Rally in Tech Stocks Ahead of Key Earnings Pushes Dow to Four-Week High | Daily Market Analysis

The Dow surged on Friday, marking its fourth consecutive weekly gain, buoyed by strong corporate earnings and data indicating cooling inflation, which fueled optimism for an upcoming interest rate cut.

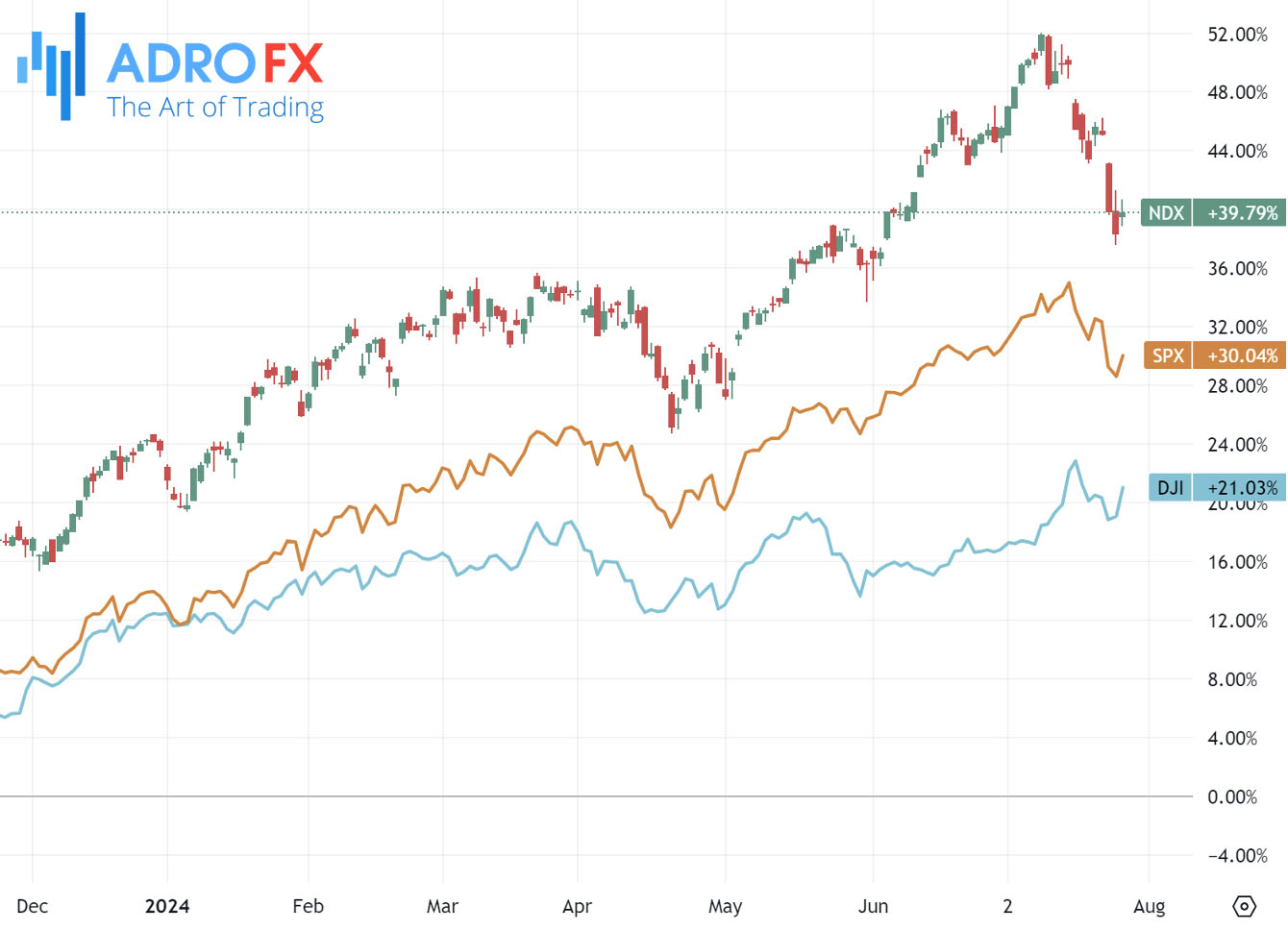

The Dow Jones Industrial Average climbed 654 points, or 1.6%. Both the S&P 500 and NASDAQ Composite rose 1.1%, though the latter two indexes recorded their first back-to-back weekly losses since April.

Optimism about rate cuts led to lower Treasury yields, which in turn spurred a rally in tech stocks following their recent slump.

This dip-buying activity occurs just before the upcoming earnings reports from major tech companies, including Microsoft and Apple, scheduled for Tuesday and Thursday, respectively.

Microsoft's results are expected to be closely watched as investors seek further indications that the tech giant's cloud division, Azure, is benefiting from the growing interest in AI.

3M Company stock surged nearly 23% to record highs after the industrial conglomerate raised the lower end of its full-year adjusted profit forecast, anticipating gains from restructuring efforts and increased demand for electronics.

Gold prices experienced some positive traction during the Asian session on Monday but struggled to maintain momentum beyond the $2,400 mark. The prevailing risk-on sentiment in global equity markets has created headwinds for the safe-haven metal. Nonetheless, significant declines remain limited due to growing expectations that the Federal Reserve will begin cutting interest rates in September.

Additionally, geopolitical tensions in the Middle East are likely to benefit the safe-haven appeal of XAU/USD.

The Japanese Yen is continuing to appreciate on Monday as traders show caution ahead of the Bank of Japan's policy meeting on Wednesday, where a rate hike is possible. Market predictions suggest the BoJ could increase rates by 10 basis points to 0.1% and may announce plans to taper bond purchases.

Additionally, the JPY may be bolstered as traders unwind their carry trades in anticipation of the BoJ's decision. Japan's chief currency diplomat, Masato Kanda, informed the G20 on Friday about the negative impact of FX volatility on Japan's economy. Kanda emphasized the increased likelihood of a soft economic landing and the necessity of vigilant economic monitoring and necessary measures, as reported by Reuters.

Meanwhile, the Australian Dollar is extending its gains against the US Dollar for a second consecutive session on Monday. This rise is driven by the hawkish outlook on the Reserve Bank of Australia’s policy. Unlike other central banks, the RBA is expected to maintain its policy tightening due to ongoing inflationary pressures and a robust labor market.

Key economic data are on the horizon for Australia, with June Retail Sales figures to be released on Tuesday and the second-quarter Consumer Price Index data on Wednesday. These reports are expected to provide insights into future monetary policy directions. Some economists are warning of the risks of continued tightening amid recessionary pressures. Recent data indicated a slowdown in private sector growth in Australia in July, with manufacturing activity contracting and the services sector's growth decelerating.

The AUD/USD pair is gaining ground partly due to a weaker US Dollar, influenced by signs of cooling inflation and easing labor market conditions in the US, which have spurred expectations of three rate cuts by the Federal Reserve this year, starting in September.

The NZD/USD pair is attracting some dip-buyers near the 0.5880 level during the Asian session on Monday, despite a lack of strong bullish momentum. The pair is trading around the 0.5900 mark, close to its lowest level since early May, touched last Thursday.

Friday's US Personal Consumption Expenditures Price Index data added to signs of easing inflation pressures and strengthened expectations that the Federal Reserve will start cutting interest rates in December. This has led to US Treasury bond yields dropping to a near two-week low, along with a risk-on market sentiment, putting pressure on USD bulls and providing some support to the NZD/USD pair.

However, ongoing concerns about a slowdown in China's economy - the world's second-largest - may continue to challenge antipodean currencies, including the Kiwi. Additionally, expectations for an early rate cut by the Reserve Bank of New Zealand, supported by last week’s weaker CPI data, are also limiting the NZD/USD pair’s gains. Hence, caution is advised before betting on further intraday gains.

Traders are likely to avoid making significant directional bets ahead of the two-day FOMC policy meeting concluding on Wednesday. The much-anticipated Fed decision, along with crucial US macroeconomic data releases at the start of the new month, including the nonfarm payrolls report, will significantly influence near-term USD price movements.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates