Mixed Performance on Wall Street as US Debt Ceiling Concerns and Nvidia Surge Impact Stocks; Eurozone Inflation Data Awaited | Daily Market Analysis

Key events:

- Canada – GDP (MoM) (Mar)

- Eurozone – ECB President Lagarde Speaks

- USA – JOLTs Job Openings (Apr)

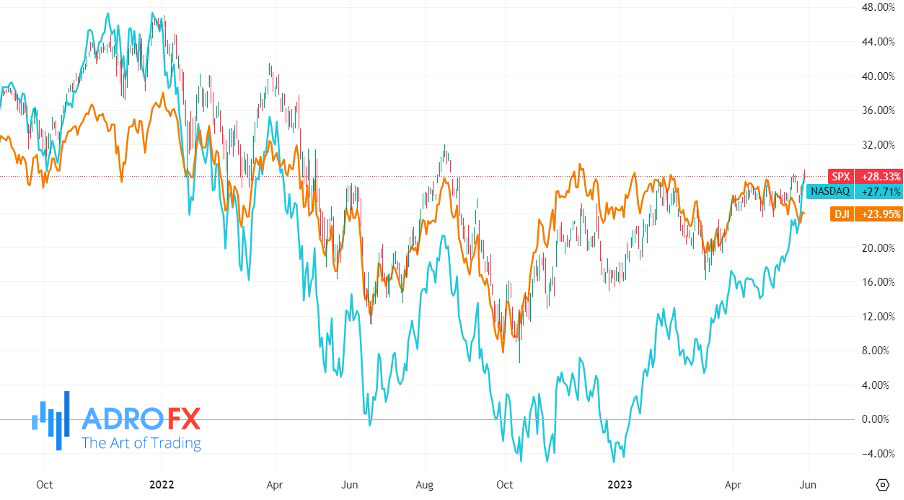

Tuesday's closing session on Wall Street saw a mixed performance among stocks. Concerns emerged due to certain US lawmakers opposing a deal to raise the debt ceiling, which amounted to $31.4 trillion. However, the market received support from a significant surge in Nvidia (NASDAQ: NVDA) shares. This surge momentarily elevated the chipmaker's value to $1 trillion, a rare achievement.

The S&P 500 index closed with minimal change, maintaining its proximity to its highest level since August 2022, just above the 4,200-point mark. On the other hand, the Dow Jones Industrial Average experienced a slight decline, while the Nasdaq Composite saw an increase. Despite the mixed performance, both the S&P 500 and the Nasdaq were on track to achieve monthly gains for May.

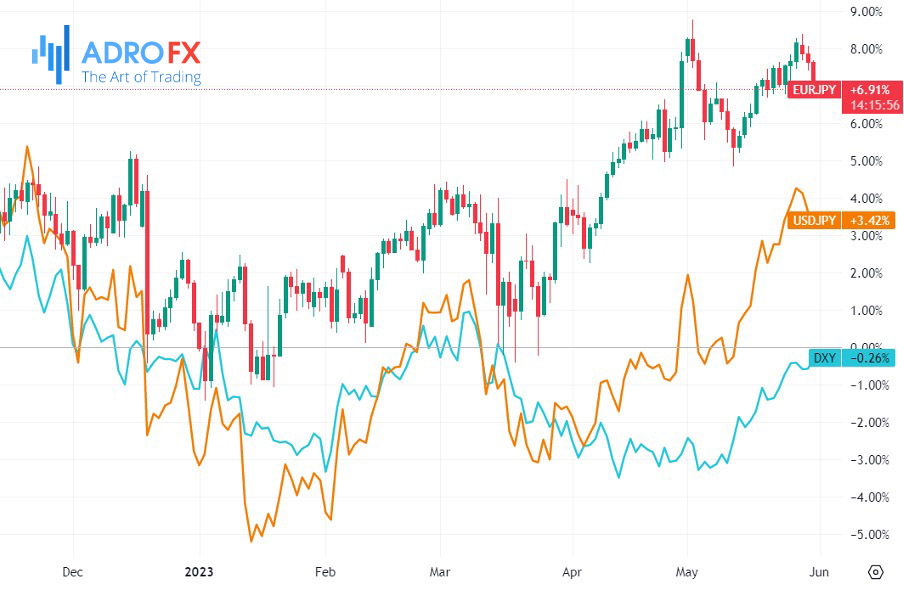

The combination of increased Australian CPI, drone attacks on Moscow, and ongoing discussions about the US debt ceiling have collectively contributed to the depreciation of various currencies against the Dollar today. The Dollar Index has surged to levels above 104, while the Euro is on the brink of falling below 1.07. Currency pairs such as EUR/JPY and USD/JPY are trending towards 149 and 138, respectively. Additionally, the Pound and the Australian Dollar are displaying bearish tendencies, approaching levels around 1.2350/1.23 and 0.6450, respectively.

According to current indications from money markets, there is a prediction of a substantial 100-basis point tightening by the Bank of England (BoE) by November, potentially resulting in a Bank Rate of 5.50%. However, analysts hold the opinion that such a significant level of tightening is highly unlikely. It is possible that the traditionally cautious BoE might attempt to counter these expectations through verbal means.

Nevertheless, the UK's economic data plays a pivotal role in shaping market sentiment. The upcoming jobs/wages data on June 13th or the May CPI data on June 21st are anticipated to have the most significant impact on whether the market adjusts its aggressive expectations regarding tightening.

Until then, it is expected that the EUR/GBP currency pair will find support around 0.8650, with the subsequent target being 0.8600/8610. Conversely, GBP/USD may exhibit greater resistance to the strength of the dollar. There is a chance that support within the range of 1.2275/2300 could temporarily hold.

Meanwhile, gold prices experienced a slight decline as market participants awaited further information regarding the potential increase of the US debt ceiling. The rise in interest rates has led to an increase in the opportunity cost of investing in non-yielding assets, which negatively affected gold throughout 2022.

However, in the event of a US default, the demand for gold as a safe haven asset may increase, particularly if such a default triggers a recession. US lawmakers are expected to vote this week on a bipartisan bill aimed at raising the debt ceiling and avoiding an economic crisis.

Today, there will be additional inflation data released from the Euro area, including flash inflation data from Germany, France, and several other countries within the Eurozone. The market is expecting a decline in inflation, but the speed at which it decreases will be crucial for market reactions. In France, the anticipated month-on-month increase for May is expected to be 0.3%, compared to the 0.6% increase seen in April. For Germany, the expected month-on-month rise for May is 0.2%, down from the 0.4% recorded in April.

Currently, the peripheral countries in the Eurozone are outperforming the core countries, leading to a narrowing of the spread between 10-year Italian government bonds (BTPS) and German bunds to around 180 basis points. Additionally, the peripheral countries are also performing better compared to EU bonds, with the 10-year bonds of Portugal (rated BBB) approaching parity with the 10-year bonds of the EU (rated Aaa). The spread of the Bund ASW (asset swap) remains relatively stable.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates