Dow and S&P 500 Hit Record Highs Amid Optimism; Fed Remarks Fuel Investor Caution | Daily Market Analysis

Key events:

- USA - Core PCE Price Index (MoM) (Feb)

- USA - Core PCE Price Index (YoY) (Feb)

- USA - Fed Chair Powell Speaks

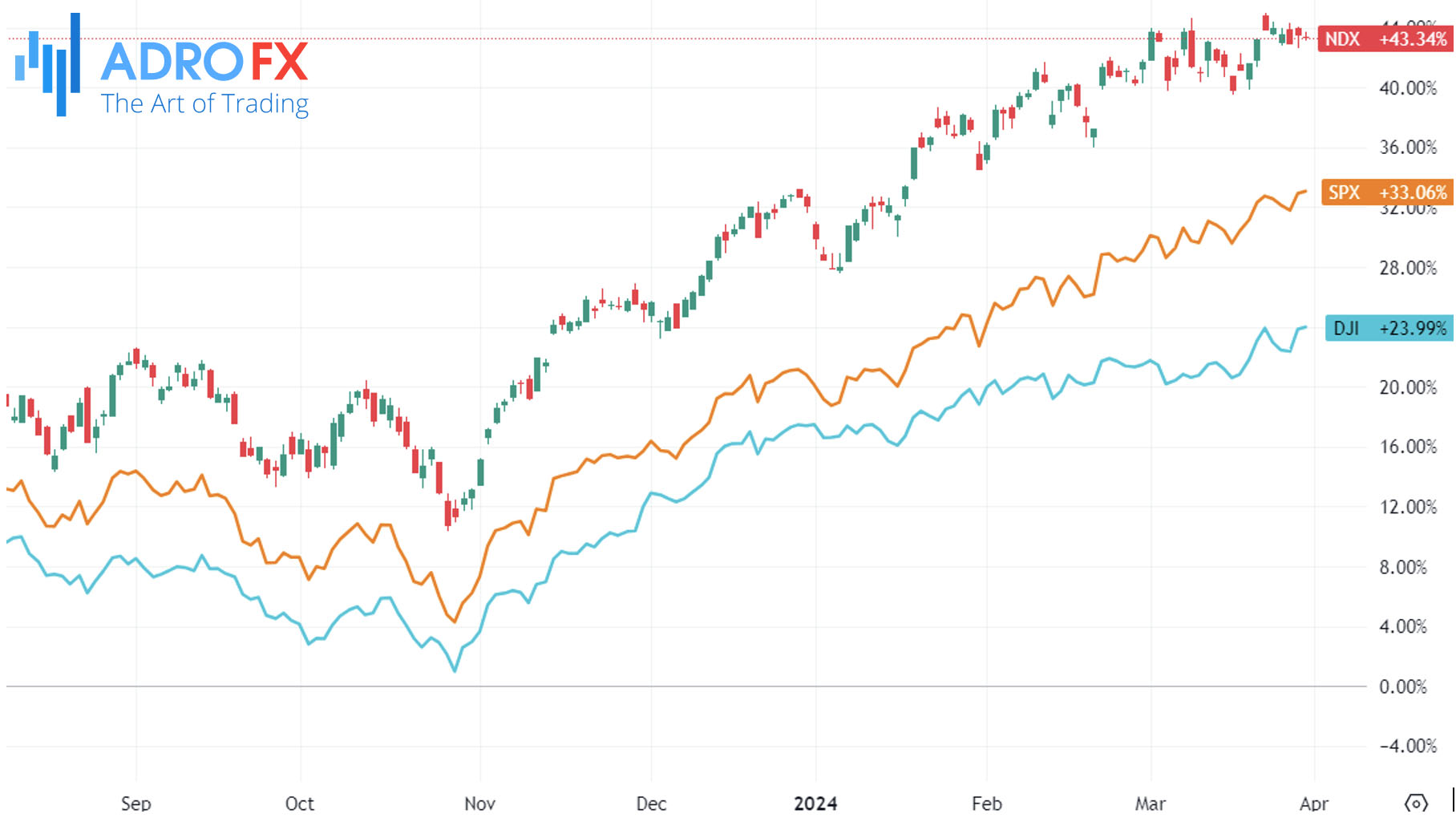

On Thursday, both the Dow and S&P 500 surged to new record highs, marking their strongest first-quarter performance since 2009. This upward momentum extended beyond the tech sector, driven by optimism surrounding potential rate cuts and encouraging economic data suggesting a soft landing for the economy.

The Dow Jones Industrial Average climbed 47 points, or 0.1%, reaching a historic close of 39,807.37. Similarly, the S&P 500 edged up 0.1%, achieving a fresh record close of 5,254.35. However, the NASDAQ Composite experienced a slight dip of 0.2%.

Notably, the S&P 500 saw a robust first-quarter gain of approximately 10%, its most significant increase since 2019, while the Dow posted a nearly 6% rise, marking its best performance since 2021.

Earlier in the day, data revealed that the US economy expanded at a faster pace than previously reported in the fourth quarter. Gross domestic product (GDP) surged at a 3.4% annualized rate, up from the previously announced 3.2%, fueled by upgrades in consumer spending, nonresidential fixed investment, and state and local government spending, all bolstered by a resilient labor market.

Furthermore, a separate report indicated a decrease in initial claims for state unemployment benefits, falling by 2,000 to a seasonally adjusted 210,000 for the week ending March 23.

However, investors faced hesitation in building on the previous session's strong gains following remarks from Fed Governor Christopher Waller at a late Wednesday Economic Club of New York event. Waller emphasized that there was no urgency for the Fed to implement interest rate cuts at present, citing several instances of higher-than-expected inflation in recent months. While Waller acknowledged the likelihood of interest rate cuts later in the year, he noted that the current robustness of the US economy provided ample room for the Fed to maintain higher rates for an extended period.

The Australian Dollar extended its decline for the second consecutive session on Friday, albeit with subdued market activity due to light trading on Good Friday.

The currency faced headwinds following weaker Consumer Inflation Expectations and Retail Sales figures from Australia, raising concerns about potential interest rate cuts by the Reserve Bank of Australia later in 2024. This sentiment was reinforced by Wednesday's release of the softer Australian Monthly Consumer Price Index.

Meanwhile, USD/CAD hovered around 1.3540 during Asian trading hours on Friday, showing signs of potentially ending its four-day losing streak. However, trading volumes remained light due to the holiday.

The Canadian Dollar received a boost from increased prospects of foreign currency inflows, driven by an uptick in WTI oil prices. Expectations of continued production cuts by the Organization of the Petroleum Exporting Countries and its allies (OPEC+) supported the rise in crude oil prices.

Additionally, Canada's Gross Domestic Product (MoM) expanded by 0.6% in January, surpassing expectations and indicating economic resilience. This bolstered confidence in Canada's economic outlook and tempered market expectations of immediate rate cuts by the Bank of Canada.

EUR/USD continued its downward trajectory for the fourth consecutive day, influenced by a stronger US Dollar amid hawkish sentiment surrounding the Federal Reserve and expectations of prolonged higher interest rates. Dovish remarks from European Central Bank policymakers also weighed on the Euro, with concerns about declining core inflation and the possibility of rate cuts.

ECB executive board member Fabio Panetta suggested that the conditions for easing monetary policy are emerging, citing restrictive policies suppressing demand and leading to a swift drop in inflation.

Similarly, the NZD/USD pair remained under selling pressure near 0.5970 after pulling back from the 0.6000 barrier during the Asian session on Friday. Dovish comments from Reserve Bank of New Zealand Governor Adrian Orr, indicating that interest rates may have peaked and cuts could be imminent, weighed on the New Zealand Dollar. Market expectations of rate cuts, potentially as early as August, acted as a headwind for the NZD/USD pair.

Looking ahead, market attention will turn to Friday's release of the Fed's preferred inflation metric, the core PCE, despite the closure of markets for Good Friday. The outcome of the PCE data is expected to significantly influence expectations regarding US interest rates. Additionally, speeches from Fed Chair Jerome Powell and FOMC member Mary Daly are scheduled for Friday, further shaping market sentiment and policy outlooks.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates