Dow Slumps Amid Job Market Strength, Raising Rate Hike Worries; Microsoft Bucks Trend with AI Advancements | Daily Market Analysis

Key events:

- USA - Average Hourly Earnings (MoM) (Jun)

- USA - Nonfarm Payrolls (Jun)

- USA - Unemployment Rate (Jun)

On Thursday, the Dow closed with a decrease as strong job market data prompted expectations of additional Federal Reserve rate hikes. This led to a surge in Treasury yields, causing concerns in the market. The Dow Jones Industrial Average dropped by 1.1% or 366 points, while the Nasdaq and the S&P 500 both experienced declines of 0.8% and 0.80% respectively.

Despite the overall market decline, Microsoft Corporation (NASDAQ: MSFT) managed to gain nearly 1% due to optimism surrounding its AI-led advancements. According to Morgan Stanley, Microsoft is well-positioned in the software industry to benefit from the estimated $90 billion generative AI growth opportunity by fiscal 2025. As a result, Morgan Stanley raised its price target on Microsoft from $355 to $415.

On the other hand, Meta (formerly known as Facebook) saw its early-day gains disappear, despite launching its Twitter competitor app called Threads. Meta CEO Mark Zuckerberg announced that Threads had attracted over 30 million sign-ups since its launch on Wednesday night.

In May, inflation expectations for the medium term in the Eurozone showed a decline, with the 12-month expectation gauge dropping from 4.1% to 3.9%. However, the long-term (three-year) inflation expectations, which hold greater importance for the European Central Bank (ECB), remained unchanged at 2.5%. This level is significantly higher than the ECB's target of 2%. With the latest flash core Consumer Price Index (CPI) estimates for June, those who advocate for tighter monetary policies within the ECB have substantial justification to support their stance.

Today, the economic calendar in the Eurozone is relatively light, and the movement of the EUR/USD exchange rate will be influenced by the market's response to US data.

Moreover, the market continues to exhibit a high level of sensitivity towards price-related developments, and there is ongoing concern regarding the Bank of England's (BoE) aggressive tightening expectations, which anticipate a 140 basis point increase by January 2024. This projection raises the possibility of a reassessment, which could pose downside risks for the British Pound and impact the GBP/USD exchange rate.

Although the EUR/GBP pair has experienced weakening in the last two sessions, it may find some support at its current levels and potentially move towards the 0.8600 mark again. This shift could be driven by the potential threat of a repricing of the previously overbought pound in response to the actions of the Bank of England.

Yesterday's market sell-off was triggered by the release of the Federal Reserve minutes, which revealed a greater inclination for further tightening than previously anticipated. This direction gained further momentum with the release of strong ADP payrolls and ISM services reports, indicating that the US labor market remains robust and is expected to continue performing well.

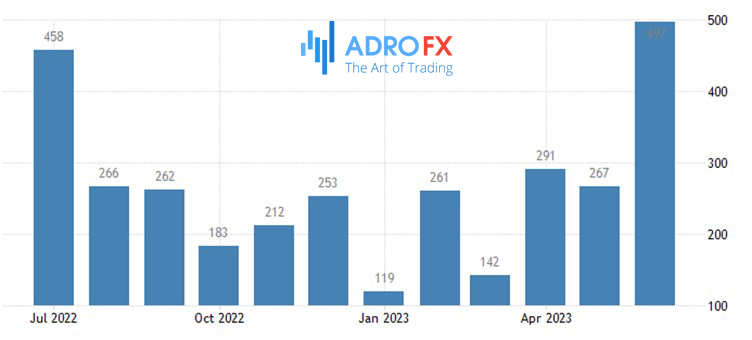

The ADP payrolls report for June showed an impressive addition of 497,000 new jobs. However, it is worth noting that a majority of these positions were in lower-paid service roles. Additionally, the prices paid component of the ISM services report slowed to its lowest level in three years.

The resilience of the labor market poses a challenge for the Federal Reserve's goal of achieving its target inflation rate. Although headline CPI could potentially decrease to 3% in June, the task of returning inflation to the desired level becomes increasingly difficult.

Today's release of the US nonfarm payrolls report for June could further reinforce optimism about the US economy. However, there is also a concern that a strong jobs report could lead the Federal Reserve to overestimate the economy's resilience and raise rates more aggressively than necessary. This is reflected in the recent rise in yields, as the market prices in such expectations.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates