S&P 500 Closes Lower Amid Tech Slide and Fed Rate Concerns | Daily Market Analysis

Key events:

- USA - Initial Jobless Claims

- USA - Philadelphia Fed Manufacturing Index (Apr)

- USA - Existing Home Sales (Mar)

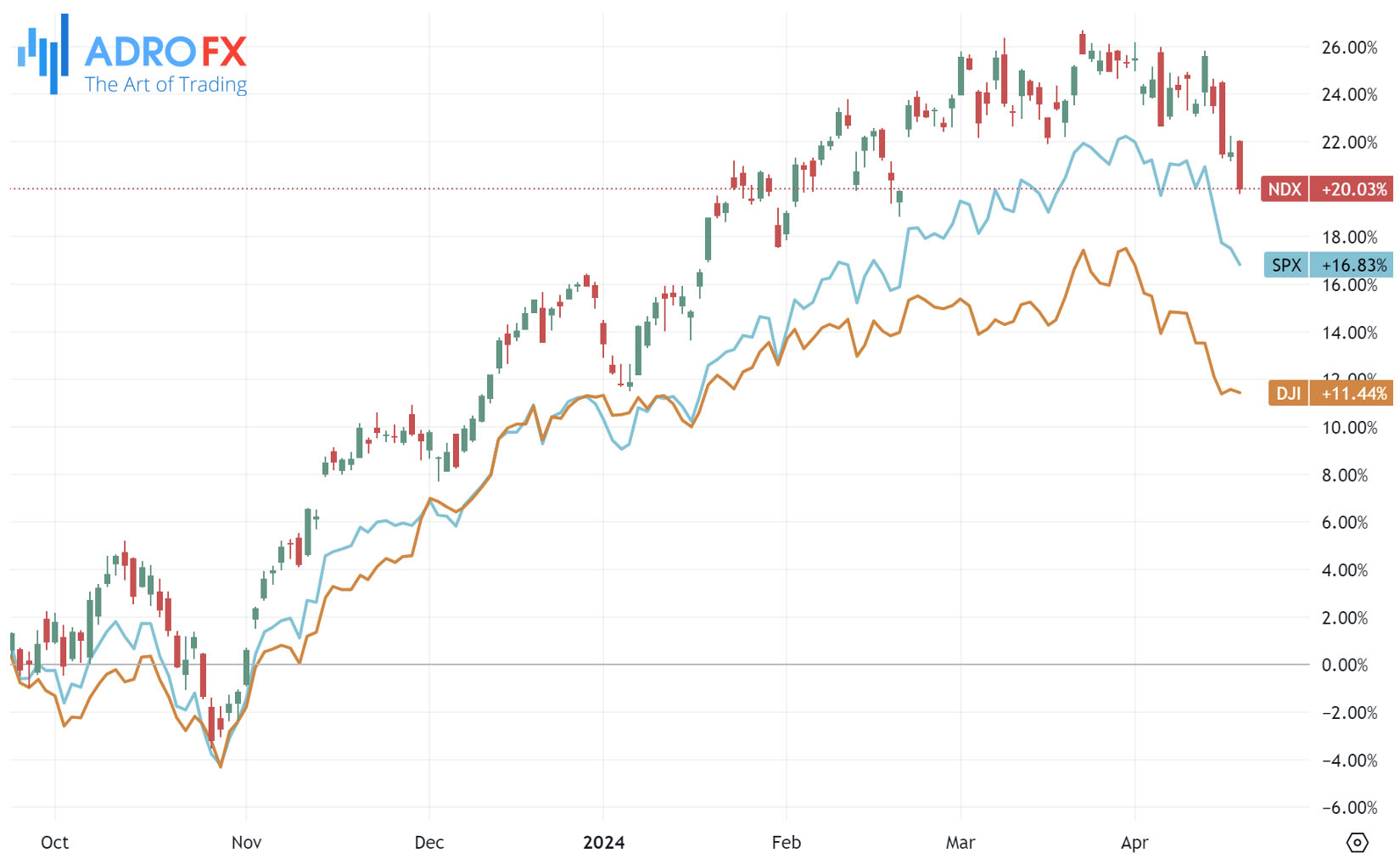

Wednesday saw the S&P 500 finishing lower, as concerns over prolonged Federal Reserve interest rates weighed heavily on tech stocks, led by Nvidia's decline.

The Dow Jones Industrial Average dipped by 45 points, equivalent to a 0.1% decrease, while the S&P 500 experienced a 0.6% decline, and the NASDAQ Composite fell by 1.2%.

US stock markets grappled with uncertainty throughout the day, following cautious remarks from Federal Reserve officials. The S&P 500 is currently enduring its lengthiest non-bullish phase in months, sparking speculation about a potential shift in market sentiment despite the ongoing upward trend witnessed in 2024.

The current market performance positions us approximately 5% below recent highs, suggesting that we are midway toward meeting the criteria for an official correction. This underscores the importance of closely monitoring market dynamics and potential shifts in sentiment going forward.

Recent market fluctuations have been attributed by some investors to geopolitical tensions, including heightened war risk premiums and concerns about rising oil prices, which have disrupted the earlier narrative of deflationary pressures.

However, a more likely scenario is that equities are adjusting to the Federal Reserve's less dovish monetary policy stance and broader interest rate dynamics. Over the past trading week, there has been a collective reassessment of the possibility of Fed rate cuts, with discussions centering on a higher terminal rate. This adjustment effectively sets a more elevated implied floor for market discount rates, impacting the rest of the yield curve and providing a less bullish outlook for stocks.

During a trilateral meeting on Wednesday, financial leaders from the United States, Japan, and South Korea pledged to "consult closely" on FX markets, addressing concerns about recent sharp declines in their currencies, particularly the yen. This agreement coincides with diminishing expectations for an immediate US interest rate cut, contributing to the yen's decline to 34-year lows and fueling speculation about potential intervention by Japanese authorities to buy the yen.

Thursday witnessed the Australian Dollar continuing its rally for the second consecutive day, buoyed by a weakening US Dollar that lends support to the AUD/USD pair. However, the AUD faces downward pressure due to mixed Australian employment data.

The AUD gains ground as the ASX 200 Index maintains its upward trajectory on Thursday, fueled by gains in mining stocks supported by robust metals prices. This positive momentum persists despite overnight declines in US stocks, driven by concerns over potential delays in Federal Reserve (Fed) rate cuts.

The US Dollar Index retreats, primarily influenced by subdued US Treasury yields. This decline in the US Dollar is further accentuated by renewed selling pressure and an overall market sentiment favoring riskier assets.

Meanwhile, the GBP/USD pair trades lower around 1.2450 during early Asian trading hours on Thursday. Weaker UK inflation data raises expectations of upcoming interest rate cuts by the Bank of England, weighing on the Pound Sterling against the Greenback. Investors eagerly await cues from US weekly Initial Jobless Claims, the Philly Fed Manufacturing Index, the CB Leading Index, and Existing Home Sales, scheduled for Thursday.

The BoE hints at a potential interest rate cut for the UK, with recent data indicating a slowdown in economic price growth. According to the Office for National Statistics (ONS), UK CPI inflation dropped to 3.2% in the 12 months to March, the lowest level in two-and-a-half years, down from the previous reading of 3.4%. Despite this, investors anticipate the first rate cut in August or September, as per LSEG data.

Investors eagerly await the release of weekly Initial Jobless Claims and Existing Home Sales later on Thursday, seeking further insights into the state of the US economy, which could potentially influence the trajectory of the US Dollar and other major currencies.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates