Markets Hit New Highs Despite Trade Tensions and Policy Uncertainty | Weekly Market Analysis

Key events this week:

Monday, June 30, 2025

- China - Manufacturing PMI (Jun)

- UK - GDP (YoY) (Q1)

- UK - GDP (QoQ) (Q1)

- USA - Chicago PMI (Jun)

Tuesday, July 1, 2025

- Eurozozne - CPI (YoY) (Jun)

- USA - Fed Chair Powell Speaks

- USA - S&P Global Manufacturing PMI (Jun)

- USA - ISM Manufacturing PMI (Jun)

- USA - ISM Manufacturing Prices (Jun)

- USA - JOLTS Job Openings (May)

Wednesday, July 2, 2025

- USA - ADP Nonfarm Employment Change (Jun)

- USA - Crude Oil Inventories

Thursday, July 3, 2025

- USA - Average Hourly Earnings (MoM) (Jun)

- USA - Initial Jobless Claims

- USA - Nonfarm Payrolls (Jun)

- USA - Unemployment Rate (Jun)

- USA - S&P Global Services PMI (Jun)

- USA - ISM Non-Manufacturing PMI (Jun)

- USA - ISM Non-Manufacturing Prices (Jun)

Friday, July 4, 2025

- USA - Independence Day

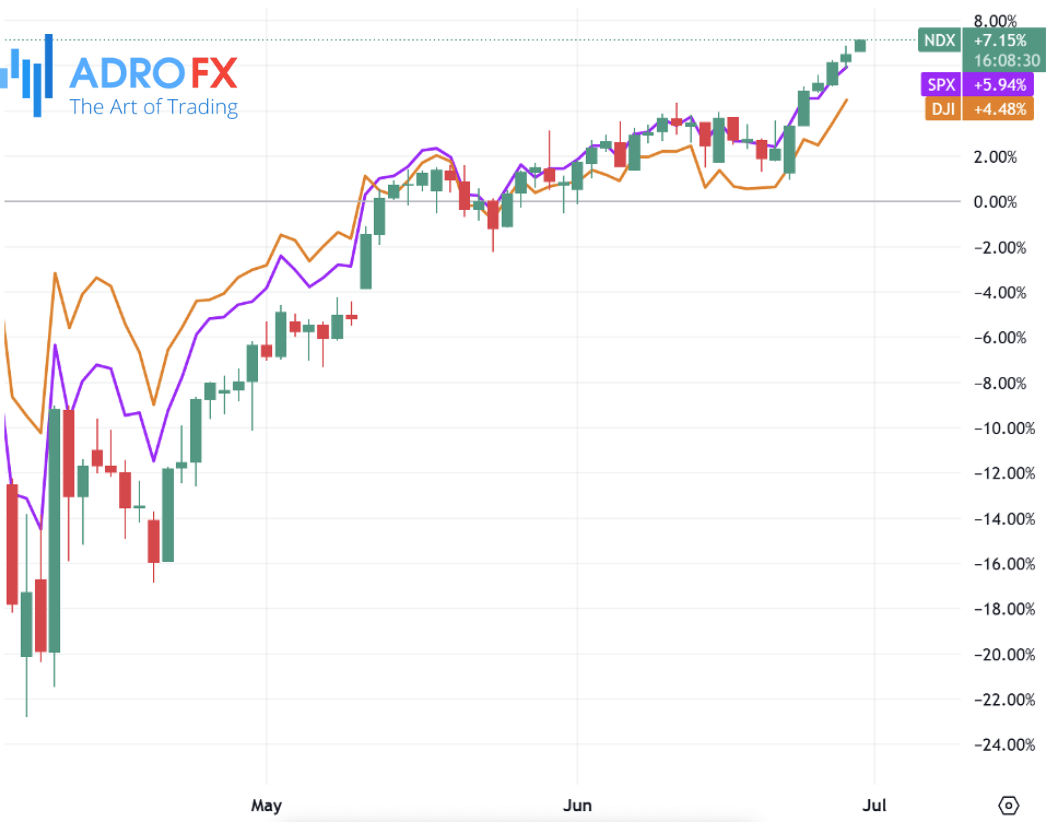

The S&P 500 closed at fresh all-time highs on Friday, recovering from a steep intraday dip that came after President Trump abruptly called off trade talks with Canada. The surprise move rattled markets and revived concerns about the possibility of a renewed trade war. Despite these fears, investor sentiment proved resilient by the session’s end, with the Dow Jones Industrial Average climbing 432 points or 1%, the S&P 500 gaining 0.5% to close at a record 6,169.84, and the NASDAQ Composite advancing by 0.5%.

Much of the market’s strength came from hopes that the Federal Reserve will lean more dovish in the coming months, especially in light of softer economic data and elevated geopolitical risks. In Washington, attention turned to legislative developments as the Senate narrowly voted 51–49 to proceed with debate on President Trump’s “One Big Beautiful Bill” - a sweeping legislative package that combines tax cuts, major changes to domestic spending, and funding for border security. The move sets up a turbulent week of negotiations, with up to 20 hours of debate ahead. According to estimates from the Congressional Budget Office, the Senate’s version of the bill could add as much as $3.3 trillion to the federal deficit over the next ten years. While Senate Republicans aim to finalize the process before the July 4th holiday, the House has signaled resistance, citing both the fiscal cost and rushed timeline. Still, the House had already passed its version of the bill last month, signaling ongoing momentum even as internal disagreements persist.

Trade developments remained in the spotlight, with US Commerce Secretary Howard Lutnick announcing that a framework had been reached with China on trade terms. Lutnick further indicated that deals with as many as 10 major trading partners were likely in the near future. However, statements from other administration officials offered less clarity. A White House spokesperson later added that China merely agreed to explore an “additional understanding” regarding the Geneva agreement. Treasury Secretary Scott Bessent added to the mixed messaging by suggesting the US expects roughly 15 trade deals soon, while Trump himself told reporters he’s anticipating somewhere between five and seven finalized agreements. The unclear and often contradictory commentary from various officials left markets uncertain about the actual progress on trade.

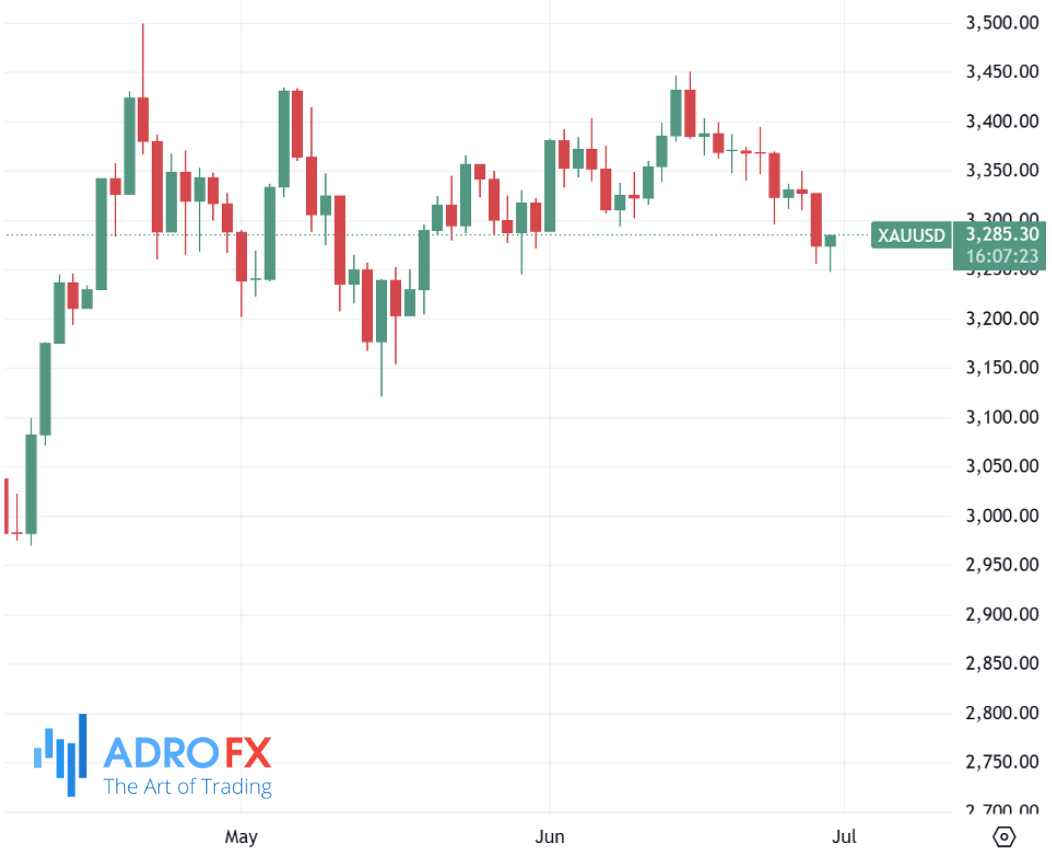

Commodity markets responded to these developments as well. Gold prices managed to recover slightly during Monday’s Asian session, helped by rising expectations of multiple Fed rate cuts this year. A weakening US Dollar supported the yellow metal’s gains, as gold becomes more attractive to foreign buyers when the dollar depreciates. Still, risk-on sentiment driven by an improving US-China relationship and a ceasefire deal between Iran and Israel may limit gold’s appeal as a safe-haven asset in the short term.

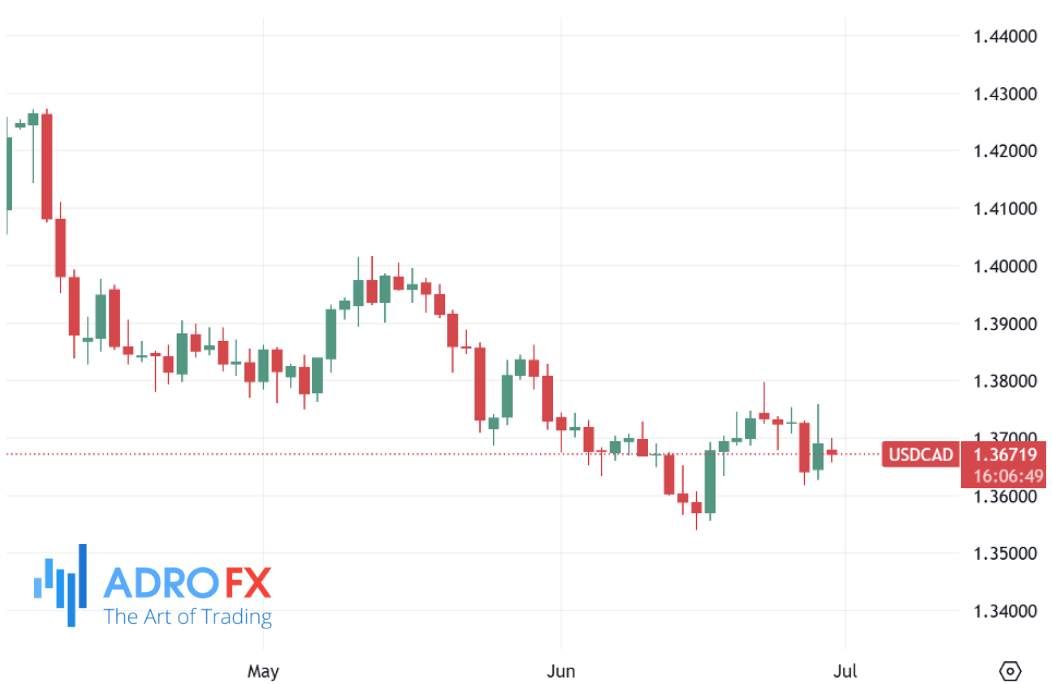

In currency markets, USD/CAD declined to around 1.3670 as the Canadian Dollar benefited from a combination of trade optimism and stronger oil prices.

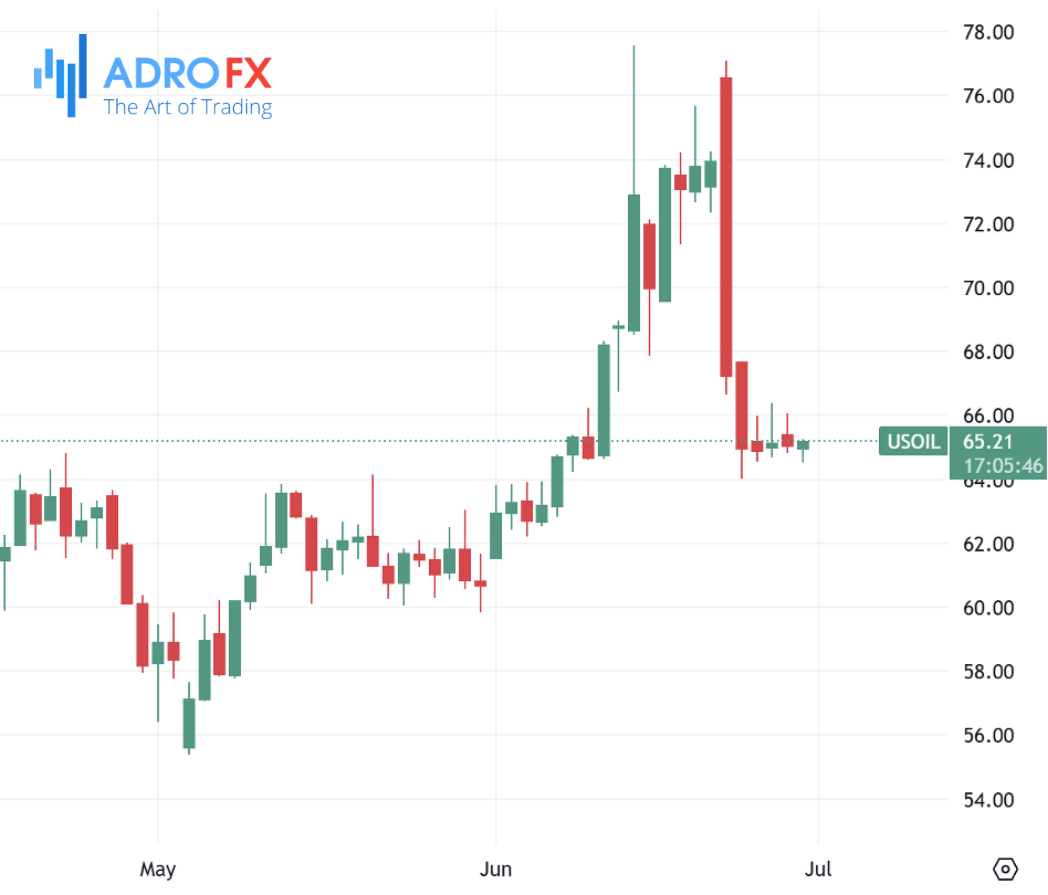

The Canadian Finance Ministry’s announcement that it would drop the digital services tax to foster progress in US-Canada trade negotiations provided a further boost. Both President Trump and Canadian Prime Minister Mark Carney confirmed their commitment to reach an agreement by July 21. Given Canada’s status as the largest crude oil exporter to the US, the loonie also drew strength from climbing oil prices, with WTI crude trading near $64.70 per barrel. While oil’s upside remains capped amid easing supply fears due to the Middle East ceasefire, the potential for sanctions relief on Iran and an anticipated production increase by OPEC+ also play key roles in moderating oil's rally.

Elsewhere, the British Pound gained slightly, with GBP/USD trading around 1.3720 in early Monday activity. Investors looked ahead to the release of UK GDP figures for Q1. Expectations of a US rate cut as early as September weighed on the greenback, further supporting the pound. Meanwhile, the Bank of England’s cautious tone on easing - prompted by persistently high core inflation - also lent some support to sterling. Still, political instability in the UK remained a factor, as Prime Minister Keir Starmer faced significant pushback from over 100 Labour MPs regarding welfare reform plans designed to reduce spending by £5 billion per year. The internal party rebellion could complicate further fiscal reforms, adding an additional layer of uncertainty for the pound.

The euro also gained momentum, with EUR/USD climbing toward 1.1720. The weakening dollar helped the euro extend its rally as traders increasingly anticipate Fed easing later this year. Meanwhile, German economic data - particularly retail sales and consumer inflation figures - are expected to drive further euro movement this week. On Friday, European Central Bank Governing Council member Klaas Knot noted that while the current policy rate is appropriate, one more 25 basis point cut could be likely by year-end. The market has now largely priced in just one ECB rate cut in the next 12 months, with expectations that the policy rate will bottom out around 1.75%.

The Australian Dollar also firmed, with AUD/USD reaching 0.6535 as early trading kicked off Monday. Renewed concerns over trade rhetoric from the White House weighed on the dollar, while China’s economic data provided modest support for the Aussie. China’s non-manufacturing PMI for June rose to 50.5, signaling a modest expansion in the sector and bolstering optimism for demand in Australia’s largest export market.

As the week progresses, attention will turn to a series of US employment reports that could reshape expectations for monetary policy. The June payrolls report is projected to show the addition of 110,000 new jobs, down from 135,000 in May. However, projections range widely, with estimates between 75,000 and 140,000. Meanwhile, unemployment is expected to tick slightly higher to 4.3% from 4.2%. These figures, along with other macroeconomic indicators and geopolitical developments, could influence the Federal Reserve’s messaging in the coming weeks and determine the pace and timing of future rate moves.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates