Markets React to Weak Consumer Confidence and Global Economic Shifts | Daily Market Analysis

Key events:

- USA - Crude Oil Inventories

- USA - New Home Sales (Jan)

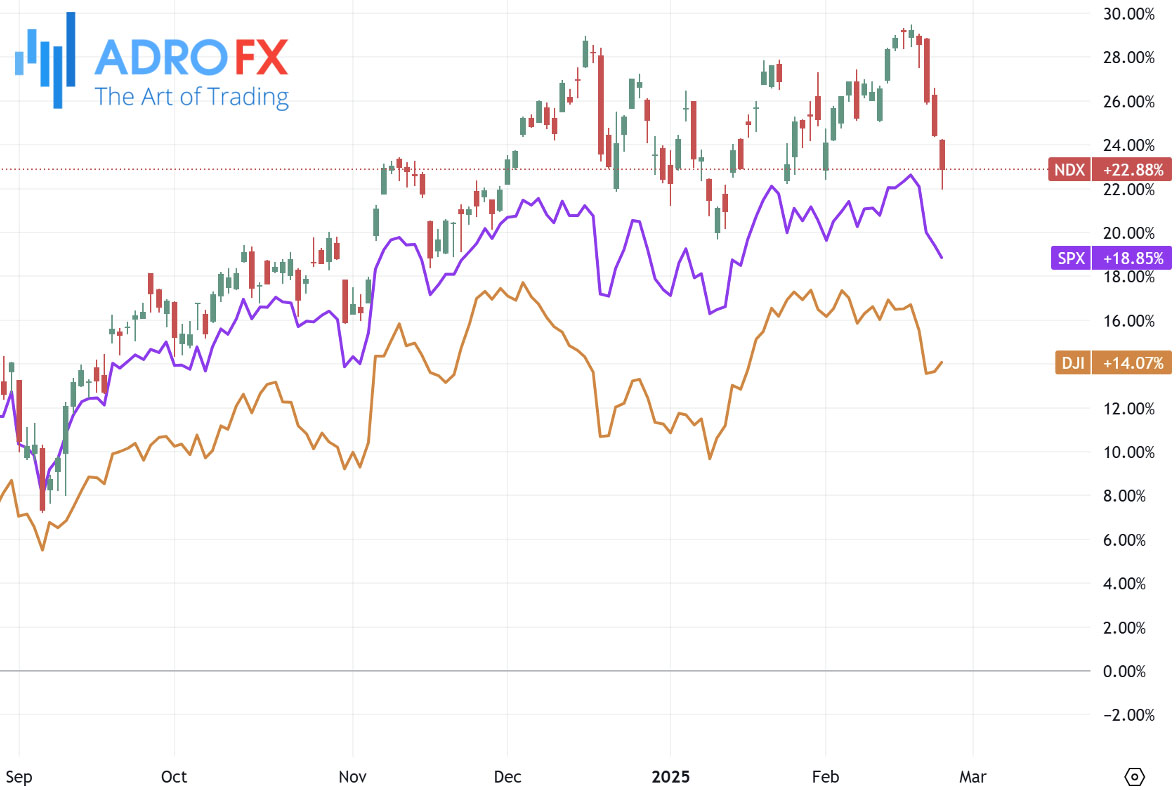

The S&P 500 extended its losses for a second consecutive session on Tuesday as investor sentiment weakened following a sharp decline in consumer confidence. The Conference Board’s latest report showed consumer confidence dropped by seven points in February to 98.3, marking its steepest fall since August 2021. This fueled concerns about the economy just ahead of Nvidia’s (NASDAQ: NVDA) crucial earnings release later this week.

Despite overall market volatility, the Dow Jones Industrial Average managed to gain 160 points (0.4%), while the benchmark S&P 500 dipped 0.5%. The Nasdaq Composite, heavily weighted toward technology stocks, suffered the most, declining by 1.4%.

In currency markets, the EUR/USD pair retreated from its recent gains, slipping to around 1.0500 in early Asian trading on Wednesday. The Euro faced selling pressure as the US Dollar strengthened, supported by rising US Treasury yields.

The US Dollar Index climbed toward 106.50. Simultaneously, US Treasury yields moved higher, with the 2-year and 10-year notes rising to 4.12% and 4.32%, respectively. Despite this, the USD’s rally was tempered by weakening US economic data, which suggested potential headwinds for growth.

Investor attention remains focused on Federal Reserve policy, with Richmond Fed President Thomas Barkin predicting another decline in the Personal Consumption Expenditures inflation index later this week. While he acknowledged the Fed’s progress in controlling inflation, Barkin cautioned that economic uncertainty warranted a patient, data-driven approach before making further policy adjustments.

The Euro, meanwhile, found support from optimism surrounding potential fiscal stimulus in Germany. Reports indicate that Europe’s largest economy is considering a €200 billion emergency defense fund, which could boost government spending and stimulate economic activity. Additionally, Christian Democratic Union (CDU) leader and Germany’s incoming chancellor, Frederich Merz, hinted at possible reforms to the country’s strict debt brake, which could pave the way for tax cuts, lower energy prices, and increased military spending.

As investors awaited next week’s European Central Bank policy meeting, ECB policymakers provided mixed signals on the future direction of interest rates. Joachim Nagel suggested further rate cuts could be possible if inflation continues to decline toward the 2% target. In contrast, Isabel Schnabel warned that the ECB might be nearing a pause in its rate-cutting cycle, indicating that the bank would carefully assess incoming economic data before making further adjustments.

In the Asia-Pacific region, the Australian Dollar remained under pressure against the US Dollar for the fourth consecutive day. The AUD/USD pair struggled to find upside momentum after Australia’s monthly Consumer Price Index data showed a 2.5% year-over-year rise in January, unchanged from December’s reading and slightly below market expectations of 2.6%. The lack of stronger inflationary pressure reduced the likelihood of aggressive monetary tightening by the Reserve Bank of Australia, contributing to the AUD’s weakness.

China also remained in focus as its Commerce Ministry announced a meeting between International Trade Representative and Vice Minister of Commerce Wang Shouwen and US business leaders. The discussions primarily revolved around trade and tariffs, though no specific outcomes were disclosed.

Elsewhere, the USD/JPY pair rebounded to around 149.30 during Asian trading hours on Wednesday. However, rising expectations of interest rate hikes by the Bank of Japan and a broader risk-off sentiment could support the Japanese Yen and limit further upside for the pair.

The BoJ is expected to raise interest rates from 0.50% to 0.75% in 2024, with markets fully pricing in a rate hike by September. Bloomberg data suggests that there is a 50% probability of a rate increase as early as June. Japan’s latest Services Producer Pricing Index data, alongside persistently high consumer inflation figures, supports the case for further BoJ tightening, reinforcing the JPY’s strength.

Meanwhile, GBP/USD edged higher on Tuesday, pushing the pair toward the upper end of its recent trading range while holding close to the 200-day EMA. Despite weaker consumer sentiment, the British Pound maintained a bullish tone as traders positioned themselves ahead of key economic data.

Looking ahead, Wednesday’s economic calendar remains relatively light for both the US and UK, but investors are closely watching Thursday’s US Gross Domestic Product report. A strong GDP reading could reinforce expectations of tighter monetary policy from the Federal Reserve, while a weaker report could increase speculation about potential rate cuts later in the year.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates