Geopolitical Tensions, Economic Surges, and Earnings Season Kick-Off | Daily Market Analysis

Key events:

- Eurozone - ECB's De Guindos Speaks

- Eurozone - ECB's Enria Speaks

- UK - BoE MPC Member Mann

During Sunday's evening trade, US stock futures were on a downward trajectory, influenced by a flight to safety following a recent Hamas attack on Israel. The Israeli-Palestinian conflict escalated into a full-blown war over the weekend, as members of the Islamist group Hamas launched attacks on several Israeli towns, resulting in hundreds of casualties and the abduction of dozens. In response, Israel conducted air strikes on various targets in Gaza, leading to additional casualties.

This newly heightened conflict, coupled with the ongoing Ukrainian war, has sent ripples through the markets, particularly impacting oil prices. The benchmark Brent and Nymex contracts initially surged by as much as 5% before retracing slightly, interrupting a previous decline in prices.

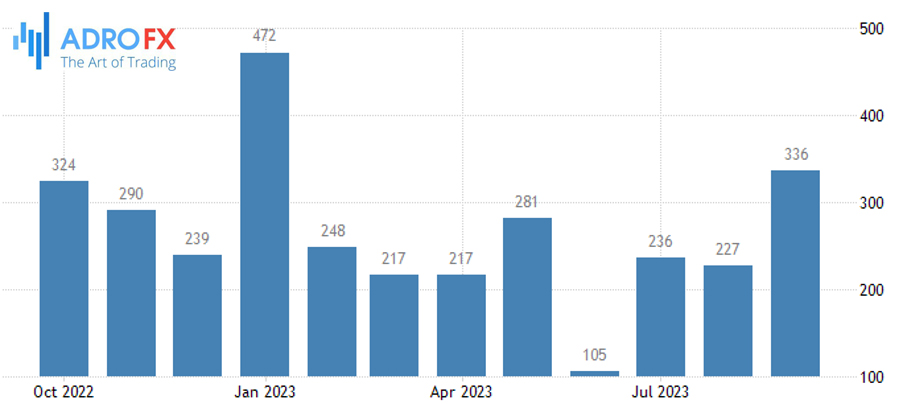

In contrast to the geopolitical turmoil, the US economy witnessed a notable surge in job growth in September, adding 336,000 jobs and maintaining the unemployment rate at 3.8%, despite persistent labor shortages. This unexpected uptick in employment figures could potentially influence the Federal Reserve's stance on future interest rate hikes as it grapples with inflation.

Hourly wages experienced a modest 0.2% increase, indicating a return to wage growth levels observed before the pandemic. Both the government and private sectors contributed to this job creation, with the hospitality and healthcare industries at the forefront. The labor-force participation rate remained steady at a post-pandemic high of 62.8%, reflecting continued demand for goods and services during a surge in third-quarter GDP.

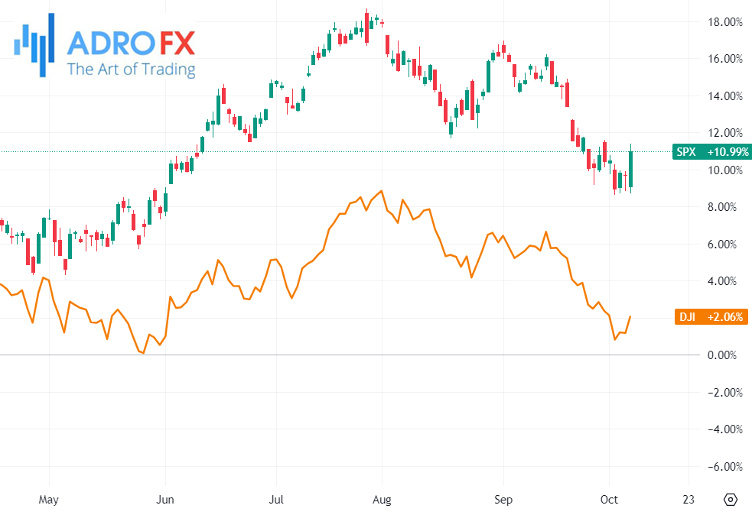

In response to these developments, markets exhibited positive reactions on Friday. The Dow Jones Industrial Average and S&P 500 rebounded from early losses, while the yield on the 10-year Treasury rose to 4.78%. This optimistic market response mirrors investor confidence following the news of increased job growth and stability in the labor market.

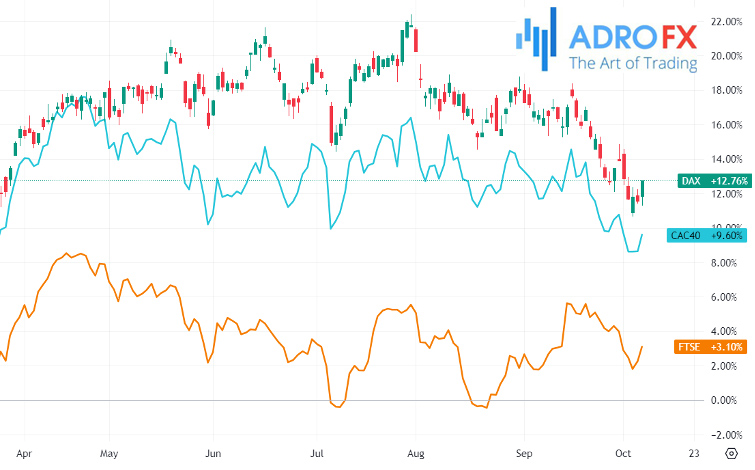

Looking ahead, European stock markets are anticipated to open mostly lower on Monday. DAX futures contracts in Germany were down 0.9%, CAC 40 futures in France dropped 0.3%, and FTSE 100 futures contracts in the UK traded largely flat.

The Australian Dollar (AUD) finds it challenging to sustain the winning streak that commenced last Wednesday. The AUD pair is receiving upward momentum driven by robust commodity prices amid the ongoing turmoil in the Middle East.

Australia has made a commitment to ensure a stable supply of energy resources to Japan during the fifth Japan-Australia Ministerial Economic Dialogue. This agreement underscores the strategic partnership between the two nations, emphasizing the significance of a consistent and reliable flow of energy resources. This cooperation likely encompasses various energy sources, including coal and liquefied natural gas (LNG).

The price of gold (XAU/USD) underwent a remarkable intraday turnaround on Friday, surging by over 1.3% from the $1,810 range, marking its lowest level since March 8, which occurred in the aftermath of the release of the United States monthly jobs data.

However, the gold price is encountering challenges in sustaining its upward momentum beyond the $1,855 range. Investors are now closely monitoring this week's release of the FOMC meeting minutes and the US consumer inflation figures for potential market-moving insights.

In the world of corporate news, the third quarter earnings season is kicking off this week, drawing particular attention to the reports from several major Wall Street banking giants, including JPMorgan Chase (NYSE: JPM), Citigroup (NYSE: C), and Wells Fargo (NYSE: WFC), scheduled for release on Friday.

This earnings season carries significant weight as it could shape the short-term trajectory of stocks, especially considering that the S&P 500 still maintains a 10% gain for the year despite its recent retreat.

In other developments, the French and German governments are scheduled to convene later on Monday for a two-day retreat in Hamburg. This meeting between the European Union's two largest powers aims to address and resolve a range of disagreements in areas such as energy, industry, and defense policy.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates