Will There Be a Recession in the US Next Year? | Daily Market Analysis

Key events:

- Eurozone – CPI (YoY) (Nov)

- USA – ADP Nonfarm Employment Change (Nov)

- USA – GDP (QoQ) (Q3)

- USA – JOLTs Job Openings (Oct)

- USA – Pending Home Sales (MoM) (Oct)

- USA – Crude Oil Inventories

- USA – Fed Chair Powell Speaks

Many are wondering today if the U.S. will have a recession, or if can it still be avoided. Well, we will not get the CPI from the Bureau of Labor Statistics until December 13, and the next day the Fed's rate decision will be announced. The Fed supposedly does not care about the CPI, preferring the PCE, though it can hardly ignore the CPI entirely as markets react to it.

Depending on which indicator you use, you can make almost any forecast. Make your choice:

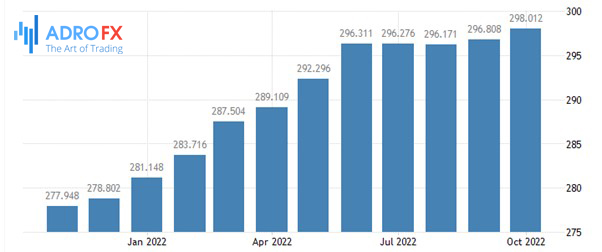

- The CPI was 7.7% YoY in October (from 8.2% in September), the 4th consecutive decline and the lowest since January. Housing accounted for more than half of the inflation;

- The Cleveland Fed's weighted average consumer price index was slightly lower at 6.95% in October, down from 7.31 in September.

The Personal Consumption Expenditures Price Index was 6.2% y/y in September, the same as in August, and the core PCE was 5.1%, up from 4.9% a month earlier. The Fed usually refers to the core PCE, although the Fed's website says the primary PCE, doesn't matter.

So we have a range of numbers from 5.1% to 6.2%, 6.95% to 7.7%. One idea is that if the core PCE is lower, the market will go back to a dovish position/possibly take a pause, and if it is higher by more than one point, the market will get nervous and start evaluating more increases, bigger increases, and longer increases. A weak underlying PCE price index negatively affects the dollar and a strong one positively, which is silly and unreasonable given that the U.S. will end up having the highest rate in the G20.

The market has three problems: to fall for one single opinion and then be surprised when it turns out to be wrong. Second, believing that one data point can or should drive currencies longer than a day or two. This is useful for traders in ultra-low time frames, but it is still a poor analysis.

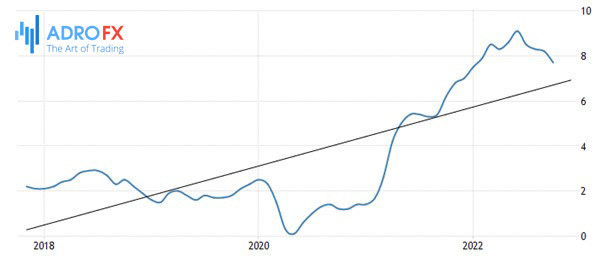

Finally, the ancient fallacy of post hoc, ergo propter hoc. It means "after this, because of that," where correlation is not causation until proven. The crowing of a rooster does not cause the sun to rise. Falling core PCE does not cause the Fed to cut the next rate hike to 50 bps, when the Fed has said several times that it is thinking about 50 bps for a bunch of reasons, none of which are related to PCE this time. The PCE trend is possible but look at the charts. We don't have a downward trend on any of them. And that raises the question of how many falling inflation numbers the Fed has to see to make sure inflation is down. No one knows, and the main measure of inflation, whether CPI or PCE, is hardly the only determinant. It is not a single number.

The Fed's recent comments have failed to move expectations toward a higher endpoint. Those expecting 5-5.25% by the December 14 meeting are now 38.6%, but it was 40.2% yesterday and 42% a week ago. How do you explain this refusal to accept Fed statements that couldn't be clearer? The ruling idea is that there will be a severe recession in the U.S. next year - witness the deepening inversion of the yield curve - and the Fed will change its mind. That, of course, is one option, but it is not the only one.

Betting on a recession seems to have been the main way to compensate for the risk aversion coming from China and even Musk, and explains why the dollar has failed to hold its gains. The U.S. stock market recovery is also contributing. It remains to be seen whether the indictment of Chinese officials will work, but it also seems unrealistic to imagine that the coronavirus crisis is over. The Australian dollar may continue to be the canary in the coal mine. Meanwhile, the emerging market economy (Mexico) is thriving.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates