Cooling Inflation Boosts Markets as Fed Rate Cut Looms | Weekly Market Analysis

Key events this week:

Monday, October 27, 2025

- USA - Durable Goods Orders (MoM) (Sep)

- USA - New Home Sales (Sep)

Tuesday, October 28, 2025

- USA - CB Consumer Confidence (Oct)

Wednesday, October 29, 2025

- Canada - BoC Interest Rate Decision

- USA - Crude Oil Inventories

- USA - FOMC Statement

- USA - Fed Interest Rate Decision

- USA - FOMC Press Conference

Thursday, October 30, 2025

- Japan - BoJ Interest Rate Decision

- USA - GDP (QoQ) (Q3)

- Eurozone - Deposit Facility Rate (Oct)

- Eurozone - ECB Interest Rate Decision (Oct)

- Eurozone - ECB Press Conference

Friday, October 31, 2025

- China - Manufacturing PMI (Oct)

- Eurozone - CPI (YoY) (Oct)

- USA - Core PCE Price Index (MoM) (Sep)

- USA - Core PCE Price Index (YoY) (Sep)

- USA - Chicago PMI (Oct)

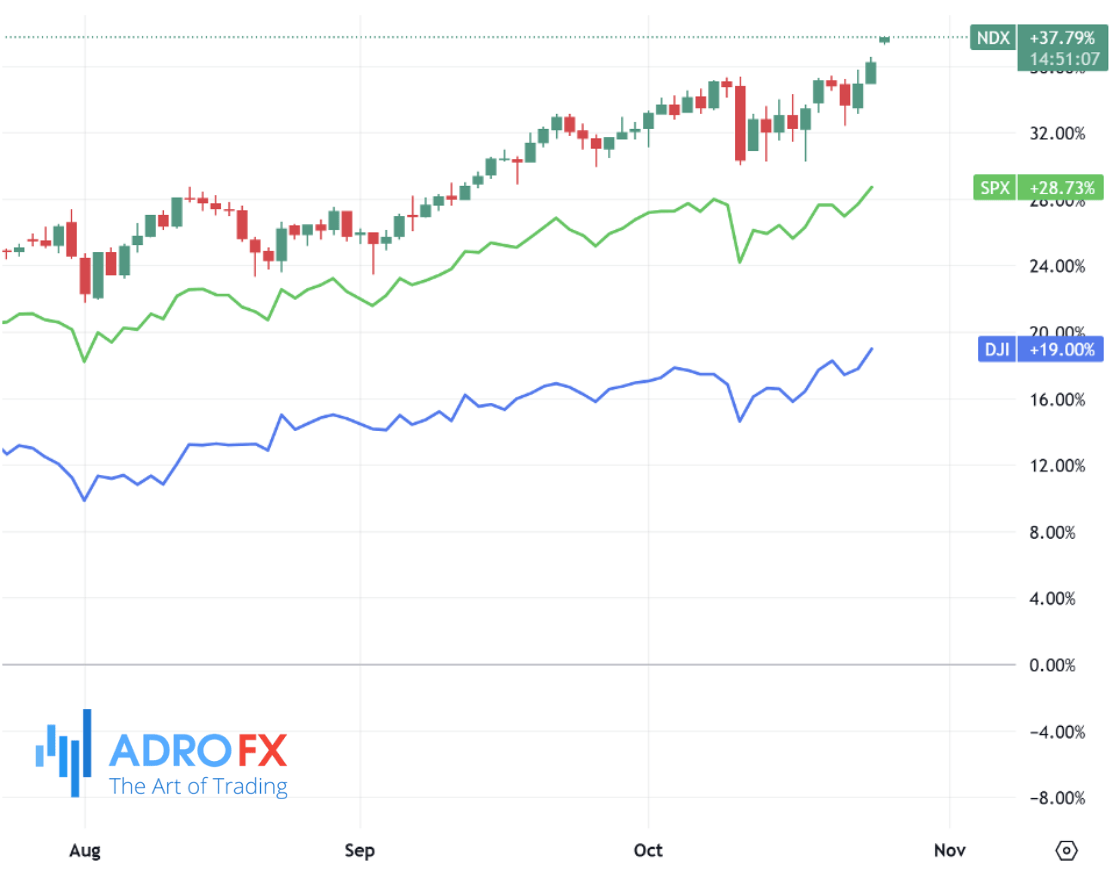

US equity markets surged to fresh highs on Friday, driven by a softer-than-expected inflation reading that has investors increasingly confident the Federal Reserve will reduce interest rates in its upcoming policy meeting. The Dow Jones Industrial Average topped the 47,000 mark for the first time ever, closing at 47,207.12, a gain of 472 points, or roughly 1%. The S&P 500 added 0.8%, while the NASDAQ Composite advanced 1.2%, with all three indexes reaching record intraday and closing levels. Market sentiment was buoyed by data showing inflation pressures remain moderate, providing what traders interpreted as a green light for potential monetary easing.

Data released earlier on Friday revealed that the US Consumer Price Index increased 3.0% year-over-year in September, slightly below forecasts of 3.1%. On a monthly basis, the CPI rose 0.3%, again under analysts’ expectations of 0.4%. Core CPI, which strips out volatile food and energy prices and is closely monitored by the Federal Reserve as an indicator of underlying inflation trends, mirrored these trends, registering 3.0% year-over-year and 0.2% monthly, below anticipated readings of 3.1% and 0.3%. These figures, delayed by the ongoing government shutdown that has disrupted much official economic reporting, carried additional weight as market participants lacked other timely economic data.

Investors responded quickly to the inflation report, interpreting it as evidence that inflation is stabilizing. This perception has fueled expectations that the Fed may move to lower borrowing costs, which would typically provide additional liquidity for financial markets and increase investor risk appetite. Market analysts emphasized that the timing of the CPI release, postponed for more than three weeks due to the government shutdown, amplified its impact, leaving the data as one of the few concrete indicators available to gauge economic momentum.

Corporate earnings also contributed to the positive market sentiment. Intel Corporation reported third-quarter profits that exceeded expectations, reflecting the benefits of substantial cost-cutting measures and strategic investments. The company’s earnings announcement followed significant financial support from Nvidia and Japan’s SoftBank, along with a notable investment from the US government, boosting investor confidence that Intel’s cash position and operational efficiency will remain robust. Shares of Intel jumped sharply after the earnings release, highlighting the market’s favorable reception to both the company’s performance and its strategic partnerships.

In currency markets, the Japanese yen extended a seven-day decline, reaching a two-week low against the US dollar during Monday’s Asian session. Traders cited expectations that Japan’s new Prime Minister, Sanae Takaichi, will continue pursuing expansionary fiscal policies while resisting early monetary tightening. The yen’s decline was further influenced by signs of easing US–China trade tensions, which have encouraged investors to take on riskier assets and reduced demand for traditional safe-haven currencies. Meanwhile, data showing Japan’s service-sector inflation rising for the second consecutive month in September has been insufficient to rally yen bulls, as expectations of a potential rate hike by the Bank of Japan remain tempered by the government’s commitment to fiscal stimulus.

EUR/USD slid to around 1.1620 in early European trading, pressured by political uncertainty in France. Olivier Faure, leader of the Socialist party holding a swing vote in France’s fragmented parliament, threatened to file a no-confidence motion against Prime Minister Sébastien Lecornu’s government if proposed tax measures on the wealthy are not enacted. The euro’s vulnerability in the face of these developments underlined how political factors can weigh on currency valuations even amid broadly stable macroeconomic conditions.

Gold prices traded lower for a second consecutive day, maintaining levels above last week’s swing low but showing limited follow-through selling. Investors appeared less willing to allocate capital to the traditional safe-haven metal as optimism moves into equities and other higher-yielding assets. Nevertheless, ongoing geopolitical uncertainties, including regional tensions and policy unpredictability, continue to support gold’s underlying appeal for some market participants.

The Australian dollar weakened slightly against the US dollar after an early gap-up at the start of the week. Market participants are closely watching Australia’s upcoming Q3 economic figures and the September inflation release, which are expected to guide the Reserve Bank of Australia’s policy stance. The AUD remains sensitive to shifts in China’s economic trajectory, given the deep trade ties between the two nations. Expectations that the RBA may reduce rates following a higher-than-anticipated unemployment figure have also pressured the currency. Futures markets indicate a roughly 67% likelihood of a rate cut to 3.35% at the next policy meeting, highlighting the market’s sensitivity to domestic labor data.

USD/CHF opened with a gap higher but retraced some losses during Asian trading hours, trading around 0.7960. The Swiss franc has benefited from diminished expectations of further easing by the Swiss National Bank. Minutes from the SNB’s September policy meeting indicated that the bank views deflation risks as limited and does not plan to return to negative rates, while still maintaining an expansionary policy stance to allow previous easing measures to take full effect.

USD/CAD also declined slightly after a period of limited gains, trading near 1.3980. President Donald Trump announced an additional 10% tariff on Canadian imports following an advertisement by Ontario that aired during the World Series, which he viewed as misleading. This move came shortly after halting trade talks with Ottawa, reflecting ongoing trade tensions between the two North American neighbors and reinforcing volatility in the USD/CAD pair.

Meanwhile, the New Zealand dollar showed modest gains, moving toward 0.5770 against the US dollar in early Asian trading. The Reserve Bank of New Zealand surprised markets by cutting the Official Cash Rate by 50 basis points to 2.5% during its October meeting, exceeding expectations. The central bank signaled that further easing could be implemented if necessary to support economic growth and achieve its inflation target, keeping traders attentive to potential future policy shifts.

Taken together, the combination of benign inflation data, strong corporate earnings, and mixed central bank signals has created a supportive environment for risk assets, while leaving currency and commodity markets more reactive to both domestic and international developments. The Dow’s historic move above 47,000 serves as a milestone not only for investors tracking equity indices but also as a reflection of the broader market’s confidence in a moderate inflation trajectory and the possibility of imminent rate cuts by the Federal Reserve.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates