Fed Rate Hints, Bank Earnings, and Currency Rebounds Dominate Investor Sentiment | Daily Market Analysis

Key events:

- UK - CPI (YoY) (Mar)

- Eurozone - CPI (YoY) (Mar)

- USA - Crude Oil Inventories

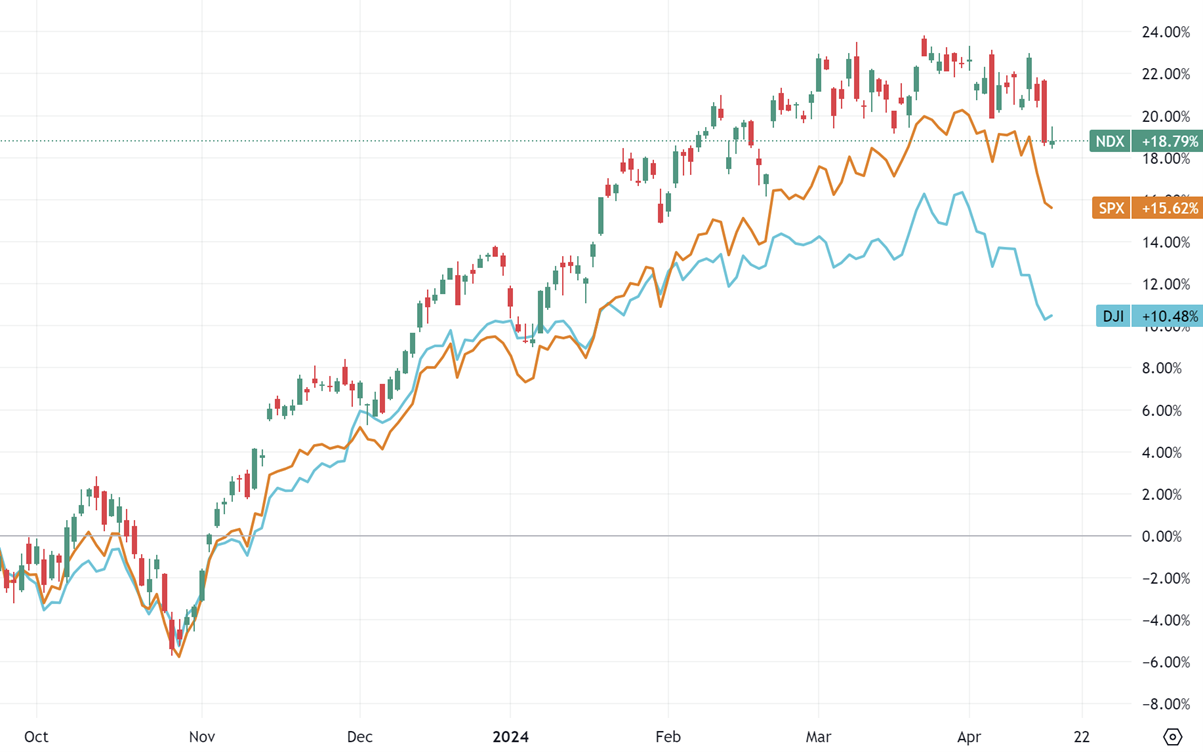

Tuesday saw the S&P 500 concluding on a downward trajectory, with investors grappling with erratic fluctuations, particularly after Federal Reserve Chairman Jerome Powell hinted at the necessity of sustained higher rates. This indication followed recent inflation figures that surpassed expectations.

Dow Jones Industrial Average recorded an ascent of 63 points, equivalent to a 0.2% increase. Conversely, the S&P 500 experienced a 0.2% decline, while the NASDAQ Composite slipped by 0.1%.

Bank of America (NYSE: BAC) and Morgan Stanley (NYSE: MS) marked the culmination of the latest round of major bank earnings, with Morgan Stanley notably delivering an impressive performance bolstered by its investment banking and sales and trading divisions. Although Bank of America Corp reported quarterly results that surpassed analysts' expectations, its stock plummeted nearly 4% amidst concerns regarding its valuation following a recent surge.

"Given the significant share price appreciation over the past approximately six months, we no longer perceive adequate upside to recommend the shares," HSBC stated in a research note on Tuesday, citing various risks including pressure on deposit costs and outflows.

Tesla Inc (NASDAQ: TSLA) witnessed a decline exceeding 2%, causing its market capitalization to dip below $500 billion, as bearish sentiment on the company persists amid dwindling demand, prompting announcements of layoffs exceeding 10%. Adding to the negativity, the Wall Street Journal reported on Tuesday that the electric vehicle manufacturer postponed cybertruck deliveries, citing buyer feedback.

The Australian Dollar halted its three-day descent on Wednesday, staging a recovery from levels unseen since mid-November. Nonetheless, hawkish comments from Fed officials and an influx of safe-haven flows may fortify the US Dollar and potentially restrict the upside of AUD/USD in the short term.

Meanwhile, the Australian Dollar gained momentum as the ASX 200 Index rebounded following three consecutive days of losses. However, AUD encountered hurdles, possibly due to risk aversion, as investors exercised caution awaiting Israel's response to Iran's air strike on Saturday. A Reuters report indicated that Israel's war cabinet postponed its third meeting, initially slated for Tuesday, to determine a reaction to Iran's unprecedented direct attack, now rescheduled for Wednesday. Simultaneously, Western allies are contemplating the swift imposition of new sanctions against Tehran to deter Israel from escalating the situation further.

The US Dollar Index retreated from a five-month pinnacle of 106.51 reached on Tuesday, potentially influenced by a slight dip in US Treasury yields. Federal Reserve Chairman Jerome Powell's remarks on Tuesday, suggesting limited progress on inflation this year and a longer-than-anticipated timeline to achieve the 2% target, might have contributed to a hawkish sentiment, lending support to the US Dollar.

During the early Asian session on Wednesday, the NZD/USD pair staged a rebound to 0.5905, bouncing off its yearly low of 0.5860. This upward movement was propelled by the anticipation that the Reserve Bank of New Zealand is unlikely to lower its Official Cash Rate soon, thereby boosting the New Zealand Dollar against the US Dollar.

Data released by Stats NZ indicated a continued decline in the annual rate of inflation in New Zealand, with the CPI rising by 4.0% YoY in the first quarter of 2024. Although the rate of price increases moderated compared to previous quarters, it still exceeds the Reserve Bank of New Zealand's target range of 1 to 3 percent. This persistent but slightly alleviated inflationary pressure suggests that rate cuts by the Reserve Bank of New Zealand are unlikely in the short term, providing support to the NZD.

Meanwhile, during the early Asian trading hours on Wednesday, the USD/JPY pair experienced mild losses, hovering near 154.65. Expectations of a delayed easing cycle by the Fed to September, instead of June, due to the robust US economy and persistent inflation data, offered some support to the US Dollar against the Japanese Yen. However, escalating tensions in the Middle East could bolster safe-haven assets like the JPY and potentially limit the pair's upside.

Recent data released by the US Census Bureau revealed a 14.7% decline in US Housing Starts for March, following a revised 12.7% increase in February. Building Permits also decreased by 4.3%, contrasting with the previous reading's rise of 2.3%. Industrial Production met market expectations, increasing by 0.4% MoM in March.

Fed officials, including Chairman Jerome Powell, reiterated the data-dependent nature of policy decisions and refrained from committing to initiating interest rate cuts. Powell emphasized that inflation has not returned to the 2% target, suggesting that interest rate cuts are unlikely in the near term.

Conversely, the Bank of Japan is adopting a more discretionary approach to policy setting, with reduced emphasis on inflation. This ongoing stance continues to weigh on the JPY and favor the USD/JPY pair. Investors await fresh insights from the BOJ's upcoming policy meeting on April 25–26, particularly regarding quarterly growth and price projections, for further market direction.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates