August Closes with Upward Momentum in US Equities Amid Anticipation of Employment Report | Daily Market Analysis

Key events:

- USA - Average Hourly Earnings (MoM) (Aug)

- USA - Nonfarm Payrolls (Aug)

- USA - Unemployment Rate (Aug)

- USA - ISM Manufacturing PMI (Aug)

- ISM Manufacturing Prices (Aug)

US equities were on an upward trajectory as August came to a close, bolstered by the anticipation of Friday's employment report for the same month.

Continuing a streak of four consecutive positive sessions, the primary indices of Wall Street concluded Wednesday on a positive note. The Dow Jones Industrial Average, representing established companies, edged up by 0.1%. Meanwhile, the broad-based S&P 500 saw a 0.4% rise, and the technology-focused Nasdaq Composite experienced a 0.5% climb.

However, it is worth noting that these significant benchmarks are still on track to register declines for the month. In August, the DJI and Nasdaq Composite both experienced declines of approximately 2%, while the S&P 500 saw a decrease of 1.4%.

Recent economic indicators, which encompassed a lower-than-expected gross domestic product (GDP) for the second quarter and core inflation data released on Thursday, have instilled optimism among investors. This optimism stems from the possibility that the Federal Reserve might be approaching the conclusion of its interest rate hikes. In July, core inflation, as projected, increased compared to June on an annualized basis. Despite this increase, the numbers remained below the high figures observed the previous year.

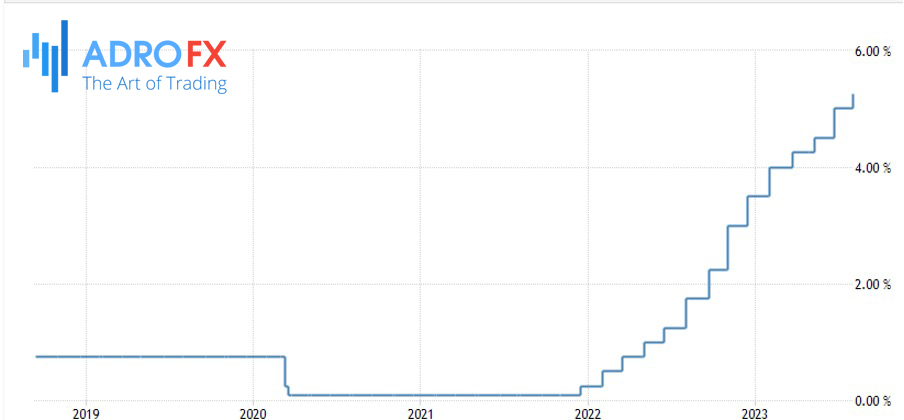

The Federal Reserve, which has emphasized the influence of data on its interest rate decisions, might interpret these reports as signs that their prior actions are beginning to yield effects. Although the objective is to limit inflation to an annual growth rate of 2%, the central bank might choose to delay a rate hike during its September meeting.

Market futures largely reflect expectations of such a pause, with certain futures traders assigning probabilities to a 0.25% increase in November, thus concluding the year.

The impending jobs report for Friday stands as another crucial determinant in the Federal Reserve's decision-making process for the upcoming month. Recent data indicated that job openings were lower than anticipated this week. Moreover, the jobs report is projected to reveal a lower rate of job creation compared to previous months. The Federal Reserve has been actively seeking indicators that suggest the tight labor market is gradually relaxing, a development that would help alleviate inflationary pressures.

Analysts expect the economy created 170,000 jobs last month, down from 187,000 the prior month. Unemployment is expected to stay at 3.5%.

By the way, the ISM manufacturing index is also due out today and is expected to show a reading of 47 compared with 46.4 in the prior reading.

Furthermore, Huw Pill, an economist at the Bank of England, announced his intention to advocate for maintaining rates at 5.25% for an extended duration, countering market expectations. This statement was reported by the Financial Times. Presently, the market anticipates a 50 basis point increase to 5.75%. Pill made these comments while speaking at a conference in South Africa. He endorsed the steadfast approach due to its potential to ensure financial stability, ease the impact on the economy gradually, and effectively transmit higher rates into two- and five-year fixed-rate mortgages, which are common lending instruments for property transactions in the UK.

The situation does not appear to be causing major disruptions. Central banks across the board are echoing similar sentiments – a resolute commitment to curbing inflation, translating into a prolonged period of higher rates, though not necessarily implying constantly escalating rates.

The US Dollar displayed strength against all its counterparts except the Japanese Yen. Recent data on Unemployment benefits in the US indicated a decline to 228,000, surpassing median forecasts that had predicted 236,000.

This decrease marked the lowest reading observed over the past 4 weeks.

The Dollar Index (DXY), a widely used metric to assess the value of the US Dollar against a basket of six major currencies, rebounded to 103.62 from the previous day's value of 103.47.

The Euro (EUR/USD) reversed its upward trend spanning three days, sliding to 1.0840 from the prior level of 1.0880. Notably, the European Central Bank's (ECB) recently released meeting minutes expressed concerns about inflation and highlighted a dimmer growth outlook. Meanwhile, the British Pound (GBP/USD) appreciated against the US Dollar, reaching 1.2670, up from the previous mark of 1.2645.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates