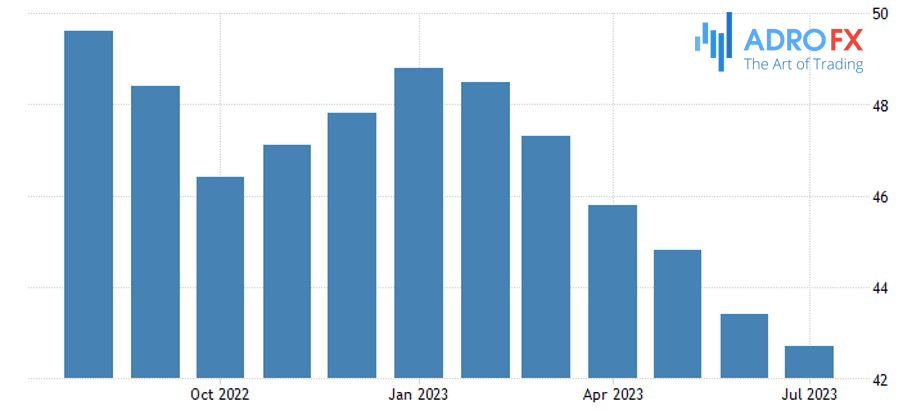

On Wednesday, both the Eurozone and the UK are set to release their PMI (Purchasing Managers' Index) data, a crucial metric that could offer insights into potential actions by central banks. These figures may influence decisions by the European Central Bank (ECB) in September regarding interest rates, and also impact considerations for a significant rate increase by the Bank of England.

Recent months have witnessed a decline in Eurozone and UK PMIs, reflecting a combination of sluggishness in the service sector and a contraction in manufacturing activity.

Investors are keeping a close eye on ECB President Christine Lagarde's speech at the Jackson Hole symposium on Friday. Her remarks are being scrutinized for any indications that could offer a glimpse into the central bank's upcoming course of action in September.

In a statement made in July, Lagarde emphasized the ECB's open-minded approach to future rate decisions. She highlighted that policymakers were entering a phase where data dependency would play a key role in shaping their choices.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates