Wall Street Banks' Earnings Fuel Dow's Friday Plunge While Gold Rises Amid Middle East Tensions | Daily Market Analysis

Key events:

- Eurorzone - ECB's Lane Speaks

- USA - Core Retail Sales (MoM) (Mar)

- USA - FOMC Member Williams Speaks

- USA - Retail Sales (MoM) (Mar)

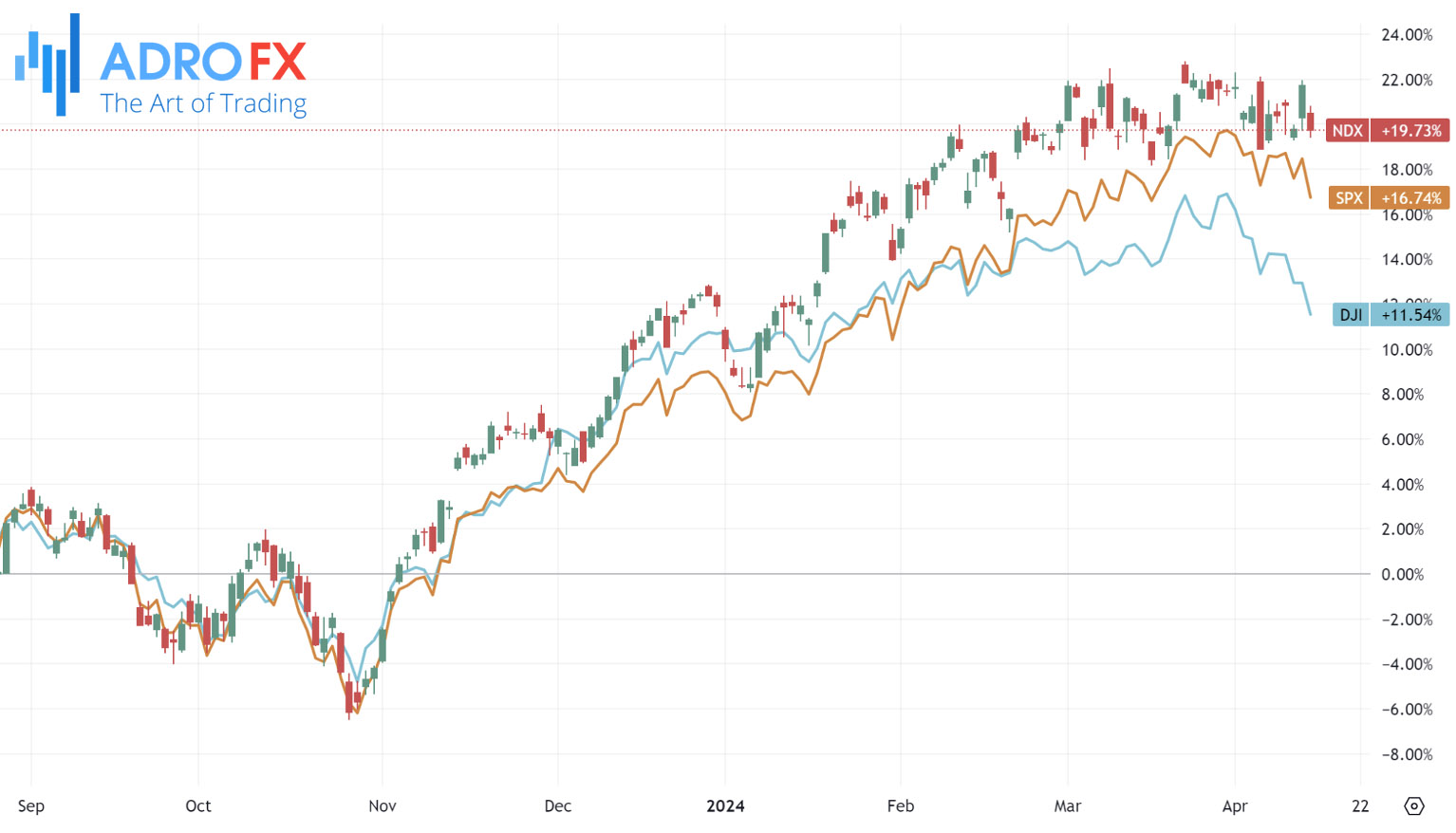

Friday witnessed a significant downturn in the Dow, triggered by disappointing results from major Wall Street banks as they initiated the earnings season. This fueled concerns about the upcoming earnings period's robustness, particularly amidst prevailing inflation concerns. The Dow Jones Industrial Average plummeted by 475 points, equating to a 1.2% decrease, while the S&P 500 and NASDAQ Composite experienced declines of 1.5% and 1.6%, respectively.

JPMorgan Chase (NYSE: JPM) shares took a nosedive of over 6% after the banking titan projected full-year interest income below market expectations, anticipating forthcoming Federal Reserve rate adjustments. Although Wells Fargo (NYSE: WFC) surpassed revenue forecasts, its stock slipped by 0.3% due to weaker-than-anticipated net interest income figures.

Similarly, Citigroup Inc (NYSE: C) witnessed a decline exceeding 2%, despite reporting quarterly results surpassing both revenue and earnings estimates, signaling progress in its restructuring endeavors. Given the banking sector's role as a barometer for overall economic health, uncertainty surrounding the Federal Reserve's interest rate stance is poised to linger throughout the first-quarter earnings period. Analysts foresee a 5% year-over-year increase in earnings for S&P 500 companies collectively in the first quarter, a notable decline from the 10.1% growth witnessed in the fourth quarter of 2023, according to LSEG data.

Gold prices, represented by XAU/USD, experienced a slight uptick at the start of the new week, halting its retreat from a recent peak of around $2,431-2,432 achieved last Friday. The surge was fueled by heightened tensions in the Middle East following Iran's attack on Israel over the weekend, bolstering the appeal of the traditional safe-haven asset. Additionally, the subdued performance of the US Dollar further supported gold prices.

Conversely, the US Dollar remained resilient amid expectations that the Federal Reserve may delay interest rate cuts due to persistent inflationary pressures. This hawkish outlook maintained elevated US Treasury bond yields, thereby limiting further gains for gold, which does not yield interest. Traders are now monitoring US macroeconomic data releases and Federal Reserve commentary for direction during the North American trading session.

During Monday's Asian session, the EUR/USD pair inched up towards the 1.0650 level, rebounding from a five-month low of 1.0622 recorded on Friday. The ascent came amidst a backdrop of increased dollar-buying driven by geopolitical tensions, exerting downward pressure on the EUR/USD pair. The European Central Bank and the Federal Reserve presented differing monetary policy outlooks, contributing to the downward momentum of the EUR/USD pair. The ECB hinted at potential policy rate cuts in June if underlying inflation continues to decelerate as anticipated.

In contrast, robust US inflation and positive macroeconomic indicators are prompting the Fed to reassess its stance on monetary easing. The likelihood of interest rates remaining unchanged at the June meeting has risen to 63.5% according to the CME FedWatch Tool, up from 46.8% the previous week. Market participants are closely monitoring Eurozone Industrial Production data and US Retail Sales figures for further insights. Boston Federal Reserve President Susan Collins commented on Friday, suggesting the possibility of 'around two' rate cuts for 2024 while anticipating a moderation in inflation pressures later in the year. However, she underscored the uncertainty surrounding the timing of potential rate adjustments, highlighting that while a rate hike is not currently part of the baseline scenario, it cannot be entirely discounted.

In the Asian session, the Japanese Yen faced renewed selling pressure, reaching multi-decade lows against the US Dollar. The Bank of Japan provided little guidance on future interest rate hikes, while expectations of rate cuts by the Federal Reserve in September widened the interest rate differential between the two currencies. Japanese authorities' warnings of potential market intervention to support the yen had limited impact amid ongoing geopolitical tensions in the Middle East.

The USD/CAD pair experienced selling pressure, retracting slightly from Friday's highs. Despite concerns over potential disruptions to oil supply from the Middle East following Iran's actions, crude oil prices struggled to attract buyers, which could limit downside pressure on the commodity-linked Canadian Dollar.

Looking ahead, market participants are eyeing US economic indicators such as Retail Sales and the Empire State Manufacturing Index, along with Federal Reserve communications and overall risk sentiment, to gauge USD demand moving forward.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates