US Equities Recover as Fed Maintains Rates, EUR/USD Climbs Amid Powell's Dovish Remarks | Daily Market Analysis

Key events:

- USA - Initial Jobless Claims

- Eurozone - HCOB Eurozone Manufacturing PMI (Apr)

- Eurozone - ECB's Lane Speaks

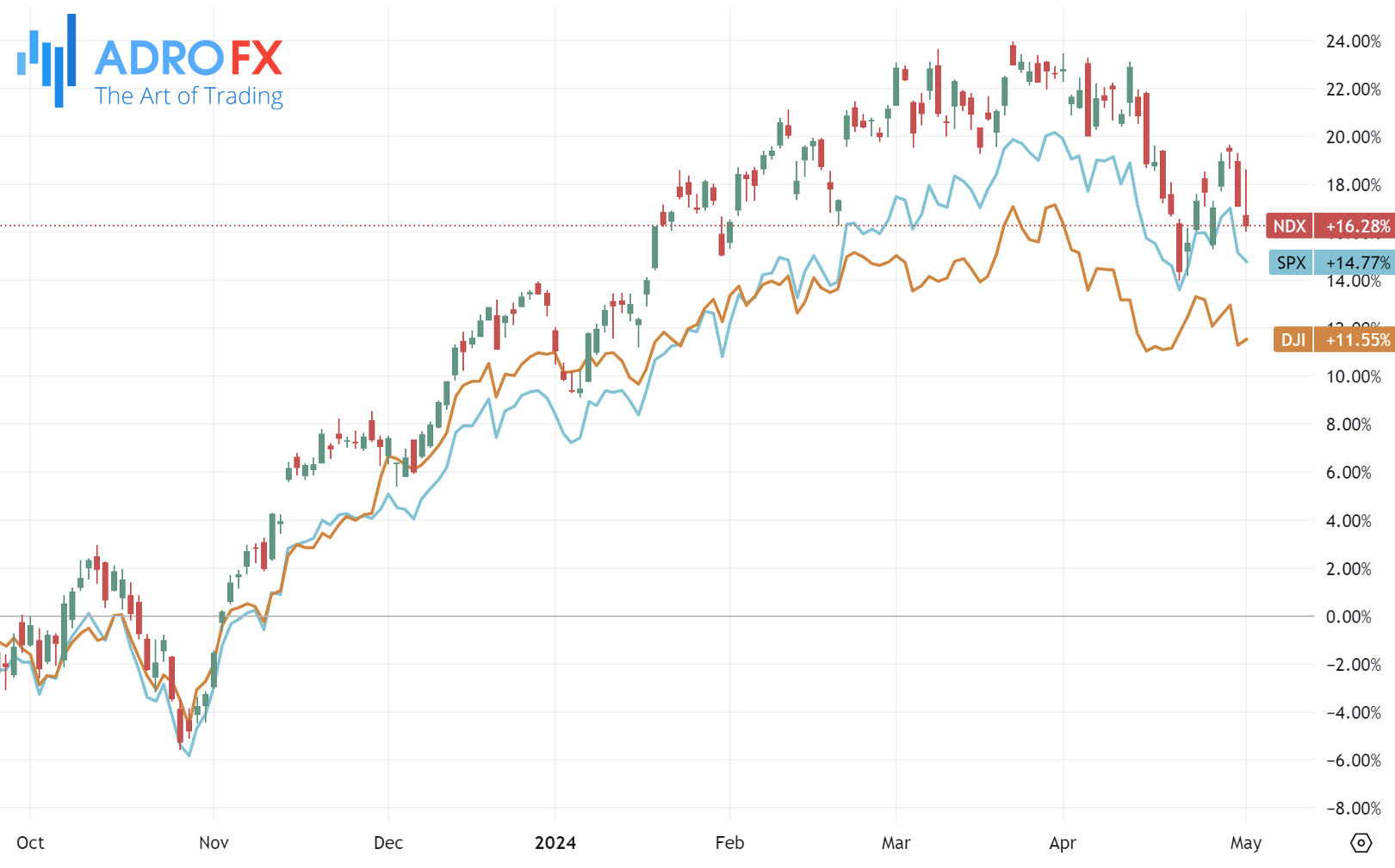

US equities pared some of their losses following the Federal Reserve's decision to keep interest rates unchanged on Wednesday and announced plans to gradually reduce the pace of its balance sheet reduction program, known as quantitative tightening, starting next month.

The S&P 500 inched up by 0.1%, the NASDAQ Composite gained 0.2%, and the Dow Jones Industrial Average surged by 179 points, or 0.50%.

The Federal Reserve maintained its benchmark interest rates within the range of 5.25% to 5.5% and hinted that rates might stay elevated for a longer duration than previously anticipated due to sluggish progress in curbing inflation.

According to the Federal Open Market Committee, there has been insufficient advancement toward achieving the committee's 2 percent inflation target in recent months.

However, the FOMC announced that starting from June, the Fed would reduce its holdings of Treasury securities by approximately $25 billion, down from the current pace of $60 billion.

This decision follows recent labor market data indicating a slight imbalance, with job openings reaching a three-month low in March. Nonetheless, private sector job gains in April surpassed economists' forecasts.

The upcoming nonfarm payrolls report, scheduled for release on Friday, is anticipated to reveal a robust addition of 243,000 jobs to the US economy in April.

EUR/USD continues its ascent on Thursday, buoyed by the prevailing positive sentiment in the market, which favors risk-sensitive currencies like the Euro. This optimistic outlook could be attributed to Federal Reserve Chairman Jerome Powell's dovish remarks on Wednesday. However, the Eurozone faces challenges due to a comparatively more dovish stance from the European Central Bank than the US Federal Reserve. Recent inflation data revealed that Eurozone inflation remained stable in April, meeting expectations.

Furthermore, core inflation declined, increasing speculation about a potential interest rate cut by the ECB in June. Thursday also sees the release of the final HCOB Manufacturing Purchasing Managers' Index data, with market expectations in line with the preliminary figures. This index serves as a leading indicator, providing insights into business activity in the Eurozone manufacturing sector.

In contrast, the Japanese Yen experiences significant selling pressure during the Asian session on Thursday, retracting from its over two-week high against the US Dollar seen the previous day. Initial reactions to rumors of Japanese authorities intervening again, for the second time this week, to bolster the domestic currency quickly diminish amid expectations of a wide US-Japan rate differential persisting. Additionally, a generally positive risk sentiment surrounding US equity markets acts as a key factor undermining the safe-haven appeal of the JPY.

Meanwhile, the USD/CAD pair continues its downward trend around 1.3730 during the early Asian trading hours. Late on Wednesday, Bank of Canada Governor Tiff Macklem reiterated the central bank's confidence in a continued decline in inflation. He stated that the BoC is "getting closer" to considering rate cuts, emphasizing that the BoC is not obligated to follow the Federal Reserve's playbook, as higher rates in Canada are proving more effective than in the US.

Traders are increasingly speculating that the Bank of Canada might implement interest rate cuts in June, given Canada's economic slowdown in the first quarter of this year. Canada's GDP expanded at a slower rate of 0.2% MoM in February, compared to the previous reading of 0.5%, falling below the market's expectation of a 0.3% expansion. Additionally, the Canadian Manufacturing PMI dropped to 49.4 in April and 49.8 in March, below the market consensus of 50.2, according to S&P Global on Wednesday.

Despite the weaker-than-expected Trade Balance and Building Permits data released by the Australian Bureau of Statistics, the Australian Dollar continues to strengthen on Thursday. The AUD/USD pair finds support from the overall positive market sentiment following dovish comments made by Federal Reserve Chairman Jerome Powell on Wednesday.

The Australian Dollar's rise can be attributed to the hawkish outlook surrounding the Reserve Bank of Australia, which is expected to maintain higher interest rates throughout 2024. Moreover, higher-than-anticipated domestic inflation data released last week has led to speculation that the RBA might postpone any interest rate cuts.

Traders are eagerly anticipating the release of weekly Initial Jobless Claims, Nonfarm Productivity, and Factory Orders from the United States on Thursday. These data points are expected to offer further insights into the current state of the US economy.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates