Wall Street Ends Positively Amid 3M and Goldman Sachs Advances Ahead of Key Data Releases | Daily Market Analysis

Key events:

- USA - CB Consumer Confidence (Aug)

- USA - JOLTs Job Openings (Jul)

On Monday, Wall Street concluded on a positive note, driven by advancements in 3M and Goldman Sachs, just ahead of significant inflation and jobs data scheduled for release this week. This data holds the potential to provide greater insights into the future direction of the Federal Reserve's interest rates.

In particular, 3M experienced a notable surge of 5.2% following reports indicating that the conglomerate has tentatively agreed to settle over 300,000 lawsuits related to the sale of defective combat earplugs to the US military. The settlement amount is reportedly exceeding $5.5 billion.

Goldman Sachs also witnessed a rise of 1.8% in its stock value. This increase followed the bank's decision to offload an investment advisory division to Creative Planning LLC, a wealth management firm, as part of a recently reached agreement.

All three major stock indices recorded upward movement as investors assimilated the remarks made by Fed Chair Jerome Powell last Friday. The statements underscore the cautious approach taken by Powell and fellow Federal Reserve officials as they navigate the intricacies of monetary policy adjustments. Their aim is to rein in rising prices without triggering a destabilizing impact on the broader economy.

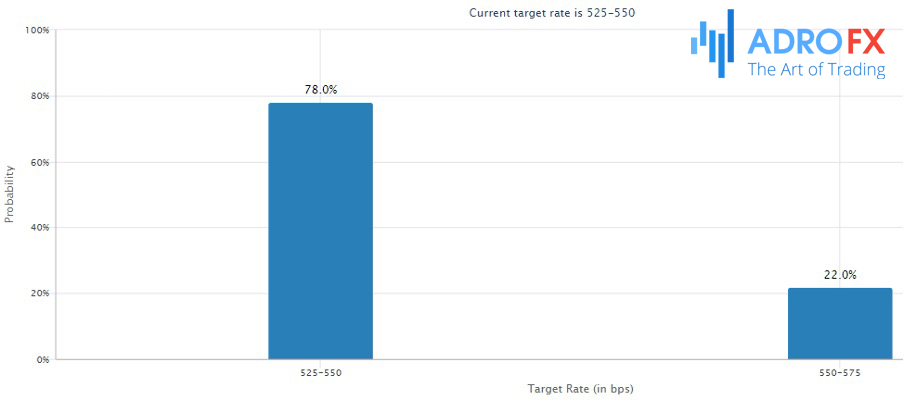

According to the CME`s Fed Watch Tool, there is an almost 80% likelihood that the Federal Reserve will keep borrowing costs within the range of 5.25% to 5.50% during its upcoming meeting in September. Meanwhile, the probability of a 0.25 percentage point increase in rates at the November gathering hovers just below 50%, marking an increase from around 35% in the previous week.

The forthcoming release of the personal consumption expenditure index, the Fed's preferred metric for gauging price growth, on Thursday, will provide the central bank with an opportunity to assess the trajectory of inflation.

Additionally, policymakers will meticulously analyze the nonfarm payrolls report for August, scheduled for release on Friday. Economists' projections indicate an estimated addition of 170,000 jobs in the US during the month, a decrease from the 187,000 added in July. Concurrently, the unemployment rate is anticipated to remain stable at 3.5%. Such an outcome could suggest that the Fed's series of rate hikes might be impacting employers' demand for labor, despite the overall labor market retaining its tight characteristics.

While the US Dollar (USD) exhibited relative weakness against the majority of G10 currencies, its behavior diverged when contrasted with the Japanese Yen (JPY). In this context, the JPY's movement was influenced by the prevalent risk-on sentiment within the trading landscape, further influenced by the elevated short-term yields of US Treasury bonds.

Among the array of currencies, the Australian Dollar (AUD) emerged as the frontrunner in terms of gaining ground against the USD. The AUD's notable strengthening can be attributed to a confluence of factors. One contributing factor was the supportive actions taken by Chinese authorities to fortify their domestic equity market. Furthermore, robust retail sales data originating from Australia also contributed to enhancing the AUD's performance in relation to the USD. The interplay of these favorable conditions culminated in a significant appreciation of the Australian Dollar within the currency markets.

Throughout the month of August, the EUR/USD currency pair has found itself ensnared in the consequences of a resurgent USD. Alongside the broader movements of the USD against various currencies, a steady stream of unfavorable news pertaining to the Euro (EUR) has contributed significantly to this unfolding pattern.

Particularly noteworthy is the continuous decline in economic data originating from the Eurozone, intensifying apprehensions surrounding the trajectory of the region's primary economy, Germany, which is undergoing a swift downturn. This deterioration has spurred investors to reevaluate their assumptions regarding upcoming interest rate hikes by the European Central Bank (ECB). Consequently, the prevailing sentiment has shifted, no longer harboring expectations of any further rate hikes at the present moment.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates