S&P 500 Ends Winning Streak Amid Jobs Report; Fed Rate Cut Expectations Adjusted | Daily Market Analysis

Key events:

- USA - NY Fed 1-Year Consumer Inflation Expectations

- Switzerland - SNB Chairman Thomas Jordan speaks

Despite a robust rally on Friday, the S&P 500 snapped a two-week winning streak as a stronger-than-expected jobs report failed to catalyze a significant increase in wages, instilling hope for a gentle economic transition.

The Dow Jones Industrial Average surged by 307 points, marking a 0.80% rise, while the S&P 500 and NASDAQ Composite climbed by 1.1% and 1.2%, respectively. Nevertheless, all three indices concluded the week in negative territory amid diminishing prospects of a rate cut in June.

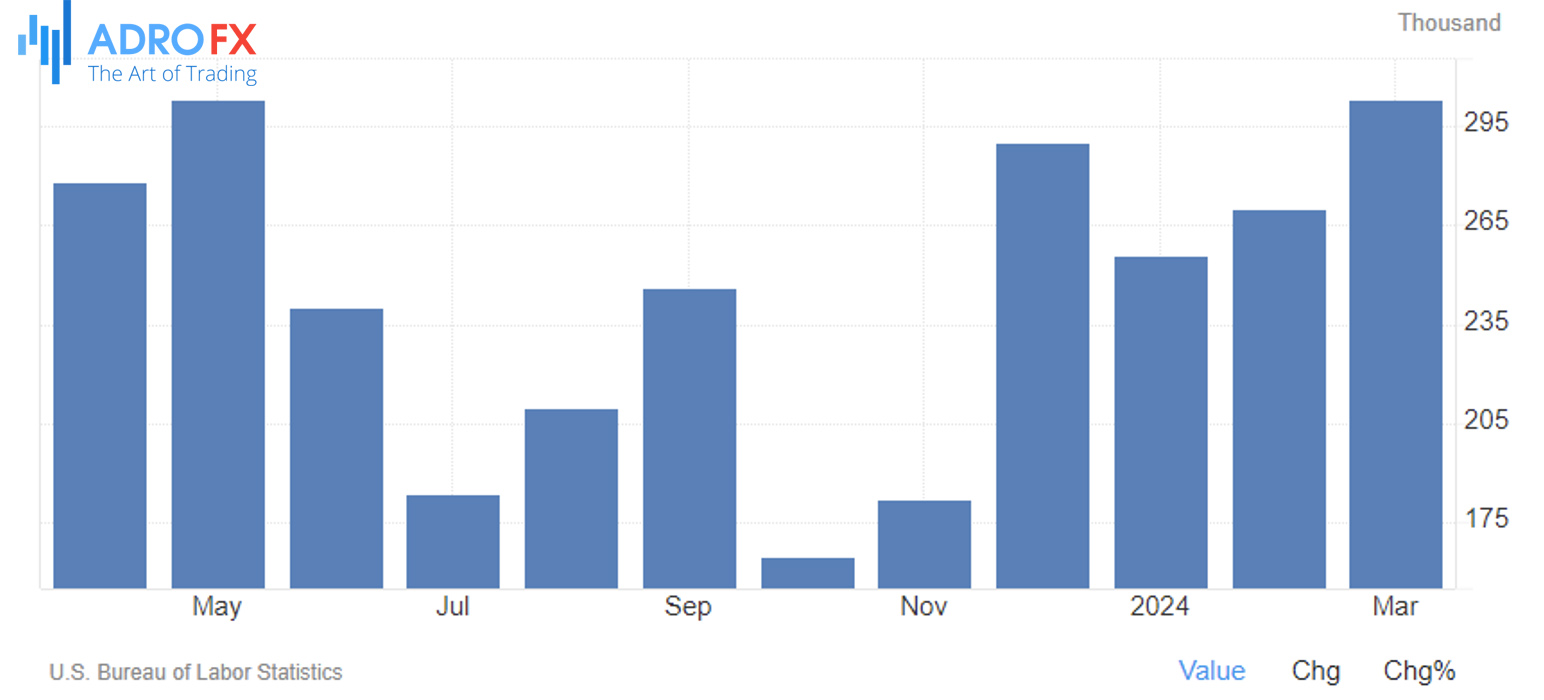

The latest data, released on Friday, unveiled a notable increase of 303,000 jobs in March, surpassing expectations of a 212,000 gain. Concurrently, the unemployment rate dipped to 3.8%, down from 3.9% the previous month, with average earnings experiencing a 0.3% monthly uptick in line with projections.

Despite the substantial surge in new job creation, the lack of a corresponding spike in wages mitigates concerns of an accelerated inflation pace. This phenomenon is attributed to a rise in the labor market participation rate, indicating a broader influx of individuals entering the workforce.

Although the likelihood of a June Fed rate cut decreased to 51% from 59% the preceding day, leading to an uptick in Treasury yields, Morgan Stanley remained steadfast in its prediction of a June cut.

The Australian Dollar managed to recover intraday losses and enter positive territory on Monday, possibly influenced by gains in the domestic equity market. The ASX 200 Index experienced upward momentum during the opening session of the week, particularly driven by a surge in tech stocks. However, the stable performance of the USD may exert pressure on the advancement of the AUD/USD pair.

The AUD encountered obstacles following the release of unchanged Final Retail Sales and disappointing Trade Balance data from Australia in the previous week. Notably, Australia reported its smallest Trade Surplus in five months for February, partly attributed to a decline in iron ore exports.

Meanwhile, the JPY underwent an intraday turnaround from a two-week high against its American counterpart on Friday, eventually settling near the lower end of its daily trading range. The Bank of Japan's dovish stance, indicating that the next rate hike will be deferred, along with positive risk sentiment, contributed to undermining the safe-haven JPY. The selling pressure persisted during the Asian session on Monday following the release of softer domestic data, revealing a continued decline in real wages in Japan for the 23rd consecutive month.

Despite recent assertions from Japanese authorities signaling readiness to intervene in the markets to support the domestic currency, the JPY bulls failed to find relief. This suggests that the path of least resistance for the USD/JPY pair remains to the upside amid expectations of a significant gap between US and Japanese interest rates. Market participants now await the release of the latest US consumer inflation figures and the FOMC meeting minutes on Wednesday for insights into the Fed's rate-cut trajectory, which will influence the USD and provide fresh impetus to the currency pair.

As for the EUR/USD pair, it struggles to capitalize on Friday's moderate rebound from levels below 1.0800 and encounters renewed selling pressure during the Asian session on Monday. Current spot prices hover around the 1.0825-1.0820 region, remaining sensitive to the dynamics of the USD. However, downside movements appear cushioned.

Nevertheless, the overall positive sentiment in global equity markets, supported by easing geopolitical tensions in the Middle East, may limit the appeal of the safe-haven Greenback.

Looking ahead, the US is poised to release consumer price inflation figures for March on Wednesday, with economists anticipating a slowdown in core inflation, which excludes food and fuel costs, to 3.7% year-over-year from 3.8% the previous month.

On Thursday, data on producer prices is expected to indicate a more tempered increase.

This inflation data follows Friday's release, which showcased that the US economy added significantly more jobs than anticipated last month, while wages saw a steady rise. This suggests that the pace of inflation may take time to moderate.

Meanwhile, the ECB convenes on Thursday, widely anticipated to maintain rates unchanged before initiating a rate-cutting cycle in June.

Market sentiment suggests an almost 100% probability of a 25 basis-point cut in June, so President Christine Lagarde's remarks will be closely scrutinized for indications.

Numerous policymakers have explicitly identified June as the likely timing for the first rate adjustment, further solidifying expectations for a rate cut as Eurozone inflation unexpectedly dipped to 2.4% in March.

Apart from the ECB meeting, central bankers in Canada and New Zealand are scheduled to meet on Wednesday, followed by meetings in Singapore and South Korea on Friday, with no rate changes expected.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates